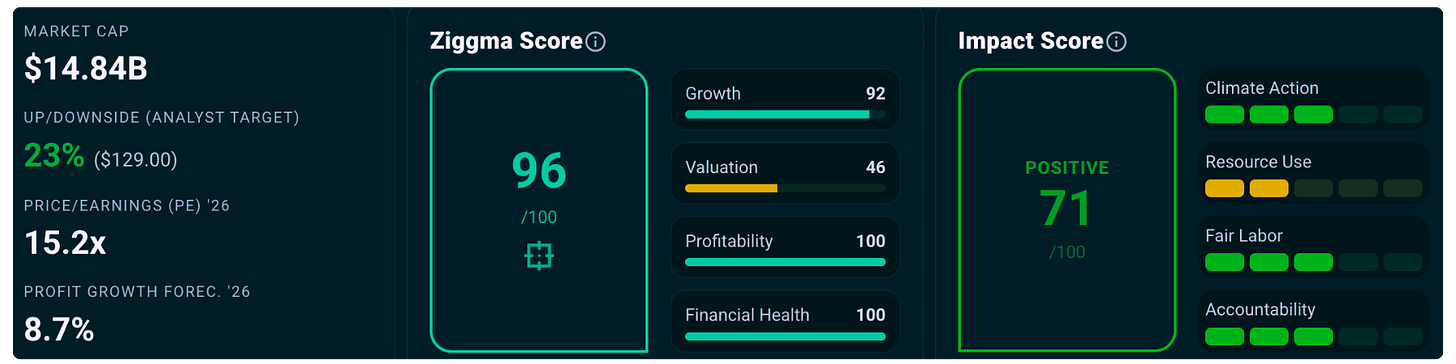

In a market often driven by hype, Deckers Outdoor Corporation (DECK 📈) stands out for a different reason. It sports a rare combination of sustained growth, elite profitability, and a corporate culture that employees genuinely value.

With a Ziggma Score of 96, strong brand momentum led by HOKA, and improving sustainability credentials, Deckers is a compelling example of responsible growth investing. And after a sharp reset in valuation, the opportunity may be more attractive than it has been in years.

Deckers delivers a rare combination of double-digit growth and top-tier profitability, yet trades at a modest earnings multiple following a recent sell-off. That disconnect creates a compelling setup for continued compounding.

Deckers shows how responsible growth investing works in practice. Strong employee satisfaction, climate alignment, and responsible operations are not just values, they reinforce brand equity and pricing power.

Deckers has built a portfolio of premium footwear brands led by HOKA and UGG, both of which command strong customer loyalty.

HOKA continues to capture share in the global running and performance footwear market, benefiting from structural trends in fitness and comfort. UGG remains a dominant lifestyle brand with enduring pricing power.

The broader market continues to grow steadily, but Deckers’ real advantage lies in brand strength. It competes on identity and experience rather than price, allowing it to sustain higher margins and deeper customer relationships.

Deckers has delivered consistent revenue growth in the mid-teens, with earnings growing even faster. This reflects strong operating leverage and disciplined execution.

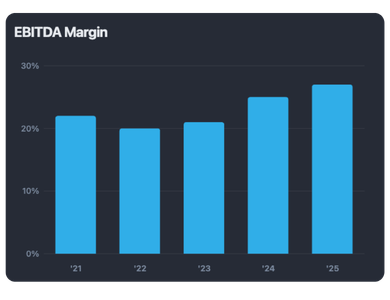

Profitability is exceptional. Net margins are approaching 20%, EBITDA margins exceed 25%, and return on equity is close to 40%. These are elite levels, particularly in apparel.

The Ziggma Score of 96 reflects strength across all key dimensions. Growth, profitability, and financial health all rank near the top of the industry.

This is not a cyclical rebound story. It is a structurally strong business.

The most interesting part of the story is valuation.

In 2025, the stock experienced a sharp correction. A key driver was concern around tariffs and potential pressure on margins, particularly given Deckers’ exposure to global manufacturing and supply chains. Investors reacted aggressively, pricing in a worst-case scenario for cost inflation and demand disruption.

But the reality has been more nuanced.

Deckers has mitigated much of this pressure through a combination of pricing power, supply chain adjustments, and brand strength. Premium positioning allows the company to pass through costs more effectively than lower-end competitors. At the same time, operational discipline has helped protect margins.

As a result, fundamentals have remained intact while valuation compressed.

Today, Deckers trades at roughly 15x forward earnings, below its historical average and modest relative to its growth profile.

This creates a rare situation where a high-quality compounder is available at a growth-at-a-reasonable-price valuation.

Analysts currently see around 23% upside, with price targets near $129.

HOKA remains the primary growth engine, with continued global expansion and category penetration. Direct-to-consumer channels are strengthening margins and customer relationships. Brand extensions into adjacent categories further increase long-term potential.

Competition remains intense, particularly from global footwear leaders. Brand momentum must be maintained. Cost pressures could return if macro conditions worsen. Sustainability execution must keep pace with expectations. Any slowdown in HOKA would impact overall growth.

Deckers offers a combination of growth, profitability, and valuation that is rarely available at the same time.

Deckers is aligned with a 1.5°C climate trajectory, reflecting efforts to reduce emissions and improve materials sourcing. While apparel remains resource-intensive, the company is moving in the right direction.

With waste recycling around 65% and improving water efficiency, Deckers shows measurable progress, though further gains are needed to reach best-in-class levels.

One of the most striking aspects is employee satisfaction. A 5.0 out of 5 rating signals an exceptionally strong internal culture.

This is not just a feel-good metric. High employee engagement translates into better execution, stronger innovation, and ultimately better financial performance.

Consumers increasingly reward brands they trust. Deckers benefits from this shift. Responsible practices reinforce brand perception, which in turn supports pricing power and loyalty.

This is the essence of responsible growth investing. Responsibility strengthens the business model rather than detracting from it.

Deckers represents a compelling opportunity where multiple forces align.

Strong growth driven by HOKA, elite profitability, and a valuation reset create the foundation for attractive returns. At the same time, high employee satisfaction and responsible practices strengthen the company’s long-term competitive position.

Over the next two to three years, earnings growth and potential multiple expansion could drive meaningful upside.

Deckers may not be the most obvious story in the market.

But it is one of the most compelling.

Following the tariff-driven sell-off, the stock now trades at a meaningful discount relative to its own history and to premium peers like Nike. Yet its growth profile, profitability, and brand momentum remain intact.

At the same time, Deckers benefits from something harder to quantify but equally powerful. A highly engaged workforce, responsible practices, and strong brand trust.

That combination is what responsible growth investing is all about.

And it is why Deckers stands out as a company where returns and responsibility move in the same direction.