What if one of the most “boring” stocks in the market was setting up for double-digit upside?

Colgate-Palmolive is doing exactly that.

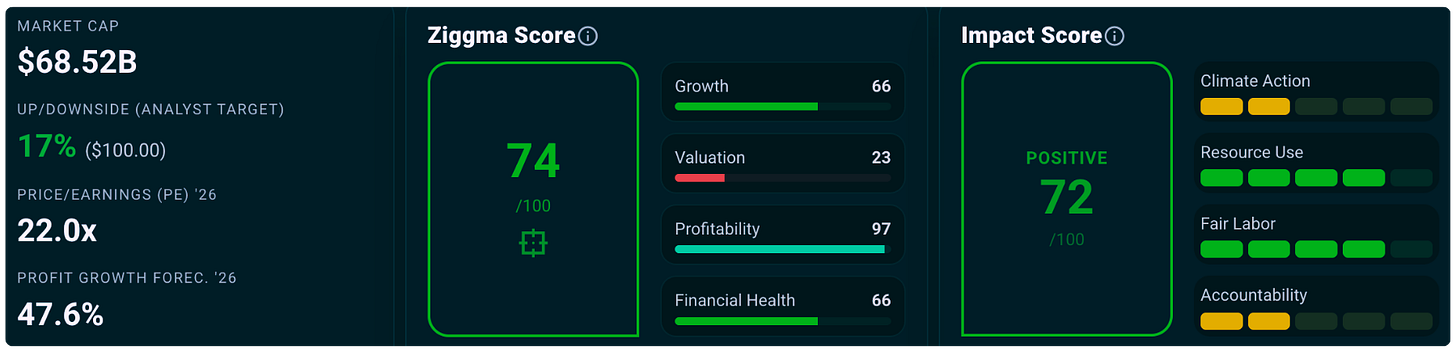

After a soft patch in early 2025, driven by currency headwinds and margin pressure, the business is more than stabilizing. Earnings are expected to rebound strongly, with projected profit growth of 47.6%, while analysts see about 17% upside to around $100.

At the same time, Colgate is improving how it operates. Its focus on sustainability is not cosmetic. It is increasingly tied to efficiency, cost control, and brand strength. In other words, sustainability that reinforces pricing power.

That combination of resilience, improving growth, and responsible operations makes Colgate eligible for the GoodStocks universe.

Colgate combines high profitability with a strong expected earnings rebound, while trading below its historical valuation range. This creates a credible setup for steady long-term returns with limited downside.

Colgate’s sustainability efforts improve resource efficiency and strengthen brand trust. Its high scores in resource use and labor practices reflect real operational progress, not just reporting.

Colgate-Palmolive is a global consumer goods company focused on oral care, personal care, home care, and pet nutrition.

Its core brands include Colgate, Palmolive, and Hill’s. These are everyday products used across millions of households. That creates predictable demand and repeat purchases, which are key drivers of long-term stability.

More than half of revenue comes from emerging markets. As incomes rise, consumers tend to shift toward trusted global brands. This supports steady volume growth over time.

Colgate’s competitive advantage is not based on rapid innovation. It comes from brand trust, distribution strength, and shelf presence. Once consumers choose a toothpaste or pet food brand, they rarely switch. That loyalty translates into pricing power.

Colgate’s financial profile reflects a business built for durability.

Revenue growth has averaged 3.2% over five years, with a temporary slowdown to 1.4% in 2025. Earlier periods showed stronger momentum, including 8.3% growth in 2023.

Profitability remains the core strength. Net margins consistently range between 11% and 15%, while cash flow margins exceed 20%. These are strong levels for a consumer goods company and signal efficient operations.

Return on equity is exceptionally high, reflecting strong capital efficiency and brand-driven economics.

The stock declined in early 2025 due to currency headwinds, input cost pressures, and some volume softness.

Importantly, pricing held. Margins have stabilized, and the underlying business remains intact.

This suggests the decline was driven by external factors rather than a deterioration in fundamentals. For long-term investors, that distinction creates opportunity.

Colgate currently trades at about 22x forward earnings, below its long-term average near 30x.

At the same time, earnings are expected to grow by 47.6%. This combination of improving growth and a more reasonable valuation strengthens the investment case.

Colgate’s future growth is driven by three clear levers.

First, pricing power. The company has consistently demonstrated the ability to raise prices without losing customers.

Second, emerging markets. Rising middle-class populations continue to drive demand for branded consumer products.

Third, premiumization. Higher-value products in oral care and pet nutrition support margin expansion.

Analysts currently see about 17% upside, with a target price near $100.

When combined with a dividend yield of around 2.4%, this creates a balanced return profile. Not explosive, but reliable and attractive for long-term investors.

Emerging market exposure introduces currency volatility. Private label competition can pressure pricing during weaker economic periods. Growth remains moderate compared to high-growth sectors. And valuation, while improved, is not deeply discounted.

Colgate offers a rare combination of stability, strong profitability, and improving growth momentum. With earnings rebounding and valuation below historical levels, the stock has credible upside in the high teens with relatively lower risk.

Colgate’s strongest impact comes from how efficiently it uses resources.

Its Sustainable Resource Use score of 78 reflects progress in water efficiency, packaging improvements, and operational optimization.

This is where sustainability connects directly to financial performance. Lower resource use reduces costs and supports margins over time. It also strengthens the brand in the eyes of increasingly conscious consumers.

This is sustainability that reinforces pricing power.

Colgate also scores well on labor practices, with a 4.2 (out of 5) employee rating.

Employee satisfaction is high, and gender equality metrics are strong. These are important indicators for a global workforce and contribute to operational stability.

A motivated workforce and strong culture support consistent execution across markets.

Colgate-Palmolive does not promise rapid disruption or headline growth. Instead, it delivers consistency, strong margins, and reliable cash flow.

Today, the setup is improving. Earnings are expected to rebound, valuation is more attractive than usual, and pricing power remains intact.

At the same time, the company is becoming more efficient in how it operates. That efficiency reduces waste, supports margins, and strengthens long-term competitiveness.

For investors, that combination matters.

Colgate is not exciting. It is effective. And over time, that tends to win.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.