Mastercard (NYSE:MA) is showing the world that a company can fuel the digital economy and widen access to financial opportunity—all while delivering world-class shareholder returns. With a market cap of $515 billion and a 12,000% gain since its 2006 IPO, Mastercard proves that doing good and doing well aren’t competing goals—they’re compounding forces.

Mastercard operates one of the world’s most essential networks—connecting consumers, merchants, banks, fintechs, and governments across 210+ countries. It is the plumbing behind modern commerce.

The business runs through three growth pillars:

‣ Consumer Payments: The core global card network

‣ Commercial & New Payment Flows: B2B, cross-border, and real-time payments

‣ Value-Added Services: Cybersecurity, data analytics, loyalty, digital identity

Mastercard processes 3.6 billion cards worldwide, with switching transactions up 10% year-over-year in Q2 2025. The company’s global footprint and strong network effects create a durable competitive advantage: more consumers → more merchants → more banks → more revenue.

This is the definition of a scalable, defensible business with generational tailwinds: cash displacement, e-commerce growth, travel recovery, and the digitization of nearly every economic activity.

Mastercard continues to deliver outstanding financial performance while benefitting from structural global trends.

Q2 2025 Results

👉 Revenue: +16% YoY

👉 Net income: +12% YoY

👉 Payment Network revenue: +13% YoY

👉 Cross-border volumes: +15% YoY

👉 Value-Added Services revenue: +22% YoY

Management now expects full-year net revenue growth in the low teens, reflecting continued strength across spending categories.

Mastercard earns a Ziggma Stock Score of 100, supported by elite profitability, strong growth, and a fortress-like financial profile.

From a shareholder-value perspective, Mastercard has one of the cleanest business models in the S&P 500: high margin, low capex, recurring revenues, and global optionality.

Mastercard isn’t just a payments company. It is one of the most influential engines of global financial inclusion.

The company has helped bring millions of unbanked individuals into the digital economy through partnerships with NGOs, governments, and financial institutions.

Key impact themes:

✔️ Empowering small and micro-businesses with digital payments tools

✔️ Supporting women entrepreneurs across emerging markets

✔️ Delivering ID-enabled payment solutions for refugees and underserved communities

✔️ Building resilient local economies by improving access to financial services

This isn’t charity—it’s strategic. Financial inclusion drives long-term spending growth, which feeds directly back into the network.

Mastercard integrates sustainability into product design, network innovation, and strategic partnerships.

Highlights include:

✅ Net-zero commitment with investments in renewable energy

✅ Carbon Calculator that lets consumers track the footprint of their purchases

✅ Priceless Planet Coalition, which aims to restore 100 million trees globally

✅ Tokenization and digital ID initiatives that reduce fraud, waste, and physical-card dependency

In short, Mastercard is proving that large global financial companies can lead on environmental stewardship and digital trust.

Several structural forces support Mastercard’s long-term value creation:

Includes consumer payments, commercial flows, and value-added services—each with decades of runway left for digitization.

Roughly $11 trillion in global transactions are still in cash or checks—ripe for conversion.

15% YoY growth, with no route representing more than 3% of volume—providing diversification and resilience.

85% recurring revenue from cybersecurity, analytics, loyalty, and ID solutions—making Mastercard less cyclical and more software-like.

Analysts expect:

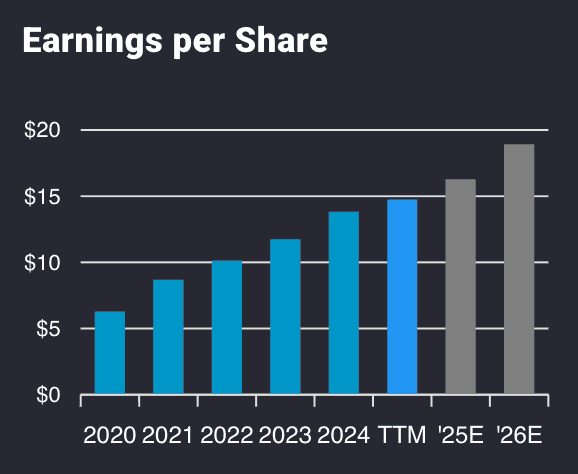

✔️ EPS to double from $14.6 to $29 over the same period

If priced at 30x forward earnings, MA stock could climb 50%+ in the next four years.

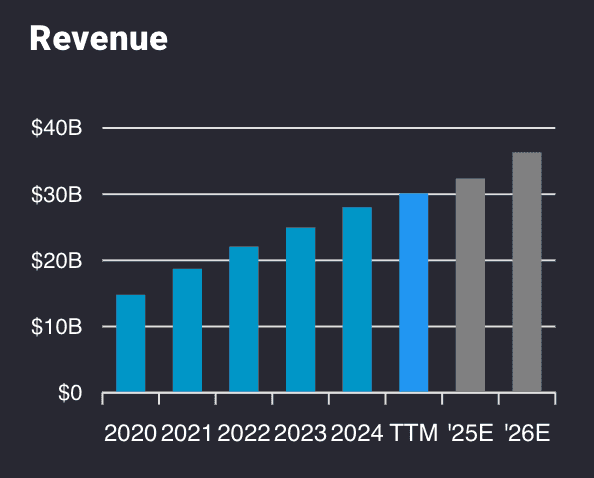

✔️ Revenue to rise from $28.2B in 2024 to $48.8B in 2029

EPS to double from $14.6 to $29 over the same period

If priced at 30x forward earnings, MA stock could climb 50%+ in the next four years.

Revenue to rise from $28.2B in 2024 to $48.8B in 2029.

Cross-Border Leadership: Cross-border volumes grew 15% year-over-year, benefiting from travel recovery and e-commerce growth

Services Diversification: Value-added services provide 85% recurring revenue with significant expansion opportunities in cybersecurity and data analytics

Mastercard’s growth strategy centers on multiple expansion vectors. The consumer payments opportunity includes a $11 trillion cash and check market that is still available for digitization, while commercial payments represent an $80 trillion addressable market with significant untapped potential.

The company’s technological investments in tokenization, artificial intelligence, and digital identity create competitive moats while opening new revenue streams. Management reported that tokenized transactions drive 3-6 percentage points higher spending compared to non-tokenized transactions.

Cross-border payments remain a key differentiator, with no single corridor accounting for more than 3% of total cross-border volumes, thereby providing geographic diversification and resilience.

Management maintains strong full-year guidance expectations, targeting net revenue growth in the low teens range, supported by healthy consumer spending trends and successful execution of strategic initiatives.

MA stock is exceptionally well-positioned to benefit from the ongoing global shift toward digital payments while providing essential infrastructure for the modern economy.

Analysts tracking the MA stock forecast continued strong performance as digital payment adoption accelerates across consumer, commercial, and government sectors worldwide.

Wall Street expects Mastercard to increase revenue from $28.2 billion in 2024 to $48.8 billion in 2029. During this period, adjusted earnings are expected to grow from $14.6 per share to $29 per share.

If MA stock is priced at 30x forward earnings, which is a reasonable valuation, it should gain over 50% over the next four years.

Market dynamics support sustained expansion as cash usage continues to decline globally, cross-border commerce grows, and businesses increasingly digitize their payment processes.

Given the company’s strategic market position, execution track record, and exposure to unstoppable digital transformation trends, MA stock represents compelling value for investors seeking exposure to the future of global commerce.

What is the Mastercard Stock Price?

Mastercard stock trades at $570 as of September 23, 2025.

Will Mastercard Stock Split in 2025?

There is no news of a stock split for Mastercard in 2025.

Who Owns Mastercard Stock?

The top holders of Mastercard stock include The Vanguard Group, the Mastercard Foundation Asset Management, BlackRock Institutional Trust, State Street Global Advisors, and Fidelity Management.