Valued at a market cap of $4.3 billion, EnerSys (NYSE: ENS) is a global leader in stored energy solutions for industrial applications.

The world relies on reliable power, as data centers require backup systems, electric vehicles need rechargeable batteries, and military operations require portable energy sources. This creates massive opportunities for companies that deliver mission-critical power solutions.

EnerSys makes batteries and power systems for applications where failure isn’t an option. From hospital backup power to defense communications, EnerSys products ensure critical systems remain operational.

ENS stock offers investors exposure to multiple growth markets. The company serves data centers, telecommunications, defense, transportation, and industrial sectors. This diversification protects against downturns in any single market.

The company just launched “EnerGize” – a transformation plan focused on speed, efficiency, and growth. Management announced $80 million in annual cost savings and is reducing the office staff by 11% while investing in technology and product development.

ENS stock delivered mixed results in the first quarter of 2026. While revenue grew 5% year-over-year, earnings fell slightly due to customer hesitation related to tariffs. Notably, management expects this to be a temporary setback, with stronger results ahead.

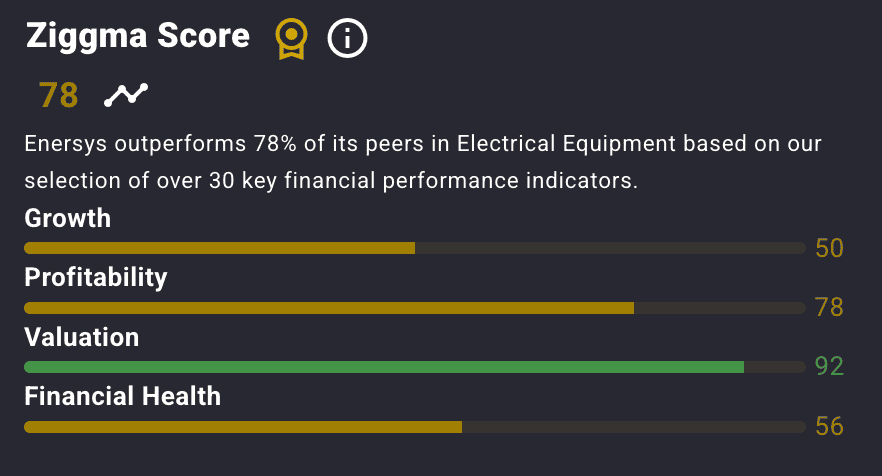

EnerSys stock has a Ziggma score of 78, ranking it in the top half of electrical equipment stocks. It also ranks highly in terms of valuation and profitability metrics.

EnerSys organizes its business into three main segments. Each targets different customer needs and technologies.

Energy Systems – Network Infrastructure: This segment provides backup power for telecommunications networks and data centers, ensuring continuous operation in the event of power outages. Products include lead-acid batteries, lithium systems, and power electronics.

Revenue hit $391 million in Q1, up 8% from last year. The data center market drives growth as AI and cloud computing demand more infrastructure. Moreover, communications customers are starting to reinvest after a period of slow growth.

Motive Power – Industrial Operations: EnerSys makes batteries that power forklifts and industrial equipment. These products are heavy-duty systems designed for warehouses and factories.

Revenue decreased 5% to $349 million in Q1, as tariff uncertainty led to customers delaying purchases. However, the long-term outlook remains strong as companies automate their warehouses and transition to electric equipment.

The company’s maintenance-free batteries are gaining market share, and although these products may cost more upfront, they ultimately save money on labor and maintenance. They now account for 27% of segment sales, up from 24% the previous year.

Specialty – Defense and Transportation: This segment serves the aerospace, defense, and commercial vehicle industries. The Bren-Tronics acquisition strengthened EnerSys’s position with the U.S. military.

Revenue increased 18% to $149 million, driven entirely by demand from the defense sector. The recent acquisition of Rebel Systems adds communication systems for military applications.

EnerSys reported its Q1 fiscal 2026 results, which show both challenges and opportunities ahead.

Revenue Trends: Total sales reached $893 million, up 5% year-over-year. Acquisitions contributed four percentage points of growth, while organic volumes actually declined by 1% as customers delayed their decisions.

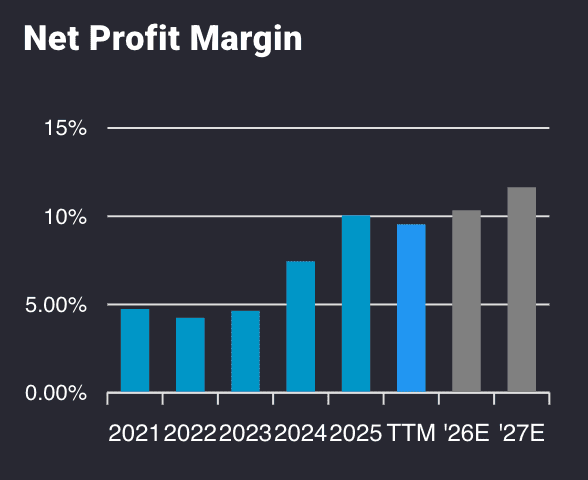

Rising Profitability: ENS’ net margin has been increasing in recent years and is projected to continue growing in 2026 and 2027, when it’s expected to surpass the 10% mark.

Cost Reduction Program: Management announced an $80 million cost-cutting plan. This includes $70 million in operating expenses and $10 million in manufacturing costs.

The program cuts 11% of office workers but doesn’t touch factory staff. EnerSys expects $30-35 million in savings this fiscal year, with the full benefits taking effect next year.

Strong Balance Sheet: Net debt stands at $964 million, equal to 1.6x EBITDA. This sits well below the company’s 2-3x target range. Strong credit metrics give EnerSys flexibility for acquisitions and share buybacks.

The Board approved a massive $1 billion share repurchase program over five years. This signals confidence in the business outlook and willingness to return cash to shareholders.

Resource efficiency gains: EnerSys achieved a 15% reduction in energy use per production unit since 2020. Water intensity dropped 6% over the same period. Total water consumption has fallen by 10% in just the past year.

These aren’t minor improvements. For a manufacturing company, reducing energy and water consumption while maintaining production demonstrates operational excellence.

Climate Action Roadmap: EnerSys has a clear climate action roadmap. It is committed to carbon neutrality for direct emissions by 2040. Purchased energy emissions are projected to reach net zero by 2050.

The company has already cut Scope 1 emissions by 25% since 2019. Another 4% reduction occurred last year, which indicates real progress.

EnerSys is also targeting leadership in the circular economy by operating a global battery take-back program. End-of-life batteries are recycled instead of being sent to landfills, while lead, plastics, and other materials are recovered and repurposed for reuse.

Battery materials have value, and recycling them reduces costs and environmental impact.

EnerSys benefits from structural growth trends across multiple end markets.

Data Center Boom: AI and cloud computing drive massive infrastructure build-outs. EnerSys holds a leading market share in lead-acid UPS systems. Importantly, data center revenue jumped 14% in Q1.

Defense Spending: Global military budgets are rising, and the Bren-Tronics and Rebel acquisitions position EnerSys for higher defense revenue. Moreover, modern military operations need portable, reliable power solutions.

Warehouse Automation: Companies are automating distribution centers, which requires more electric forklifts and charging systems. EnerSys’s maintenance-free batteries win in automated facilities because they need less human intervention.

Margin Expansion Path: The $80 million cost program yields $1.60 per share in annual savings, which is expected to boost net margins from 9.5% to 11.7% based on current revenue levels.

Substantial Tax Benefits: The 45X advanced manufacturing tax credit provides $35-40 million in quarterly benefits. These credits support investments in domestic battery production.

Management provided Q2 guidance of $870 million to $910 million in revenue, with earnings expected to range from $1.34 to $1.44 per share, excluding tax credits. That represents 8% growth at the midpoint despite ongoing macro uncertainty.

The company expects Q1 to mark the low point for the year, as tariff clarity is expected to improve customer confidence. Further, communications spending is recovering, and defense budgets continue to grow.

EnerSys repurchased $150 million of stock in fiscal Q1 at an average price of $86.20. With authorization now at $1.1 billion, expect aggressive buying when the stock dips.

ENS stock positions investors to benefit from electrification and digitization trends across the economy.

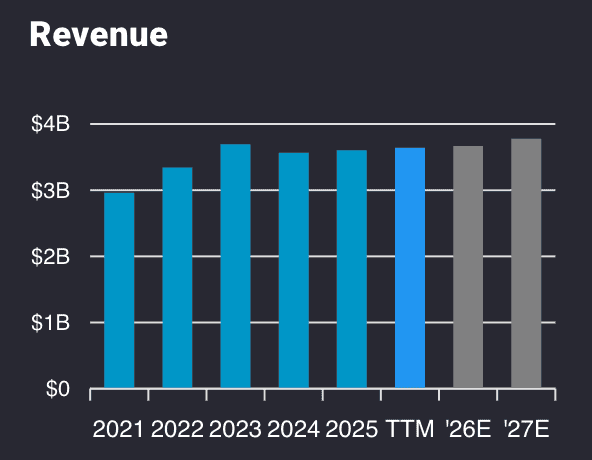

Analyst forecasts indicate solid growth rates that could accelerate significantly. Revenue should climb from $3.6 billion in fiscal 2024 to $3.8 billion in fiscal 2027. That represents roughly 2% annual growth.

Compared to fiscal 2024, net income is projected to increase from $345 million to $435 million in fiscal 2027. That equals an 8% annual growth rate, driven by margin expansion resulting from the restructuring program.

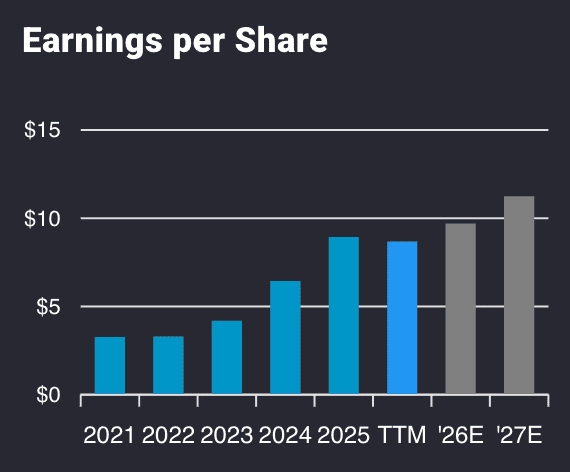

Thanks to a massive share repurchase program at 25% of the current market cap, ENS’ adjusted earnings are forecast to increase by 35% to $11.3 per share in 2027, from $8.35 per share in 2024.

Given the company’s market positions, margin expansion potential, and strong cash generation, ENS stock represents solid value for investors seeking exposure to critical infrastructure trends.