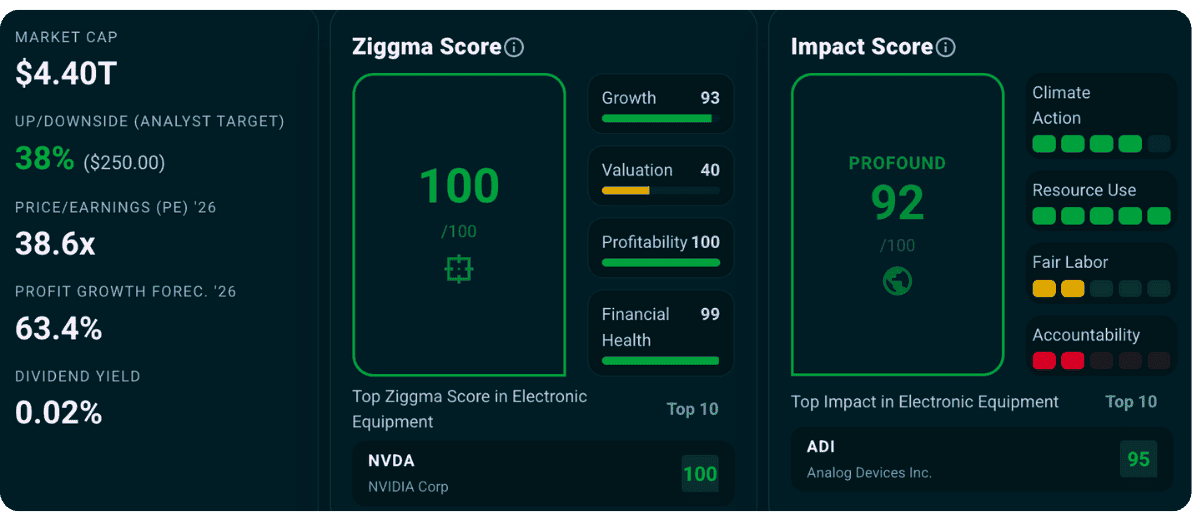

Nvidia has become synonymous with artificial intelligence. Its technology sits at the heart of today’s AI boom, powering everything from data centers and autonomous vehicles to climate modeling and medical research. For investors, Nvidia stands out not just for its exceptional growth and profitability, but also for the real-world impact its products enable. This combination places NVDA firmly in the Goodstocks universe: companies with strong long-term value creation potential and a meaningful positive contribution to society.

After an extraordinary run, the question is no longer whether NVIDIA is a great company—but whether it can continue to justify its premium. The data suggests it can.

Nvidia is the world’s leading designer of graphics processing units (GPUs) and accelerated computing platforms. Originally built for gaming graphics, its GPUs have become the backbone of modern AI, powering large language models, cloud computing, and advanced simulations.

Its core offerings include data center GPUs, AI software platforms such as CUDA, networking solutions, and systems designed for hyperscale data centers. Nvidia’s full-stack approach—combining hardware, software, and developer ecosystems—creates a powerful flywheel that competitors struggle to replicate.

The market opportunity is vast. Global spending on AI infrastructure is growing at a high single- to double-digit pace, with hyperscalers, enterprises, and governments racing to deploy AI at scale. Nvidia’s moat lies in its software ecosystem, deep customer integration, and years-long lead in performance and efficiency. Once customers build on Nvidia’s platform, switching costs become significant.

Nvidia’s share price is driven by explosive earnings growth, unmatched profitability, and a dominant competitive moat in AI computing. With revenue, earnings, and cash flow growing at exceptional rates, the company is compounding value faster than almost any large-cap peer. Analysts still see meaningful upside of 38% with an average price target of $250, supported by strong demand visibility and structural growth in AI infrastructure.

Nvidia’s chips are not just about speed—they are about efficiency. By dramatically improving compute performance per watt, Nvidia enables lower energy use per task, accelerates climate science, and supports breakthroughs in healthcare, clean energy, and scientific research. Its Impact Score reflects this dual role as both an innovation leader and a responsible corporate actor.

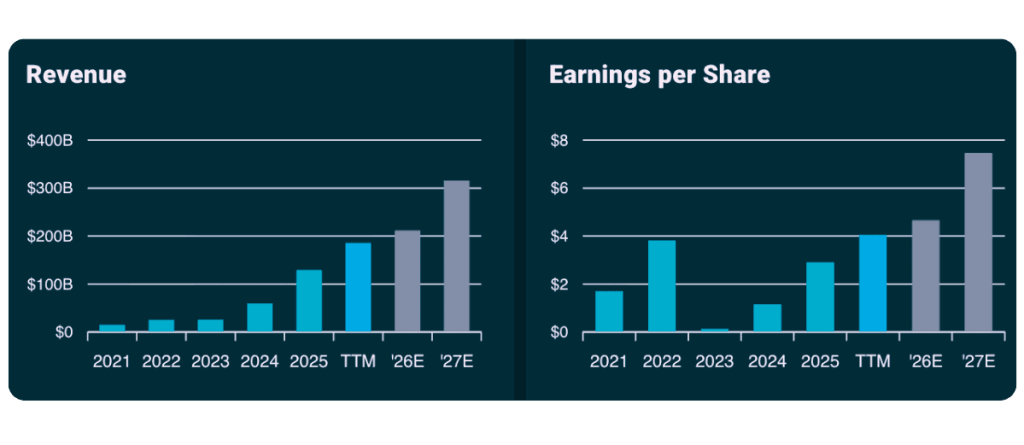

Nvidia’s financials underscore why the market continues to reward the stock. Over the past several years, revenue growth has accelerated dramatically, culminating in triple-digit growth rates in the most recent periods. TTM revenue growth stands above 60%, while EBITDA and earnings per share have surged even faster, reflecting powerful operating leverage.

Exceptional profitability

Profitability is exceptional. TTM net profit margins exceed 50%, EBITDA margins are above 60%, and return on equity has climbed past 100%, placing Nvidia among the most profitable companies globally. Cash flow margins above 40% highlight the quality and sustainability of these earnings.

Valuation not cheap but justified

Valuation remains elevated, with a forward P/E around the high-30s and price-to-sales multiples well above historical averages. However, this premium is partially justified by growth. With projected profit growth north of 60%, Nvidia’s valuation looks more reasonable on a growth-adjusted basis, especially compared to other mega-cap technology peers with far lower growth trajectories.

Valuation not cheap but justified

Growth visibility remains strong. Industry-specific KPIs such as data center backlog, hyperscaler capex plans, and AI model deployment all point to sustained demand. Nvidia’s order books are supported by multi-year investments in AI infrastructure, not short-term cycles. Analysts’ consensus price targets imply roughly 35–40% upside, reflecting confidence that earnings momentum can continue. While volatility is inevitable, the long-term upside remains compelling.

Nvidia’s impact goes far beyond financial returns. Its Impact Score of 92 places it among the top companies in electronic equipment, with particularly strong performance in Climate Action and Resource Use.

One key impact lies in energy efficiency. Nvidia’s GPUs deliver dramatically higher performance per watt, reducing the energy required for complex computations. This is critical as AI workloads scale globally, helping data centers lower their carbon footprint per unit of compute. Nvidia scores highly on climate metrics, including carbon intensity and alignment with lower global warming potential pathways.

Social impact

Equally important is the societal impact enabled by its technology. Nvidia-powered systems are used in climate modeling, renewable energy optimization, drug discovery, medical imaging, and autonomous safety systems. By accelerating research and innovation in these fields, Nvidia indirectly contributes to better healthcare outcomes, cleaner energy systems, and safer transportation.

Governance and workplace metrics are more mixed, particularly around executive pay ratios, but strong employee ratings and low fines and violations suggest a broadly responsible operating culture.

Nvidia’s investment case rests on three pillars. First, structural demand for AI compute continues to expand across industries, providing a multi-year growth runway. Second, Nvidia’s integrated hardware-software moat protects pricing power and margins, supporting sustained profitability. Third, ongoing innovation in efficiency strengthens both financial returns and environmental impact.

Over the next two to three years, upside could come from continued earnings growth, expanding AI adoption beyond hyperscalers into enterprises, and potential multiple resilience as Nvidia proves its earnings durability. While valuation is not cheap, few companies offer this combination of growth, profitability, and impact at scale.

Nvidia is not just riding the AI wave—it is shaping it. With industry-leading growth, world-class profitability, and technology that enables real progress in climate science, healthcare, and energy efficiency, Nvidia exemplifies what a Goodstock can be. For investors seeking long-term value creation with meaningful impact, NVDA remains a standout opportunity at the intersection of innovation and responsibility.

Important Notice

This article is not investment advice. We cannot predict whether the stocks mentioned in this article will go up or down.

We believe the information contained in this text to be reliable but do not warrant its accuracy or completeness. Opinions, estimates, and investment strategies and views expressed in this document constitute our judgment based on current market conditions available data and are subject to change without notice. Please consider your full financial situation prior to making an investment decision.