A new report by Schroders and the Saïd Business School at Oxford University is reshaping the narrative around positive impact investing. The research provides strong evidence that positive impact investing in listed equities can deliver risk-adjusted returns that are not only competitive, but in many cases superior to traditional investment strategies.

The study challenges the widely held assumption that generating financial alpha and driving measurable impact are mutually exclusive. Instead, it finds that with the right approach and due diligence, investors can align portfolios with meaningful environmental and social outcomes without sacrificing financial performance.

The report analyzed 257 companies whose business models are directly tied to solving pressing global challenges — from climate change to equitable healthcare and sustainable infrastructure. These firms were assessed using asset pricing models and regression analysis, and their performance was compared with traditional equity indices.

Key findings:

These findings signal that positive impact investing is not only viable but potentially advantageous for long-term, risk-conscious investors.

Also Read: Best Renewable Energy Stocks

To put this in context, consider the standard broad equity indices — such as the MSCI World or S&P 500 — designed to capture market performance without regard for social or environmental value creation. While they have historically provided consistent returns, they also carry exposure to sectors or companies that may pose reputational, regulatory, or sustainability-related risks.

By contrast, positive impact investing portfolios in the study achieved:

The implication is clear: prioritizing measurable impact does not hinder performance — it may in fact enhance it when supported by strong fundamentals.

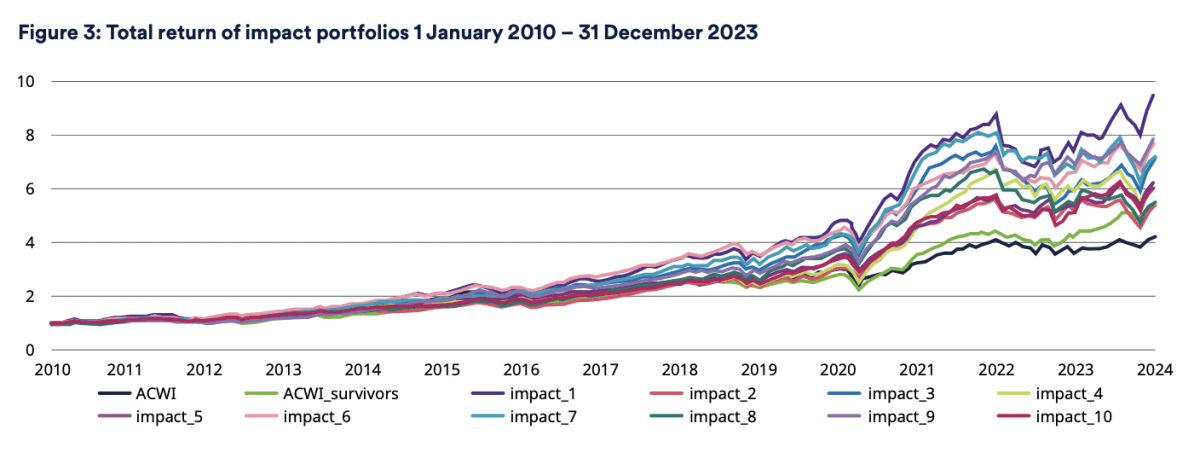

In their research, the authors examined the raw total return performance of 10 randomly selected impact portfolios containing 40 equally weighted firms to be picked across multiple portfolio from the approved 257 impact firm universe and compare their performance to the MSCI ACWI IMI (All Country World Investable Market Index with roughly 8,400 constitutents).

The following chart illustrates the outperformance of impact portfolios. Out of the 10

impact portfolios, only two underperform the ACWI IMI over the 2010-2023 period. Several of the impact portfolios outperform the ACWI survivors considerably.

Source: In focus – Impact and Financial Performance. Evidence from listed equities

One of the companies highlighted in the study is Schneider Electric, a global leader in energy management and automation. The company develops technologies that enable buildings, data centers, and industrial facilities to operate more efficiently, reducing energy waste and carbon emissions.

Its core business activities are tightly aligned with the UN Sustainable Development Goals, especially in areas related to energy transition and climate action. Schneider Electric demonstrates that positive impact investing does not require compromising on profitability. The firm has delivered robust earnings growth, maintains high operating efficiency, and consistently ranks among ESG leaders globally.

This case exemplifies how businesses solving real-world problems can also outperform on traditional financial metrics — reinforcing the thesis that positive impact investing is compatible with long-term value creation.

The research identifies several financial and operational characteristics common to high-performing impact firms:

Sectors such as information technology, healthcare, materials, and industrials were among the strongest contributors to performance within the positive impact investing universe.

Also Read: Best EV Stocks

As regulatory frameworks evolve and stakeholder expectations rise, integrating impact considerations into investment strategies is no longer a fringe concept. Positive impact investing is increasingly recognized as a driver of sustainable, long-term value, not just a values-based add-on.

“This research challenges the persistent belief that purpose-driven investing compromises financial performance,” said Amir Amel-Zadeh, Director of the Oxford Rethinking Performance Initiative. “By integrating impact metrics with traditional financial analysis, it becomes clear that positive impact investing can be a source of competitive advantage.”

Despite the promising findings, the report also stresses the importance of rigorous analysis. Not every investment labeled as “impact” will generate alpha. A clear framework for measuring and monitoring impact outcomes — combined with sound financial due diligence — is essential.

“For investors that get this right, aligning financial strength and impact could not just deliver positive purpose outcomes but an investment return edge as well,” said Maria Teresa Zappia, Global Head of Impact at Schroders.

This underscores the need for robust methodologies when constructing and evaluating positive impact investing strategies.

This comprehensive study affirms that positive impact investing in listed equities is not just an ethical imperative — it’s a strategic advantage. With the right data, disciplined portfolio construction, and a long-term outlook, investors can build portfolios that are both financially competitive and deeply aligned with global progress.

The message is clear for a generation of investors looking to align their money with their values: you no longer have to choose between doing well and doing good. With positive impact investing, you can achieve both.