Amazon’s business mix is changing fast and firing on all cylinders – so is Amazon a good stock to buy? The market certainly thinks so. AMZN‘s 📈 stock price gained 46% over the past year and 20% year-to-date. Where will it go from here? What are the company’s prospects?

After having come to dominate online retailing, many pundits predicted dim growth prospects for Amazon. The company had failed to conquer the Chinese market, unable to match the growth of local players, such as Alibaba and JD.com.

Proving its many critics wrong, over the past ten years, Amazon has successfully diversified into not just one but several new massive revenue channels.

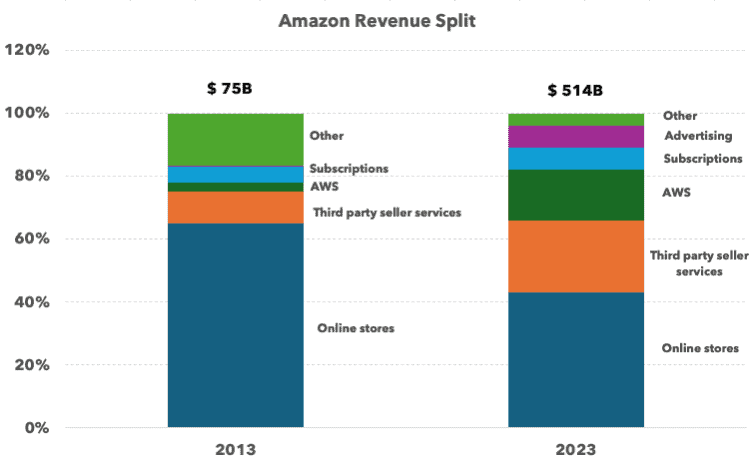

The share of revenue from online stores has decreased from 65% in 2013 to 43% in 2023. This relative decline reflects Amazon’s successful diversification into other revenue streams. Many of which have significantly higher margins that retail.

AWS’ share of revenue grew more than five-fold from 3% of revenue in 2013 to 16% in 2023. What’s more is that AWS is one of the most profitable segments for Amazon, contributing significantly to the company’s operating income and margins.

The third-party-service segment more than doubled from from 10% to 23%. The marketplace model has risen a great deal in importance within Amazon’s business mix, ranking second behind Amazon’s own online retail. It acts as a massive multiplication factor for its online business, as literally anyone can now start selling on Amazon in a matter of minutes.

Until very recently, advertising was not a significant revenue stream for Amazon. Thanks to Amazon’s platform, it has exploded into a $47B revenue stream. Amazon cleverly manages its extensive user data for targeted advertising, creating a new high-margin revenue stream.

Revenue from subscription services increased slightly from 5% to 7%, fueled by the growth of Prime memberships and additional services like Prime Video and Amazon Music.

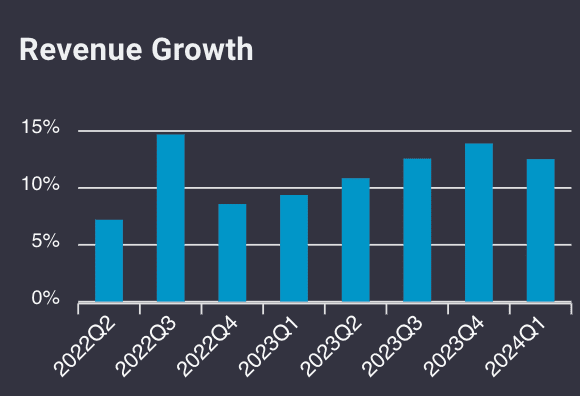

Amazon’s growth prospects are strong and structural. The company has been extremely successful in leveraging its dominance in e-commerce for the benefit of various business lines. Quarterly revenue growth was in the double digits in each of the past four quarters – an impressive feat for a company with over $500B in annual revenue.

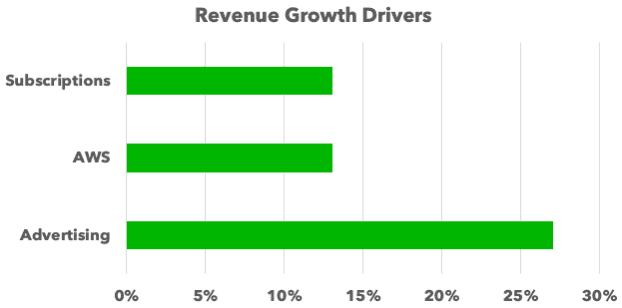

Amazon’s primary revenue drivers are advertising, AWS and subscriptions.

Advertising, which is closing in on $50B in annual revenue, grew by as much as 27% in the past year. AWS remains a powerhouse, buyoed by its cutting-edge cloud computing and AI solutions. The cloud business grew by 13% year-on-year. Amazon’s investment in content creation through Prime Video and its expansion into new markets generated an annual increase of 13% in subscription revenue.

These factors, coupled with Amazon’s relentless innovation and customer-centric approach, position it well for sustained growth and market leadership in the coming years.

Amazon’s profit is growing at a higher rate than its revenue, reflecting the company’s strategic focus on high-margin segments. In 2024, net profit is projected to grow at a rate of 46%. In 2025, net profit growth is expected too slow to a still impressive rate of 27%. By comparison, revenue is forecast to grow at 4% and 11% in 2024 and 2025 respectively.

Amazon’s focus on high-margin businesses has driven its profitability. Consequently, Amazon’s operating income has seen a marked increase, underscoring the effectiveness of the company’s revenue diversification strategy.

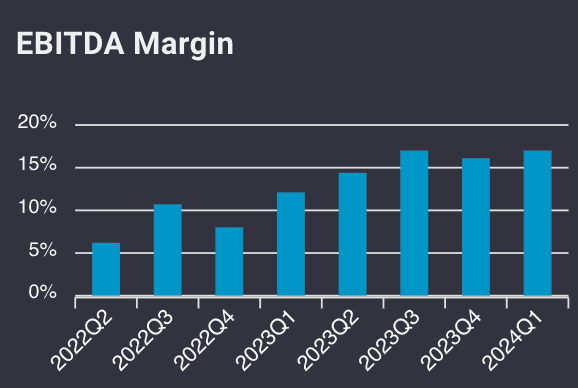

The rise in its EBITDA margin is impressive. It almost tripled in less than years from just 6% in Q2 2022 to 17% in Q1 2024.

Given that revenue growth is primarily driven by the two business lines with the highest margins, advertising and cloud, it can be expected that Amazon’s margins will continue to trend up.

Anyone who will simply look at Amazon’s price-to-earnings ratio (PE ratio) to determine whether the stock is cheap, expensive or fairly priced will quickly move on. Amazon’s PE ratio on last year’s earnings stands at jaw-dropping 52x. The verdict as to the prerogative is amazon a good stock to buy thus looks like a clear “stay away and look for cheaper stocks”.

A closer look, however, reveals that the company is a litteral cash-machine. Its massive investments, notably in data centers, are paying of in a big way. In Q4 of 2023 alone, Amazon reported a whopping $42.4B in cash-flow from operations.

Sign up for cutting-edge stock research.

For the full year 2023, net cash flow from operations was almost three times as high as net income – $85B versus $30B. With a ratio of 23x price to operating cashflow, Amazon’s valuation looks a lot less lofty compared to the earnings-based valuation. Amazon is off to a great start in 2024. Its operating cashflow was up 4-fold in Q1 2024. It is now likely that it will surpass the $100B mark this year.

Analysts have built in Amazon’s strong business prospects into their price targets. For them, the answer to the question is Amazon a good stock to buy is a clear yes.

The average analyst price target is currently at $221 – 21% above the stock’s current price of $186. Analysts have consistently raised their target price after starting off the year at $179. We believe this trend will continue. The market is playing catchup.

The findings of our fundamental analysis are in line with Wallstreet analysts. AMZN’s stock is a buy at this level. In fact, we believe that estimates will continue to trend upwards, as Amazon successfully executes on the massive opportunities in advertising and cloud computing. Upward revisions to the average price target will follow and could reach $250 before too long.

Important notice

This article is not to be understood as a recommendation to buy or sell. Please conduct your own research before making investment decisions. To this end, we aim to provide you with the best portfolio management tool and investment research data possible. However, we cannot guarantee the accuracy of this information in spite of our extensive efforts to ensure that the data is complete and 100% accurate.

Disclosure

Ziggma team members presently hold shares in one or several of the stocks mentioned in this article.