Clearway Energy (CWEN) stands out as one of the most compelling income-and-impact opportunities in today’s market. Backed by long-term contracted cash flows, a diversified renewable energy portfolio, and a mission to accelerate the clean energy transition, CWEN combines reliable shareholder value creation with measurable environmental benefit.

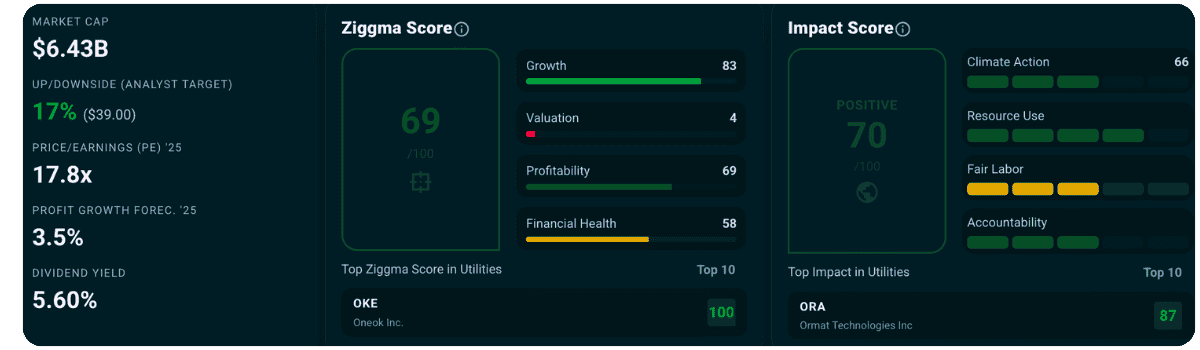

With a Ziggma Score of 73, an Impact Score of 70, and a dividend yield approaching 5.8%, CWEN fits squarely into the GoodStocks universe—companies that deliver both attractive financial returns and positive real-world outcomes.

CWEN offers steady, predictable cash flows, strong EPS momentum (projected 25%+ growth next year), a healthy analyst upside target of 19%, and one of the most attractive dividends in the utilities sector.

Producing large-scale clean electricity, reducing dependence on fossil fuels, and maintaining strong Climate Action and Resource Use scores, CWEN directly contributes to decarbonizing the power grid.

Clearway Energy is one of the largest owners of renewable energy assets in the United States, operating utility-scale wind, solar, and energy storage facilities. Its business model is straightforward and resilient: CWEN owns energy-generating assets and sells electricity under long-term contracts, often 10–20 years, to highly rated utilities and corporate buyers.

This contracted revenue model provides exceptional cash flow visibility, a rarity in the utilities space. CWEN also benefits from Clearway’s development partner, Clearway Energy Group, which continuously feeds the company a pipeline of new renewable projects.

Renewable energy remains one of the fastest-growing segments of the U.S. power system, with long-term structural tailwinds driven by policy support, declining costs, and electrification. The industry’s projected growth rate of ~9%, reflected in CWEN’s strengths profile, underscores this momentum.

CWEN’s moat is built on:

This positioning gives CWEN durable competitive advantages relative to smaller or less integrated renewable developers.

CWEN’s financial profile reflects the typical dynamics of a capital-intensive utility, but with improving performance and attractive shareholder distributions.

Profitability has fluctuated due to acquisitions, asset rollouts, and one-time accounting items, yet key long-term indicators show continued improvement:

Clearway’s return metrics (e.g., ROA near -0.5%) reflect heavy depreciation and investment rather than weak performance. This is common for renewable operators with large upfront capital expenditure.

Debt/equity has improved from 2.6x to 1.6x (TTM), and net debt/EBITDA at 7.8x remains manageable for a contracted-asset utility. Interest coverage is tight at 0.6x, a typical characteristic of yieldcos, but CWEN mitigates this with predictable PPA-backed revenues.

CWEN trades at 17x forward earnings, well below its 35.1x 5-year average – a sign of significant multiple compression. Its price/sales of 3.9x and EV/revenue of 9.5–10x are in line with peers, but the valuation discount suggests that investor sentiment may be overly pessimistic given the company’s improving earnings trajectory.

The dividend yield of 5.76% is a key part of the total return proposition and is well supported by cash generation.

Analysts see CWEN reaching $39, implying 19% upside from current levels. Combined with the nearly 6% dividend, total return potential becomes highly attractive.

If EPS growth materializes as expected and valuation multiple regains even a portion of its historical norm, CWEN could experience meaningful rerating over the next 24–36 months.

Impact Analysis + Renewable Energy at Real Scale

CWEN’s Impact Score of 70 puts it firmly among the leading utilities for positive environmental contribution. The company’s entire operating model—developing and owning clean power assets—directly reduces carbon intensity across the U.S. power grid.

CWEN scores 66 in Climate Action, with strong performance on:

Although carbon intensity per MWh remains high (score: 16), this measure often reflects grid-mix allocations rather than actual project-level emissions. What matters is the renewable output CWEN delivers into the system.

CWEN’s 75 score in Sustainable Resource Use highlights effective water management, waste practices, and use of renewable energy inputs across its operations—a major positive relative to fossil-based utilities.

With Fair Labor (60) and improving governance metrics, CWEN demonstrates responsible stakeholder management appropriate for a large infrastructure operator.

In short, Clearway enables cleaner electricity at scale—making it a quintessential GoodStock.

CWEN’s investment case over the next 2–3 years hinges on three core drivers:

Coupled with CWEN’s strong Impact Score and role in decarbonizing the U.S. electricity mix, the stock delivers both financial upside and genuine societal benefit.

Clearway Energy is a rare blend of yield, growth potential, and real-world climate impact. With a discounted valuation, strong projected EPS rebound, and one of the highest impact scores in the utilities sector, CWEN offers investors a credible pathway to doing well while doing good. For long-term impact-minded investors seeking stable income and exposure to renewable energy infrastructure, CWEN stands out as a compelling GoodStock.