Ralph Lauren (RL 📈) is proving that premium brands, disciplined execution, and responsible operations can coexist. With improving margins, strong earnings growth, and a Ziggma Score of 79, the company combines financial momentum with an Impact Score of 71. That makes RL a rare blend of shareholder return potential and credible corporate responsibility in global apparel.

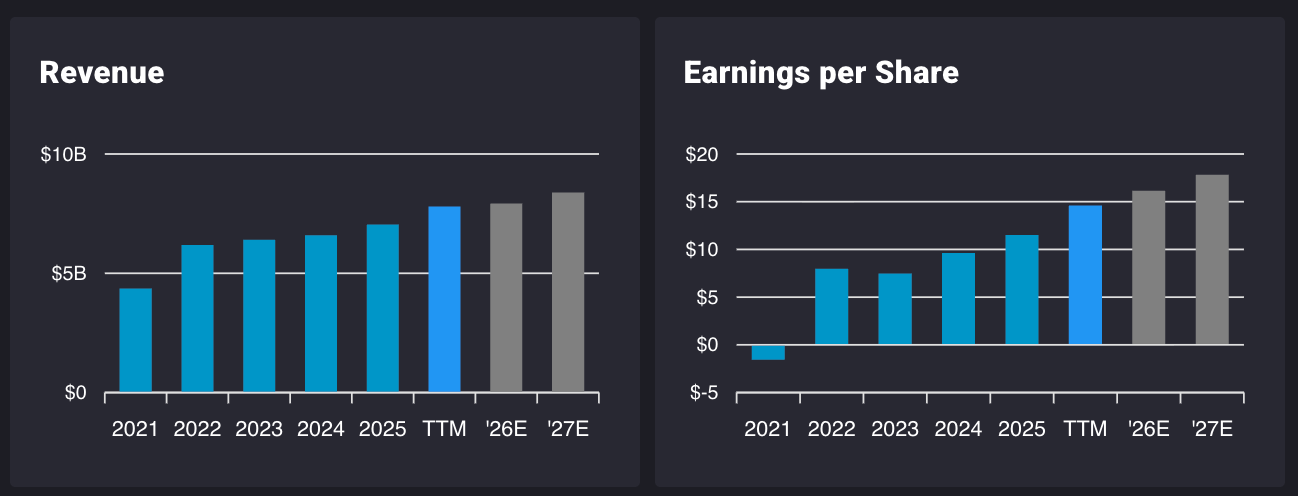

Ralph Lauren is delivering accelerating profitability, with earnings per share up 34.2% in the last twelve months and return on equity climbing to 33.8%. With profit growth forecast at 40% for next year and shares trading around 22x earnings, the setup supports continued upside if execution holds.

RL earns a 71 Impact Score, driven by a top score for its global warming potential of just 1.5°C and a 98 score for gender equality. Strong labor practices and high data privacy standards position the company as one of the more responsible operators in global fashion.

Ralph Lauren is a global lifestyle and apparel company best known for its Polo brand. The company designs and sells clothing, footwear, accessories, and home products across premium and luxury segments. Its distribution spans direct online channels, flagship stores, department stores, and select wholesale partners worldwide.

What makes RL different is brand depth. Few fashion companies command similar recognition across decades, demographics, and price tiers. From entry level Polo shirts to high end Purple Label tailoring, the brand occupies multiple layers of consumer spending.

Unlike fast fashion retailers chasing trends, Ralph Lauren focuses on timeless design. This reduces markdown risk and inventory volatility. A classic navy blazer or Oxford shirt does not go out of style in one season. That durability supports pricing power.

The company has also leaned into direct to consumer channels. More sales now come from owned stores and e commerce, improving margins and strengthening customer relationships.

The global premium apparel market continues to expand, supported by rising middle class wealth and global brand demand. While fashion is competitive, brand equity acts as a moat. Consumers buying Ralph Lauren are often buying identity and heritage, not just fabric.

The company’s improving return on assets, now at 12.3%, and expanding profit margins suggest that this moat remains intact.

This stock is part of our list of best sustainable stocks for 2026.

Ralph Lauren’s financial trajectory is going from strength to strength.

Over the past five years, revenue growth has stabilized and reaccelerated. Revenue rose 12.7% in the last twelve months. More importantly, profitability has strengthened meaningfully. Net profit margin has climbed to 11.7%, while operating cash flow margins reached 14.4%.

Return on equity now stands at 33.8%, up significantly from earlier years. That signals efficient capital allocation and improving brand monetization.

Debt levels remain moderate. Debt to equity has declined to 0.4x, and interest coverage exceeds 22x. The company generates sufficient earnings to comfortably service obligations. A payout ratio around 23% leaves room for reinvestment and dividend growth.

Shares trade at roughly 22x forward earnings. That is not cheap compared to the broader market, but it reflects improving growth and margin expansion.

The Ziggma Score of 79 reflects strong growth and financial health sub scores of 83 and 67 respectively. The valuation sub score of 38 signals that the stock is not a deep value play. Instead, investors are paying for quality and momentum.

Analyst targets imply approximately 18% upside toward $416 per share. If earnings continue to compound at double digit rates, multiple expansion could provide additional lift.

Management continues to prioritize premiumization, international expansion, and digital channels. Higher average selling prices and disciplined cost control support margin growth. Brand elevation in Asia and Europe remains a multi year opportunity.

If revenue grows near 10% annually and profit margins hold or expand modestly, earnings growth above 15% annually is realistic. Combined with a stable valuation multiple, that supports attractive shareholder returns.

Fashion demand can weaken during economic slowdowns. Premium brands rely on discretionary spending. Currency movements can affect international results. Competitive pressure from other luxury houses remains intense. A misstep in inventory planning could pressure margins. Finally, valuation leaves less room for disappointment.

Even accounting for these risks, current fundamentals suggest upside potential in the high teens over the next two to three years, with additional gains if growth surprises to the upside.

The apparel industry faces scrutiny over environmental impact, labor practices, and resource use. Ralph Lauren is not perfect, but its impact data shows meaningful progress.

The company earns a climate score of 70, driven by a global warming potential of just 1.5°C. Carbon intensity remains an area for improvement relative to peers, but emissions reduction trends are positive. Renewable energy use stands above 60%, signaling strong commitment to climate action.

RL scores 66 in fair labor practices, supported by strong employee ratings and a 98 score in gender equality. Supply chain oversight remains critical in global fashion. Continued transparency and enforcement will determine long term credibility.

Premium pricing often attracts criticism. Is it ethical to charge high prices for clothing? In a capitalist model, pricing power reflects brand value and consumer choice. Higher margins can fund sustainability investments, supply chain improvements, and employee benefits. The key is whether profits are reinvested responsibly. RL’s improving environmental and social metrics suggest it is moving in that direction.

Ralph Lauren combines brand durability with improving financial performance. Earnings growth above 30%, rising margins, and disciplined capital allocation create a strong foundation for value creation.

Over the next two to three years, upside can come from three drivers.

First, continued earnings growth supported by premiumization and direct sales.

Second, stable or modestly expanding valuation multiples as investor confidence builds. Third, dividend growth supported by strong cash generation.

At the same time, the company demonstrates measurable positive impact in climate action, labor practices, and governance standards. For investors seeking profits aligned with responsible business conduct, RL fits the profile.

Ralph Lauren is not a speculative turnaround story. It is a high quality global brand that has regained momentum. With strong profitability, manageable debt, and accelerating earnings, the financial case stands on solid ground.

Add an Impact Score of 71 and leadership in climate targets and gender equality, and RL earns its place in the good stocks universe. For long term investors who care about both returns and responsibility, this classic American brand still has room to grow.

Disclaimer

This document is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.