The market prices Accenture (ACN 🔎) at a record low valuation. At the same time, bookings are at record highs. Is this a major opportunity or a value trap?

ACN is trading at its lowest known valuation. At its peak in 2021, the stock was 2.5x more expensive. This is not a cyclical dip. This is a full re-rating.

The market is pricing Accenture like a business in structural decline due to the threat to its business from AI. Yet bookings are at record highs, AI demand is accelerating, and margins are expanding.

That disconnect is where the opportunity sits. The question is simple. Is AI replacing Accenture or making it indispensable? We’ve done the research.

At the same time, this is a company with a positive real-world footprint. A 1.4°C temperature alignment, 93% renewable energy usage, and strong labor metrics place it firmly in the GoodStocks universe.

Source: Ziggma

If Accenture re-rates from 14x to just 20x earnings, investors could see ~40–50% upside excluding dividends and the impact of its $9bn share buyback program.

With a 1.4°C temperature alignment and 93% renewable energy, Accenture is both reducing its footprint and enabling others to do the same.

Accenture is the partner companies call when transformation cannot fail. With over 700,000 employees, it helps governments and global enterprises redesign how they operate. Today, that increasingly means AI. This is not about installing a tool. It is about rebuilding the operating system of a company.

The bear case assumes that AI commoditizes consulting. That logic holds if AI were like previous enterprise software waves. But it is not. ACN has faced the “in-housing” threat before. Many analysts predicted that once installed ERP systems would make a big part of Accenture’s business obsolete. It did not. What’s more, while SAP was a “Record-Keeping” revolution, AI is a “Decision-Making” revolution. The complexity difference is massive.

AI is a different beast entirely.

We are moving from a world of record-keeping to a world of decision-making. Unlike the deterministic logic of an ERP, AI is inherently probabilistic. It doesn’t give you a “correct” answer; it gives you an “85% certain” answer. This shift changes the consulting relationship from a one-time installation to a permanent necessity.

In the SAP era, data was clean and structured. In the AI era, the “fuel” is the chaotic mess of an enterprise’s unstructured history—PDFs, emails, Slack messages, and video logs. You cannot simply “plug in” an AI agent and expect it to work; you have to re-architect the entire data core of the company. This is the “Last Mile” problem that individual CEOs cannot solve in-house.

Furthermore, the risks have scaled with the rewards. If an SAP module glitched, a line item was off. If an AI agent glitches, it hallucinates, leaks proprietary data, or introduces systemic bias into a supply chain. This creates a massive “Liability Shield” for Accenture. Fortune 500 boards aren’t just paying for code; they are paying for a “throat to choke”—a trusted partner to manage the constant “model drift” and security vulnerabilities that come with autonomous intelligence.

The market treats AI as a tool that replaces the consultant. In reality, the probabilistic, unstructured, and high-risk nature of AI makes the consultant more essential than they were during the cloud or ERP booms.

This is why in-housing is harder than it looks.

Running a chatbot internally is easy. Rewiring decision-making across a Fortune 500 company is not.

Accenture sells that complexity. And more importantly, it sells accountability when things go wrong.

This stock is part of our list of best sustainable stocks for 2026.

The most important signal is not growth. It is margins. Margins are expanding, not collapsing. If AI were destroying Accenture’s business model, margins would be compressing.

Instead, operating margin increased to 13.8%, from 13.5%. Gross margin improved to 30.3%, from 29.9%. It shows that Accenture is capturing efficiency gains from AI rather than passing them entirely to clients.

Accenture reported $22.1B in quarterly bookings with a book-to-bill ratio of 1.2x. That means demand is growing faster than revenue. AI-related bookings hit $2.2B in a single quarter and continue to scale. Companies are not cutting consultants. They are hiring them to navigate AI.

The Ziggma Score of 99 confirms the strength of the business:

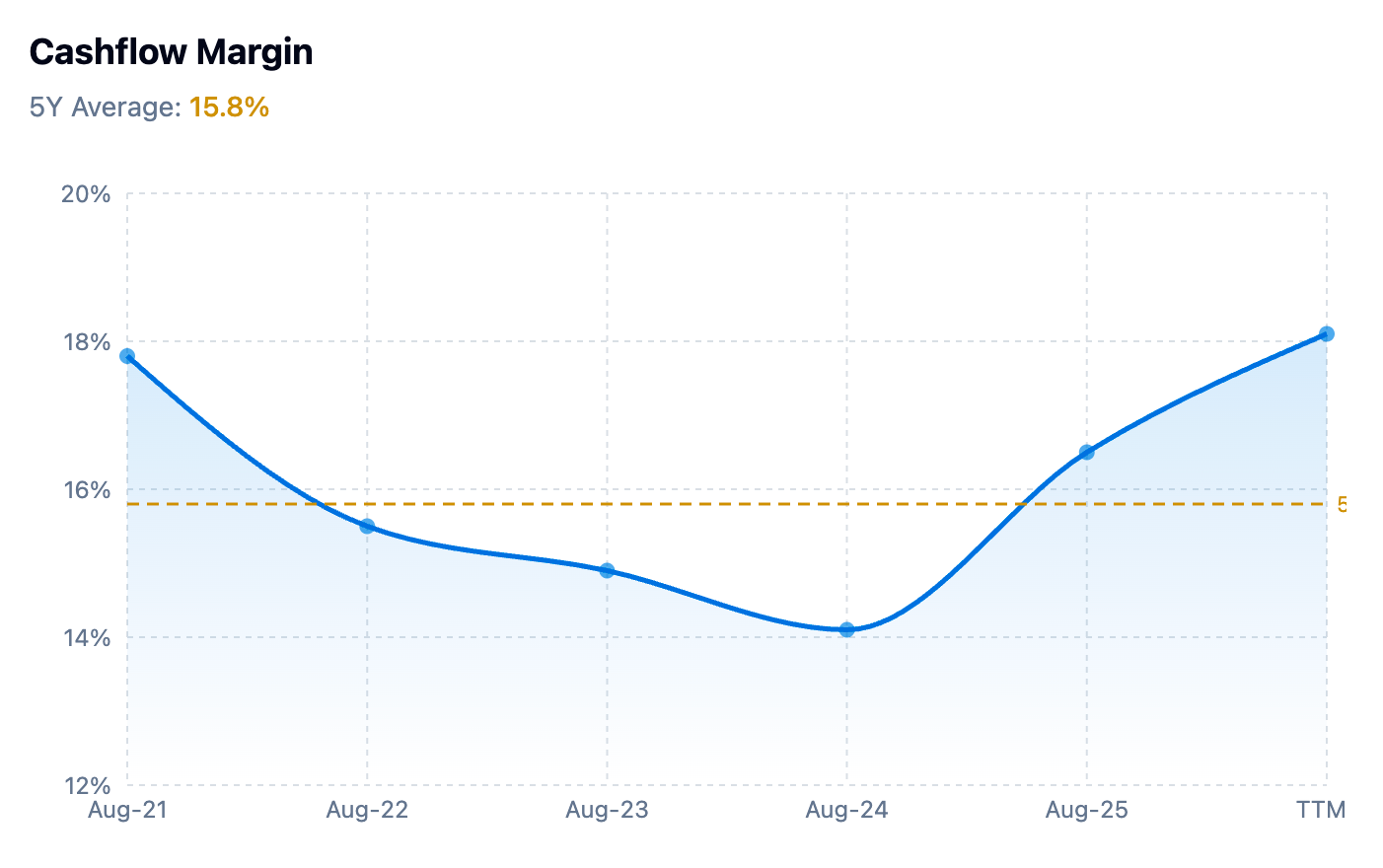

Return on assets is bouncing back. Cash generation is extremely strong with cashflow margin picking up strongly.

Source: Ziggma

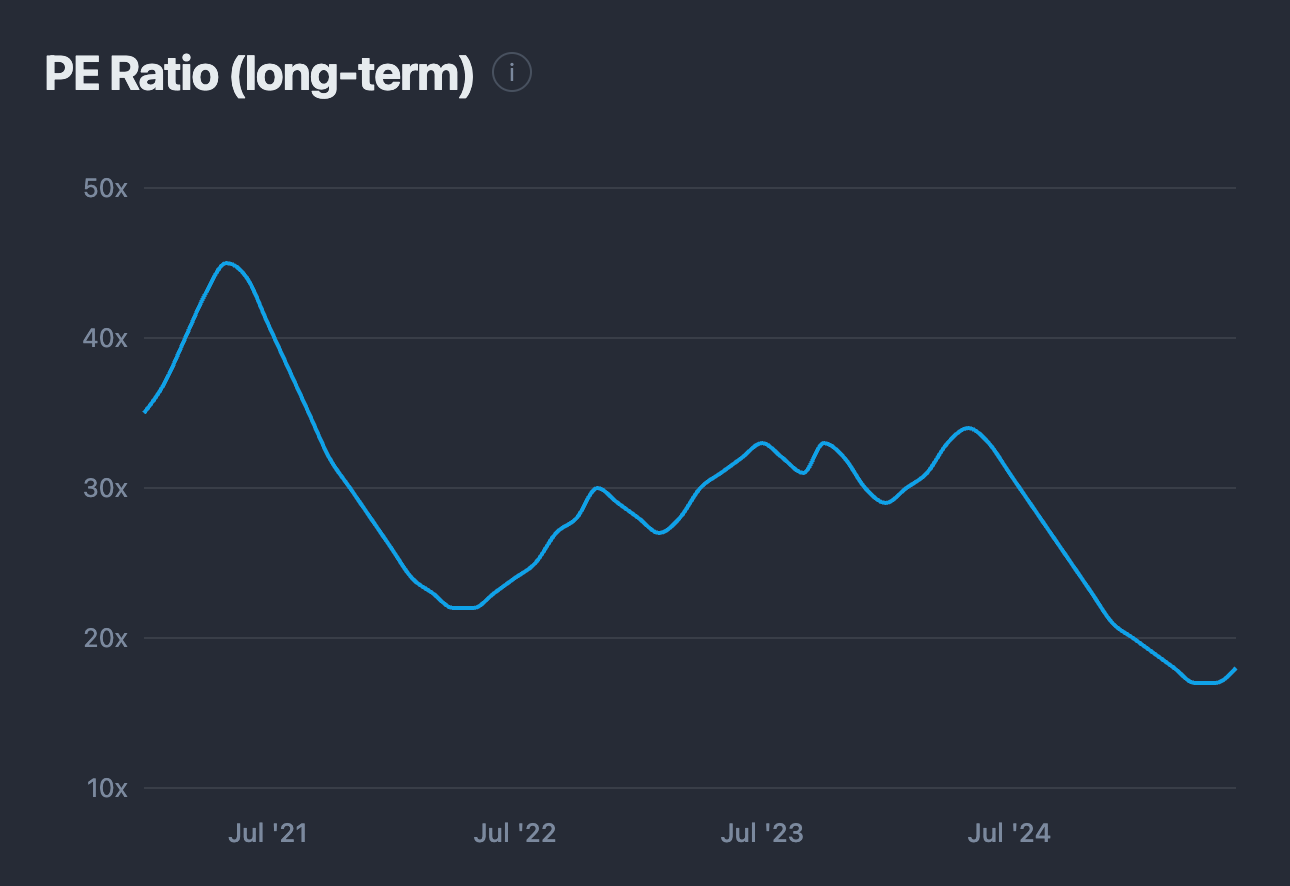

This is where the story really stands out. Accenture is currently trading at around 14x forward earnings, roughly half its long-term average of about 28x. The same pattern shows up across other metrics. The price-to-sales ratio sits near 1.9x versus a historical level closer to 3.3x. At the same time, the dividend yield has climbed to about 3.3%, well above what investors have typically received from this business.

Put simply, the market is pricing Accenture as if its best days are behind it. Yet the underlying data does not support that view.

Source: Ziggma

Analyst price targets currently point to around 28% upside. That alone is attractive. But it likely understates the real opportunity. The bigger lever is valuation. If Accenture merely re-rates to 20x earnings, still below its historical norm, the implied upside moves into the 40–50% range. A return to something closer to its long-term average around 25x would push potential gains above 70%. And importantly, this does not factor in dividends or ongoing buybacks, which add another layer of return on top.

The main risk is pricing pressure if clients demand lower fees as productivity increases. Some enterprises may attempt in-house AI builds, though complexity remains a barrier. Government spending cuts create near-term noise. Execution risk exists in shifting from time-based to value-based pricing.

Accenture is being priced like a melting ice cube while showing signs of becoming more efficient and more relevant. That gap is the opportunity.

Accenture’s impact is both direct and amplified. A 1.4°C temperature alignment places Accenture in the group of climate leaders. 93% of its energy comes from renewables, showing real operational progress. Carbon intensity remains controlled and continues to improve.

Source: Ziggma

Accenture’s biggest impact comes from what it enables. It helps companies:

When a company like Accenture improves a Fortune 500 supply chain, the impact is not incremental. It is systemic.

Employee ratings of 4.1 out of 5 indicate strong internal culture. Gender equality scores are high. Labor practices are solid. There are areas to improve in governance, but overall the company operates responsibly relative to peers.

The market is focused on whether AI reduces the need for consultants. The better question is whether AI increases the complexity of running a company. All current evidence points to the latter. At 14x forward profit, investors are being offered a high-quality company, expanding margins, strong demand, and growing relevance at a valuation usually reserved for declining businesses. That disconnect does not tend to last. For investors who want both return potential and positive real-world impact, ACN may just be one of these rare opportunities that doesn’t come around all that often.