Finding the best cheap stocks to buy now has become a top priority for investors mindful of a pricey market and political uncertainty. Cheap stocks with low price-to-earnings (P/E) ratios can offer tremendous opportunities, particularly when paired with strong forward-looking growth potential.

This combination – often referred to by the acronym GARP for growth at a reasonable price – allows investors to benefit from both stock price appreciation and a margin of safety, making it an effective strategy for navigating today’s dynamic market environment.

For this post, we’ve identified five standout stocks that meet two essential criteria: a P/E ratio below 15x and double digit earnings growth. These stocks are not only undervalued compared to their peers but also positioned to capitalize on industry trends, improving fundamentals, or innovative strategies. Growth at a reasonable price is the sweet spot of many famous investors, such as Warren Buffet, Peter Lynch or Michael Burry.

Pro Tip: Before buying any of these cheap stocks, make sure you take advantage of these six apps that will give you free stocks for signing up.

As a long-term investor looking to build a high-performing portfolio, these five stocks deserve your attention as some of the best cheap stocks to buy now.

Let’s dive into the list and explore why each one stands out as a compelling opportunity for value-conscious investors.

United Therapeutics Corporation is a biotechnology company focused on developing innovative therapies to treat rare and life-threatening diseases, including pulmonary arterial hypertension and other chronic conditions. Headquartered in Silver Spring, Maryland, the company leverages cutting-edge technologies such as regenerative medicine, organ manufacturing, and advanced drug delivery systems to improve patient outcomes.

Here are three compelling reasons why UTHR is on the list of the best cheap stocks to buy now.

1 – Attractive Valuation: UTHR trades at a discount relative to its biotech peers, despite delivering consistent revenue growth and robust profitability. This undervaluation provides an opportunity for investors to acquire a growth-oriented company at a discounted price, offering potential for significant upside as the market re-rates its valuation.

2 – Innovative Pipeline and Long-Term Growth Potential: UTHR is heavily invested in cutting-edge areas such as organ manufacturing, regenerative medicine, and advanced therapies for rare diseases, including pulmonary arterial hypertension. Its diversified pipeline positions the company for sustained growth in high-demand markets, with the potential for blockbuster products that could drive future earnings.

3 – Financial Strength: UTHR has one of the best balance sheets in biotech. The company operates with minimal financial leverage as evidenced by a debt to equity ratio of just 0.1x. At the same time, operating cash flow is strong and growing fast. After closing in on $1bn in 2023, UTHR can be expected to surpass that threshold in 2024. With a solid balance sheet, strong cash flow generation, and minimal debt, UTHR is well-equipped to weather economic uncertainty and reinvest in growth initiatives. This financial stability, coupled with its focus on addressing critical unmet medical needs, makes it a compelling choice for value-conscious investors seeking growth in the biotech sector.

Also Read: The Best Stocks to Own in 2025

Mr. Cooper Group is a leading home loan servicer and mortgage lender, providing comprehensive servicing, origination, and real estate solutions to homeowners and investors. Headquartered in Coppell, Texas, the company has thrived by combining a customer-centric approach with cutting-edge technology.

COOP’s strong prospects haven’t been lost on one of Wall Street’s famous value investors Leon Cooperman. Through his hedge fund, Cooperman owns close to 5% of the company.

On present earnings estimates, COOP’s 2025 price to earnings ratio stands at just 7.7x. Given projected earnings growth of 29%, COOP’s PEG ratio is as low as 0.3. It turns COOP a well-deserved spot on our shortlist of the best cheap stocks to buy now. Generally, a stock trading at a PEG ratio below 1 is considered good value.

Owning a true GARP stock alongside Leon Cooperman is certainly one of the better bets in the market right now.

Also Read: Best Renewable Energy Stocks

JPMorgan Chase & Co. is a leading global financial services firm and one of the largest banking institutions in the world, with operations spanning investment banking, asset management, commercial banking, and consumer financial services. Headquartered in New York City, the bank has been serving millions of customers across over 100 markets worldwide for over 200 years.

Jamie Dimon may have some regrets about his massive stock sale in 2024. In Q2 2024, Dimon raked in $184m by selling 1 million shares in JPM. The price at the time? $184. Today, JPM’s stock price is a whopping 44% higher and rising still.

If it’s any consolation to Jamie Dimon, the bellwether scenario for JPM’s stock price was not an easy one to predict. It is largely driven by higher rates for longer and the Republican’s sweeping election victory.

With projected earnings growth in the double digits at 12%, and a P/E ratio of below 15x, JPM holds a solid place on the list of best cheap stocks to buy now. Add to that, the prospects of less bank regulation and lower capital requirements. These mean higher profitability and potentially return of capital to shareholders through dividends or buybacks.

First Solar provides photovoltaic (PV) solar energy solutions in the United States, Japan, France, Canada, India and Australia. The company designs, manufactures, and sells cadmium telluride solar modules that converts sunlight into electricity. First Solar is headquartered in Tempe, Arizona.

The market’s pricing of FSLR at a P/E ratio of 8.6x might raise questions, particularly for investors focused on renewable energy’s long-term potential. Since it became clear that Donald Trump would win the White House, the stock has lost 42%, although it is still up over one year. Investors have been selling FSLR due to policy uncertainties surrounding renewable energy, including fears about reduced government incentives or shifts in support toward fossil fuels.

However, determining whether the market is “wrong” depends on a closer analysis of several factors:

1 – Policy and Industry Outlook: While the Trump administration may have introduced a less favorable policy environment for renewables, global trends continue to favor solar energy. In most places, solar energy is now the cheapest form of energy. So politics aside, betting on solar is simply a good business decision. This is why solar will continue to grow, even in Texas.

2 – FSLR’s Fundamentals: A forward P/E ratio of 8.6x is significantly below the broader market average. It suggests significant undervaluation, especially since analysts have only slightly revised FSLR’s earnings prospects downwards..

3 – Market Sentiment vs. Long-Term Trends: Often, markets overreact to political changes in the short term. If FSLR’s growth trajectory aligns with increasing global renewable energy adoption, the current valuation presents an opportunity for long-term investors, making FSLR one of the best cheap stocks to buy.

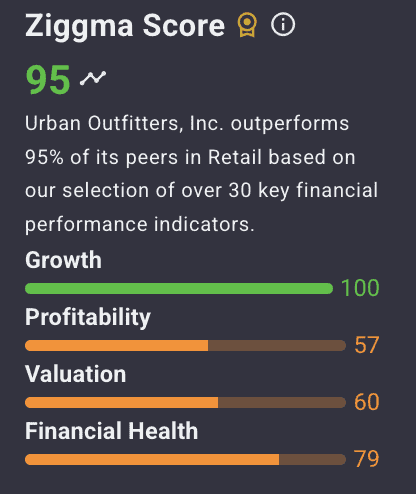

Urban Outfitters is a lifestyle retail company that specializes in on-trend fashion, accessories, home decor, and unique lifestyle products. Headquartered in Philadelphia, Pennsylvania, the company operates a portfolio of popular brands, including Urban Outfitters, Anthropologie, and Free People, catering to a diverse and creative customer base. With a focus on innovation, experiential retail, and sustainable practices, Urban Outfitters has become a global leader in delivering distinctive shopping experiences both online and in-store.

The final stock on our list of the five best cheap stocks to buy now is a high-performing retail standout, Urban Outfitters (URBN). URBN has consistently outpaced competitors and is projected to deliver high single-digit revenue growth for each of the next two years. This growth is fueled by the company’s strong brand portfolio, which includes Anthropologie and Free People, brands that appeal to a broad and diverse customer base, particularly in the trendy and lifestyle-driven retail segments. URBN has also been a leader in e-commerce and omnichannel strategies, seamlessly integrating its online and in-store experiences to capture a growing share of online shoppers, driving additional sales growth.

For investors seeking exposure to the retail sector, URBN offers a compelling opportunity with accelerating earnings growth available at a reasonable valuation of just 15x forward earnings.

In conclusion, identifying the best cheap stocks to buy involves finding companies that combine strong growth potential with attractive valuations. The stocks highlighted in this analysis showcase the perfect balance of financial strength, forward-looking strategies, and market opportunities, making them excellent candidates for value-conscious investors. By focusing on companies with robust fundamentals and solid growth prospects, investors can position themselves to capitalize on these undervalued opportunities while building a portfolio with long-term potential. As always, careful research and alignment with individual investment goals are key to making informed decisions.