Every major computing shift - from cloud to AI - runs on memory. As data volumes explode and AI models grow more complex, demand for high-performance memory is accelerating rapidly. Micron Technology (MU 📈) sits at the center of that transformation, supplying the DRAM and NAND chips that power data centers, AI accelerators, and energy-efficient devices worldwide.

After enduring one of the deepest semiconductor downturns in decades, Micron is now emerging into a sharply improving environment. Supply discipline has returned, pricing is recovering, and profitability is rebounding fast, setting the stage for both strong shareholder returns and meaningful real-world impact.

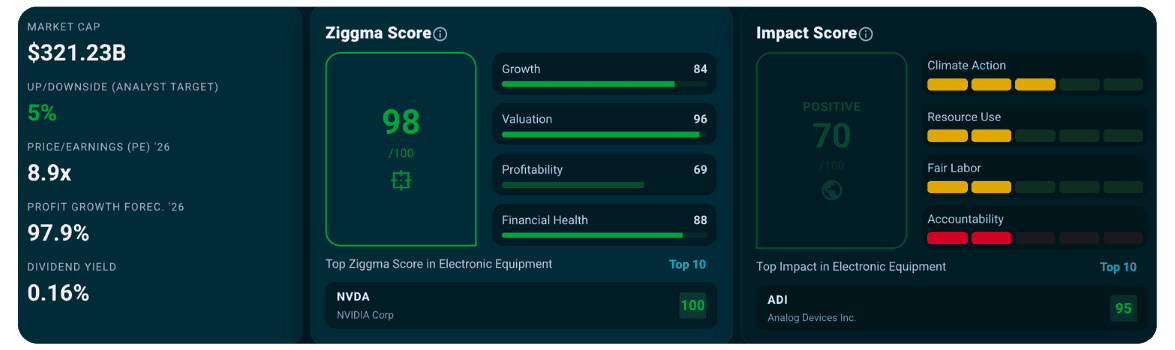

Micron’s earnings recovery is already visible in the numbers. With forward P/E of just 8.9x and profit growth forecast near 98%, the stock offers further upside as memory markets normalize and AI demand accelerates.

Micron enables more energy-efficient computing at global scale. Its advanced memory solutions reduce power consumption per unit of data processed — a critical lever for lowering the environmental footprint of data centers and AI workloads.

Micron is one of only a handful of companies globally capable of manufacturing advanced DRAM and NAND memory at scale. Unlike diversified semiconductor firms, Micron’s pure-play focus allows it to concentrate capital and R&D on pushing memory performance, density, and efficiency forward.

Micron’s portfolio spans DRAM for servers and AI applications, NAND for storage devices, and specialized memory for automotive and industrial systems. High-bandwidth memory (HBM) has become a key growth driver as AI accelerators demand faster data throughput with lower energy consumption.

The memory market is cyclical, but structurally growing. AI training, inference, autonomous driving, and cloud workloads are driving sustained demand growth. Micron’s moat lies in scale, capital intensity, and process expertise. These are strong barriers that limit new entrants and encourage industry-wide supply discipline.

Micron’s financials reflect the severity of the 2023 downturn, followed by a sharp rebound. After revenue declined nearly 50% at the trough, growth has surged back, with TTM revenue up 45% and EBITDA growth exceeding 76%. This snap-back highlights the operating leverage embedded in Micron’s model.

Margins have recovered quickly as pricing improves. EBITDA margins are back above 50% TTM, while return on equity has climbed to 22.6%, well above the five-year average. These metrics confirm that Micron is firmly exiting the downcycle.

Micron’s financial health stands out. Net debt to EBITDA is effectively zero, interest coverage exceeds 30x, and the current ratio remains well above 2x. The Ziggma Financial Health score of 88 reflects a balance sheet capable of supporting growth without excessive leverage.

Despite the earnings recovery, valuation remains conservative. The Ziggma Valuation score of 96 reflects pricing well below long-term averages, even as growth accelerates. Compared with historical multiples during upcycles, today’s valuation leaves room for meaningful expansion.

Consensus price targets imply only modest upside — but analyst estimates often lag early-cycle earnings revisions. With EPS growth forecast above 200% TTM and valuation still compressed, upside potential remains asymmetric if the cycle continues to strengthen.

Micron’s most significant impact comes from improving energy efficiency across computing infrastructure. Advanced DRAM and NAND reduce power usage per bit stored or processed — a crucial factor as data centers become one of the fastest-growing sources of electricity demand globally.

Micron scores well on labor practices, with strong employee ratings and gender diversity metrics. While accountability and climate metrics indicate room for improvement, transparency and operational discipline provide a foundation for progress.

Micron offers exposure to one of the most powerful investment setups in semiconductors: a cyclical recovery layered on top of secular AI-driven demand. Over the next two to three years, returns are likely driven by rapid earnings growth, improving margins, and potential multiple expansion as confidence returns.

Crucially, Micron’s technology enables more efficient data processing at scale — aligning shareholder value creation with broader societal benefits.

Micron is no longer fighting the cycle. It is riding it. With earnings rebounding, valuation still attractive, and AI-driven demand accelerating, MU offers investors a compelling return profile backed by real-world impact. When the memory cycle turns, disciplined leaders tend to outperform — and Micron is well positioned to do exactly that.

Important Notice

This article is not investment advice. We cannot predict whether the stocks mentioned in this article will go up or down.

We believe the information contained in this text to be reliable but do not warrant its accuracy or completeness. Opinions, estimates, and investment strategies and views expressed in this document constitute our judgment based on current market conditions available data and are subject to change without notice. Please consider your full financial situation prior to making an investment decision.