When we first covered First Solar (FSLR 🔎), the core idea was simple: First Solar is not just a solar stock. It is one of America’s most strategic clean energy manufacturers.

That thesis still holds. The latest earnings call added fresh numbers and a sharper picture. First Solar delivered a strong start to 2026, with Q1 net sales of $1.04B, up 24% year over year, and earnings per share of $3.22, up 65% year over year. Management also reaffirmed full-year guidance.

The market still treats First Solar like a volatile clean energy trade. The numbers increasingly look like a high-quality industrial growth business with a climate-critical mission. That tension is exactly why FSLR deserves a fresh look.

Source: Ziggma

First Solar combines growth, backlog visibility, strong margins, and a valuation that still looks reasonable relative to earnings power. Analysts see roughly 34% upside to $284, while Ziggma shows a very moderate forward P/E of 12.1x and projected 2026 profit growth of 23%.

First Solar is an existential problem solver. Its core product helps decarbonize the power grid, and ACA Ethos data points to a 1.3°C climate pathway, 82% waste recycling, and strong resource-use performance.

First Solar is the leading U.S.-based solar module manufacturer. Its technology differs from most global peers because it uses thin-film cadmium telluride technology rather than conventional crystalline silicon. That distinction matters.

As we highlighted in our previous post, First Solar is not only selling solar panels. It is building a domestic clean energy supply chain at a time when energy security, AI electricity demand, and U.S. industrial policy are all moving in its favor. The company’s footprint includes manufacturing in the U.S., India, Malaysia, and Vietnam. Its U.S. position is especially important because customers increasingly value domestic sourcing, tariff insulation, and policy eligibility.

First Solar’s Q1 numbers were solid. Net sales rose 24% to $1.04B, driven by higher module volumes. Net income reached $347M, or $3.22 per diluted share, up from $210M and $1.95 a year earlier. Adjusted EBITDA came in at $520M, compared with $379M in Q1 2025.

That is not a broken growth story. It is a business still scaling through a noisy policy environment.

The biggest update from the earnings call was that management reaffirmed 2026 guidance. The company still expects 17.0 GW to 18.2 GW of volume sold, $4.9B to $5.2B in net sales, and $2.6B to $2.8B in adjusted EBITDA. This is important because the stock had previously come under pressure after revenue guidance disappointed the market. Reuters reported that the earlier sell-off reflected customer headwinds, permitting delays, and an expected $125M to $135M tariff impact in 2026.

So the setup has changed. The risk is not gone. But the earnings call showed that First Solar is delivering.

One of the strongest parts of the FSLR story remains backlog. The company ended Q1 with 47.9 GW of contracted sales backlog. That’s over 2.5x annual installed capacity. In our previous report, we emphasized multi-year visibility as a key pillar of the investment thesis. That remains true, even though backlog is down from earlier levels.

The key point is visibility. In a volatile energy market, contracted demand through future years gives First Solar something many clean energy companies lack: a clearer path to revenue conversion.

Ziggma data shows FSLR trading at 12.6x 2026 earnings, with projected 2026 profit growth of 22%. That combination is unusual. The stock is not priced like a high-growth climate infrastructure leader. It is priced more like a cyclical manufacturer with policy risk. That creates the opportunity. If First Solar continues to convert backlog, maintain margins, and benefit from domestic manufacturing incentives, the current valuation may prove too low. Analyst targets imply 29% upside to $284, which gives the stock a meaningful re-rating path.

Policy uncertainty remains the biggest risk. Tariffs, tax credit rules, and permitting timelines can all affect customer behavior. Manufacturing ramp-ups can also create execution risk. Finally, solar remains a competitive and politically sensitive industry.

First Solar still offers one of the strongest combinations in clean energy: visible demand, high margins, net cash, and a valuation that does not fully reflect its strategic importance.

First Solar’s impact case is unusually clear. The company makes solar modules. Those modules help utilities add clean power at scale. That matters even more today. AI, electrification, and industrial growth are driving electricity demand higher. The world needs more power, but it also needs that power to be cleaner. First Solar sits directly inside that challenge. This is why, as we argued in the previous FSLR report, the company belongs in the GoodStocks universe as an Existential Problem Solver.

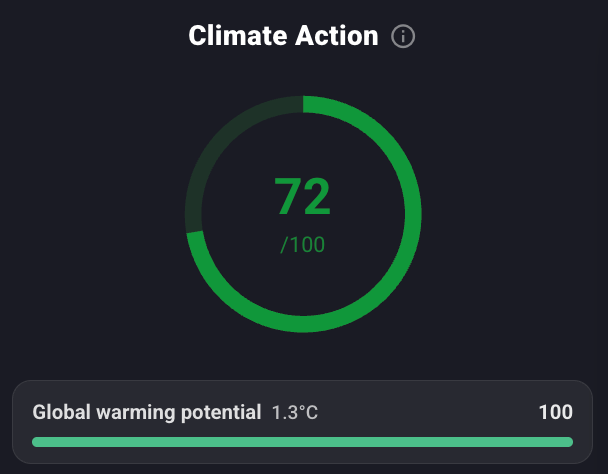

ACA Ethos data reinforces the impact story. First Solar shows a 1.3°C global warming potential, a Climate Action score of 72, and a strong Sustainable Resource Use score of 83.

Source: Ziggma

The resource-use details are notable: 82% waste recycling, 75 on sustainable water use, and 100% energy from renewables. These numbers strengthen the case that First Solar is not only selling climate solutions. It is also improving its own operating footprint.

The impact profile is strong, but not perfect. Fair Labor Practices score 58, while Accountability is 40. Employee rating is solid at 3.8/5, and gender equality scores well at 89, but accountability metrics, fines and violations, and governance-related measures leave room for improvement. That balance is important. First Solar is not flawless. But it is one of the clearer examples of a company where the core business model directly supports climate progress.

Our previous report framed First Solar as a rare company sitting at the intersection of clean energy, U.S. manufacturing, and long-term shareholder value. The latest earnings call strengthens that view. Q1 confirmed strong growth. Guidance was reaffirmed. Backlog remains large. Margins are strong. And the valuation still looks surprisingly modest for a company with this level of strategic relevance. Policy risk may the stock volatile. But volatility is not the same as a broken thesis.

First Solar remains a classic GoodStock: a company where profit and positive impact reinforce each other. It helps solve one of the world’s biggest problems while building a business with real earnings power.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.