Four independent data sources — Schroders and Oxford Saïd Business School, Corporate Knights, Morgan Stanley, and the Global Impact Investing Network — point to the same structural conclusion: impact-driven portfolios do not just keep pace with the market. They frequently beat it. Here is what the evidence shows, why the outperformance has structural roots, and where the honest caveats lie.

And here’s the kicker: Nearly all Gen Z (99%) Millennial (97%) investors say they want their money to make a difference. Together, they are projected to inherit $124 trillion in wealth over the next two and a half decades. That’s not just wealth transfer. That’s power transfer.

Meanwhile, plenty of investors cling to the old idea that doing good means giving up returns. But that’s changing fast.

So let’s break it down. Here’s what the numbers are really saying about making money and making impact.

Perception among private investors is shifting fast. Whether it’s gut instinct or growing evidence, more investors now believe sustainability pays. In 2025, 38% already say sustainable investments outperform traditional ones. More than half plan to increase their allocations next year. Only 3% plan to dial back.

Underlying conviction regarding the need for a more sustainable form of capitalism is strong. More than 80% of investors believe companies should address environmental issues, and over two-thirds say social issues should also be tackled.

Given that the Gen Y and Gen Z are projected to be on the receiving end of a $124 trillion wealth transfer over the next 25 years, impact investing could be a huge trend in the making.

What if the companies shaping a better world are also building the strongest portfolios? The evidence says: they are.

Widespread acceptance of the superiority of long-term, sustainability-focused business strategy in corporate value creation could be the game changer.

The potential for outsized returns through breakthrough solutions, for instance in energy storage, healthcare or recycling, is hardly the subject of debate.

In the following, we present three compelling pieces of evidence that doing well and doing good is anything but mutually exclusive.

A joint study by Schroders and Oxford Saïd Business School found that impact-focused equity portfolios didn’t just keep up. They often beat the market.

8 out of 10 randomly built 40-stock portfolios outperformed the MSCI ACWI IMI from 2010–2023. Some generated over 9% annualized alpha, with lower volatility and smaller drawdowns.

The bottom line – Doing good isn’t just morally sound. It’s a sound investment strategy.

Schroders pinpoints the drivers of this outperformance to a combination of strong business execution, including operational efficiency, more active capital deployment, and growth orientation.

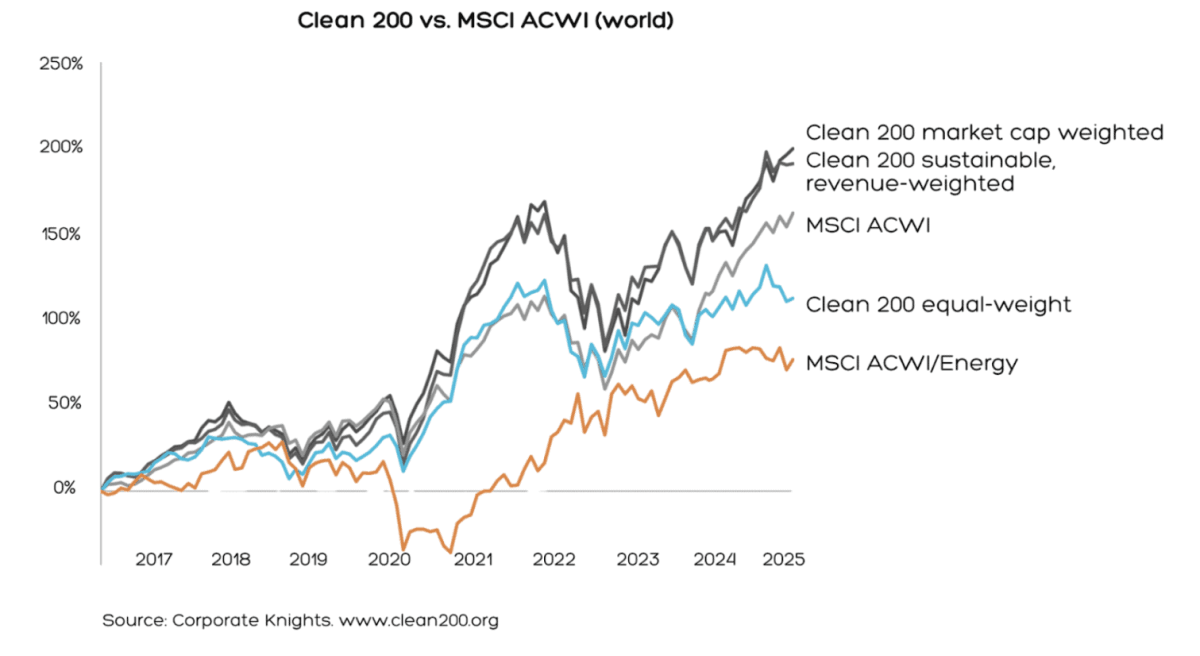

Take the Clean200 – a portfolio of the world’s most sustainable companies. Over the last eight and a half years, it’s crushed the MSCI World by 29% (191% vs. 162%).

The Clean200 Portfolio is compiled by Corporate Knights, a Toronto based B Corp. Its research division provides rankings and ratings that currently serve investors representing $15 trillion in assets under management.

These Clean200 companies don’t just talk sustainability. They sell it. On average, 55% of their revenue comes from sustainable lines of business, compared to just 16% in the broader market.

The resilience argument got a live test in early 2025. During the April tariff-driven market selloff — when the MSCI ACWI Large Cap Net Return Index fell 5.44% — global large-cap sustainable funds declined just 1.32% on average. That gap between -5.44% and -1.32% is not a rounding error. It reflects the same lower-volatility characteristic that the Schroders/Oxford study identified in its 2010–2023 data."

Morgan Stanley's latest analysis adds another layer. In the first half of 2025, sustainable funds generated median returns of 12.5% versus 9.2% for traditional funds — the strongest period of outperformance since Morgan Stanley began tracking data in 2019. Over the longer run, a $100 investment in a sustainable fund in December 2018 would be worth $154 today, compared to $145 in a traditional fund. The H1 2025 data is particularly notable because it coincided with a volatile, tariff-driven market selloff — a period when defensive quality tends to matter most. Doing the right thing has literally paid off.

Sustainable funds invest in companies that meet environmental, social, and governance (ESG) standards, aiming to generate financial returns while promoting positive impact.

The Global Impact Investing Network's State of the Market 2025 report, drawing on 429 organizations across 54 countries, adds the broadest cross-sectional evidence. Impact AUM has grown at 21% compound annual growth rate over six years, compared to just 5% for total AUM — capital is flowing toward impact at four times the rate of the broader market. More directly relevant to the returns question: 90% of impact investors reported meeting or exceeding their financial expectations, and 88% met or exceeded their impact goals. The market now stands at $1.571 trillion in AUM, the first time it has crossed the $1.5 trillion mark.

The evidence above is not a straight line. In 2024, US sustainable funds experienced $19.6 billion in outflows — their second consecutive year of net redemptions — and only 42% of sustainable funds finished in the top half of their Morningstar category.

The primary culprit was rising interest rates, which hit clean energy stocks and other long-duration growth names particularly hard. Academic literature adds further nuance: some peer-reviewed work finds that once you adjust impact fund returns for market beta, the alpha narrows or disappears.

The Schroders/Oxford finding is therefore the most important piece of evidence in this article — it is one of the few studies that explicitly measures both alpha and volatility together, finding outperformance alongside lower drawdowns, not instead of risk control. One difficult year in a rate-driven environment does not invalidate a structural thesis. But investors should hold the evidence clearly: the long-run case is strong; short-run performance is subject to the same macro forces as any equity strategy.

So what’s behind this consistent outperformance? Turns out, impact-driven companies share a few traits that set them apart.

Impact firms exhibit significantly higher operating margins, suggesting they are more efficient at generating profit from their core business operations compared to the benchmark.

Impact firms put capital to work. They tend to hold a lower percentage of cash to total assets, suggesting a more active capital deployment strategy.

Investors reward impact firms with higher valuation multiples – for good reason. Impact firms trade at higher valuations relative to earnings and cash flow, a common characteristic of growth-oriented firms.

Impact firms build more real stuff than the average company. A larger share of their assets consists of physical, tangible items like property, equipment, and inventory, rather than intangible assets such as goodwill, patents, or brand value.

This could mean they are in industries that require more physical capital (e.g., renewable energy, infrastructure, or manufacturing).

It could also indicate that they have less goodwill on their balance sheet, as they tend to be smaller and earlier stage, so may have fewer acquisitions.

Impact firms show higher employee growth, pointing to active expansion and investment in human capital.

The outperformance documented above reflects structural advantages that are not going away: large addressable markets, regulatory tailwinds, and a quality bias — impact leaders tend to be operationally efficient, growth-oriented, and disciplined with capital. Those characteristics compound. The $124 trillion wealth transfer projected over the next 25 years will direct trillions toward companies solving the biggest challenges of our time. The investors positioned earliest will benefit most.

The question is not whether impact and returns can coexist. The evidence answers that. The question is which companies combine genuine impact alignment with the financial quality to deliver on both — and that is exactly what Ziggma is built to surface.

→ See how your portfolio scores on real-world impact