After a roughly 30% pullback from recent highs, Agilent Technologies (👉 Ziggma profile) may now offer a compelling entry point into a business that quietly underpins modern medicine and scientific progress.

Agilent sits at the center of global healthcare, diagnostics, and scientific discovery. The market currently views it as a cyclical slowdown story. But that framing misses the bigger picture.

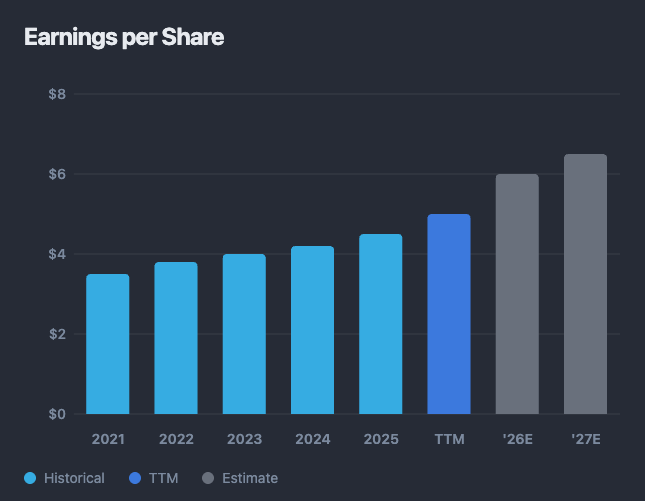

Earnings are expected to re-accelerate sharply, with projected EPS growth of 30.6% next year, while valuation has compressed to a much more reasonable 19.2x forward earnings.

This is not just a company that grows. It is a company that enables progress. From cancer research to food safety testing, Agilent supports systems that society depends on every day.

That combination places it firmly within the GoodStocks universe.

With earnings expected to grow by 30.6% next year and a forward multiple of 19.2x, Agilent offers a rare combination of recovery-driven growth and reasonable valuation.

Agilent enables drug development, cancer research, and food safety testing, making it essential to modern healthcare while maintaining responsible operations and resource efficiency.

Agilent Technologies is a global leader in analytical instruments, diagnostics, and life sciences tools. Its customers include pharmaceutical companies, hospitals, diagnostic labs, and environmental agencies.

In simple terms, Agilent builds the tools that scientists rely on to analyze and validate the world around us. Whether it is a new cancer treatment, a food safety inspection, or water quality testing, accurate measurement is essential. Agilent provides that precision.

The company operates in a market growing at roughly 6% per year, supported by long-term trends such as rising healthcare demand, aging populations, and increasing regulatory standards.

Its competitive advantage is deeply rooted. Agilent systems are embedded into laboratory workflows, making switching costly and disruptive. Over time, this creates a steady stream of recurring revenue through consumables and services.

Once a lab adopts Agilent equipment, it tends to stay.

Over the past few years, growth has clearly slowed. Revenue expanded at just 1.9% annually over five years, while earnings growth came in at 3.0%. Cash flow has also been uneven.

At first glance, this does not inspire confidence.

But the context matters. The slowdown reflects a period of digestion across the biotech and pharmaceutical ecosystem following a surge in activity during and after Covid. Funding tightened, customers paused spending, and growth temporarily stalled.

Importantly, the underlying business did not break. It paused.

The most important number right now is the expected 30.6% earnings growth next year.

This reflects a combination of recovering demand, disciplined cost management, and operating leverage. As volumes pick up, margins are likely to expand.

The earnings trajectory tells a clear story. After flattening in recent periods, estimates point to a meaningful step up. This kind of re-acceleration is often where strong returns begin.

Valuation is where the opportunity becomes more tangible.

The forward price to earnings ratio has come down to 19.2x, a notable shift from the 30x range seen in previous years. At the same time, the price to sales ratio sits around 5.4x, close to multi-year lows.

In other words, expectations have already been reset.

That creates room for upside if the recovery plays out as expected. Analysts currently see potential upside of around 44%, with a target price of $165.

Agilent’s Ziggma Score of 75 reflects a business that is consistently strong across key dimensions.

Profitability stands out with a score of 83, supported by solid margins and returns on equity above 20%. Valuation and financial health both score 75, indicating a balanced profile with no major weaknesses.

This is not a perfect company, but it is a high-quality one. And importantly, quality has not deteriorated during the slowdown.

The main risk is timing. A slower-than-expected recovery in biotech and pharma spending could delay the earnings rebound. Growth may remain muted in the near term, and competitive pressure from larger peers could weigh on margins. Currency fluctuations and global demand softness are additional factors to watch.

Agilent combines a resilient business model with a visible recovery path and a more attractive valuation.

That combination supports the case for double-digit annual returns over the medium term, especially if earnings re-acceleration materializes as expected.

Agilent’s impact is not always visible, but it is deeply embedded in systems that affect everyday life.

Agilent plays a critical role in enabling modern medicine. Its instruments are used in drug development, cancer research, and diagnostics. These tools allow scientists to understand diseases, develop treatments, and ensure that therapies are safe and effective.

Without this layer of scientific infrastructure, progress in healthcare would slow significantly.

Beyond healthcare, Agilent contributes to food safety and environmental protection. Its technologies are used to detect contaminants in food, monitor water quality, and analyze pollutants.

This work helps reduce health risks, improve public safety, and support regulatory standards across industries.

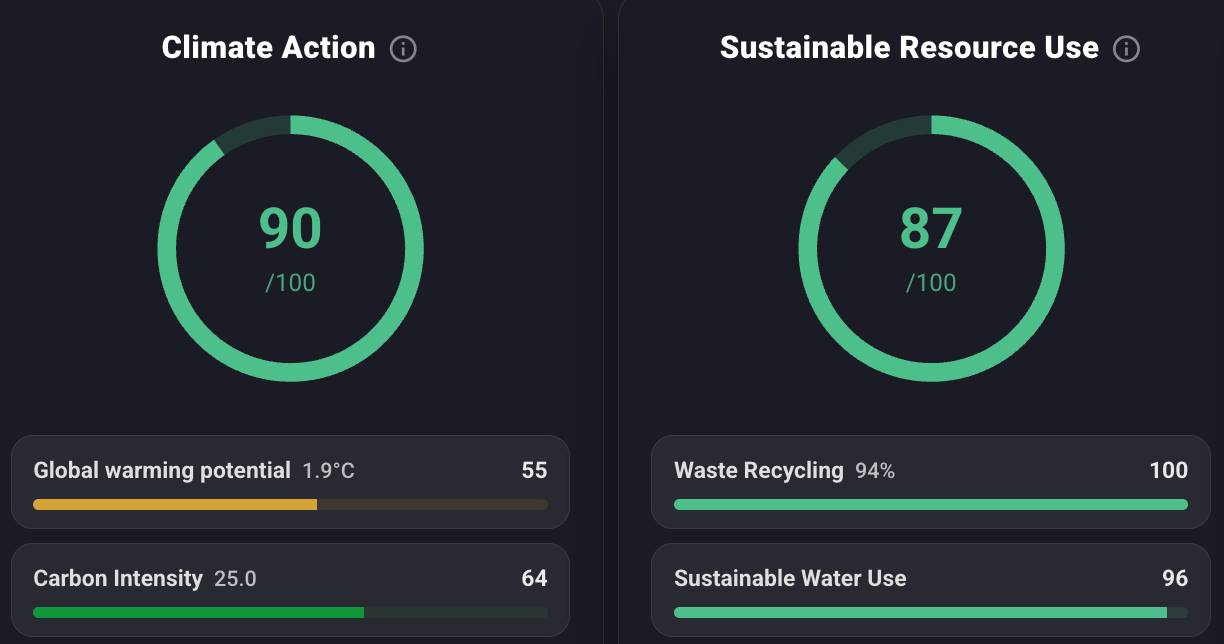

Agilent also shows signs of responsible operations. The company has made progress in improving resource efficiency and maintaining high waste recycling rates across its operations. It aligns with broader climate goals, even if it is not a pure-play environmental company.

Its contribution is indirect but meaningful. By enabling better testing and more efficient systems, Agilent helps reduce waste and improve outcomes across entire industries.

Agilent is a reminder that some of the most impactful companies are not always the most visible.

It operates behind the scenes, enabling breakthroughs in healthcare, ensuring food safety, and supporting environmental monitoring. At the same time, it maintains strong fundamentals and a resilient business model.

Right now, the market is focused on short-term softness. But beneath that, the conditions for re-acceleration are building.

With earnings set to recover and valuation at more reasonable levels, Agilent offers a compelling combination of return potential and real-world impact.

For investors looking to align performance with purpose, this is a stock worth serious attention.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.