Edwards Lifesciences (EW 🔎) has quietly built one of the most important franchises in modern healthcare. Its minimally invasive heart valve technologies helped transform treatment for patients who once faced high-risk open-heart surgery. In the process, Edwards became a dominant force in structural heart care and a long-term stock market winner.

Now the company may be entering its next chapter. After years of explosive growth driven by transcatheter aortic valve replacement, or TAVR, investors have become worried about slowing procedure growth and rising competition. That concern pushed Edwards’ valuation far below the levels investors once paid for the stock.

Yet the long-term story remains intact. Edwards continues to post strong profitability, exceptional financial health, and expanding opportunities in newer structural heart markets like tricuspid valve disease. At the same time, the company remains one of the cleaner and more socially beneficial businesses in healthcare. Its products directly improve and extend lives while helping patients avoid invasive surgery and lengthy recovery periods.

That combination of durable healthcare demand, a powerful moat, and meaningful real-world impact clearly qualify Edwards Lifesciences for the GoodStocks universe.

Source: Ziggma

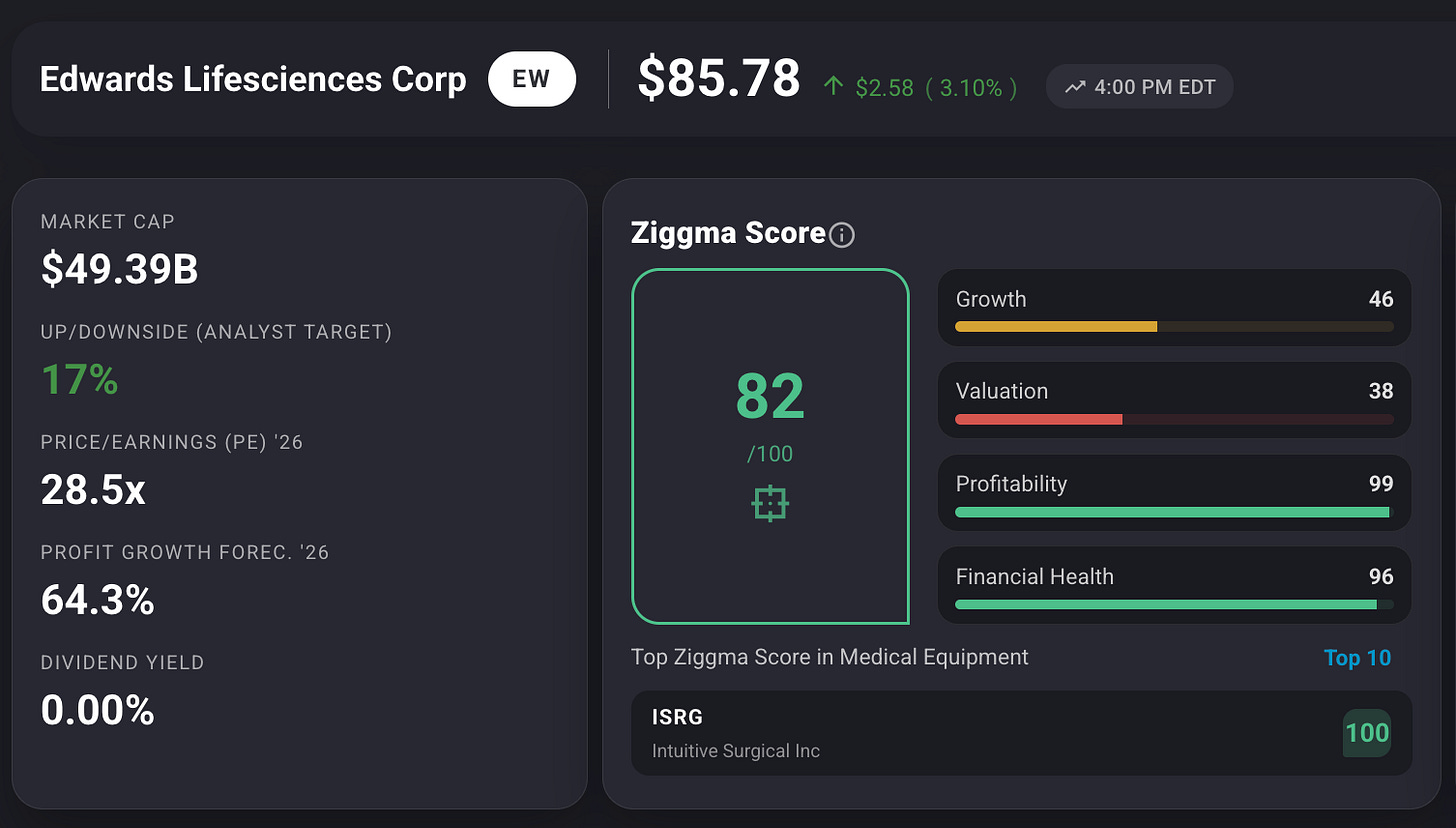

Edwards Lifesciences combines a long-term upward stock trend with exceptional profitability and financial strength. Earnings growth is forecast above 60% next year. The current valuation may underestimate the company’s next growth phase.

Edwards helps patients avoid open-heart surgery through minimally invasive valve therapies that improve survival and quality of life. Few healthcare companies create such direct and measurable patient impact while maintaining relatively low controversy and strong operational quality.

Edwards Lifesciences develops medical technologies focused primarily on structural heart disease and critical care monitoring. Its flagship products are transcatheter heart valves used to treat conditions such as aortic stenosis, a life-threatening narrowing of the heart valve that becomes increasingly common with age.

Traditionally, many patients required invasive open-heart surgery to replace damaged valves. Edwards helped pioneer a less invasive alternative that allows physicians to replace valves using catheter-based procedures. Recovery times are shorter, complication risks can be lower, and many elderly patients who were previously poor surgical candidates can now receive treatment. That innovation created one of the strongest franchises in medical technology.

The company’s moat is substantial. Physicians require extensive training to perform these procedures, hospitals invest heavily in specialized structural heart programs, and switching costs are meaningful. Clinical data, physician trust, regulatory expertise, and hospital relationships all reinforce Edwards’ leadership position.

Importantly, the market itself continues to expand. An aging global population means structural heart disease is likely to become more common over time. Unlike cyclical consumer markets, these procedures are medically necessary. Demand tends to remain resilient even during economic slowdowns.

And Edwards is no longer just a TAVR story. The company is increasingly expanding into newer structural heart categories, particularly tricuspid valve therapies. That transition may define the next phase of growth.

Edwards’ long-term stock chart tells an important story.

Over the past decade, the company created enormous shareholder value as TAVR adoption accelerated globally. But the stock also experienced sharp resets whenever investors feared slowing growth.

That is exactly what happened more recently. Concerns about moderating TAVR procedure growth, increasing competition, and tougher year-over-year comparisons pushed the stock’s valuation far below historical norms.

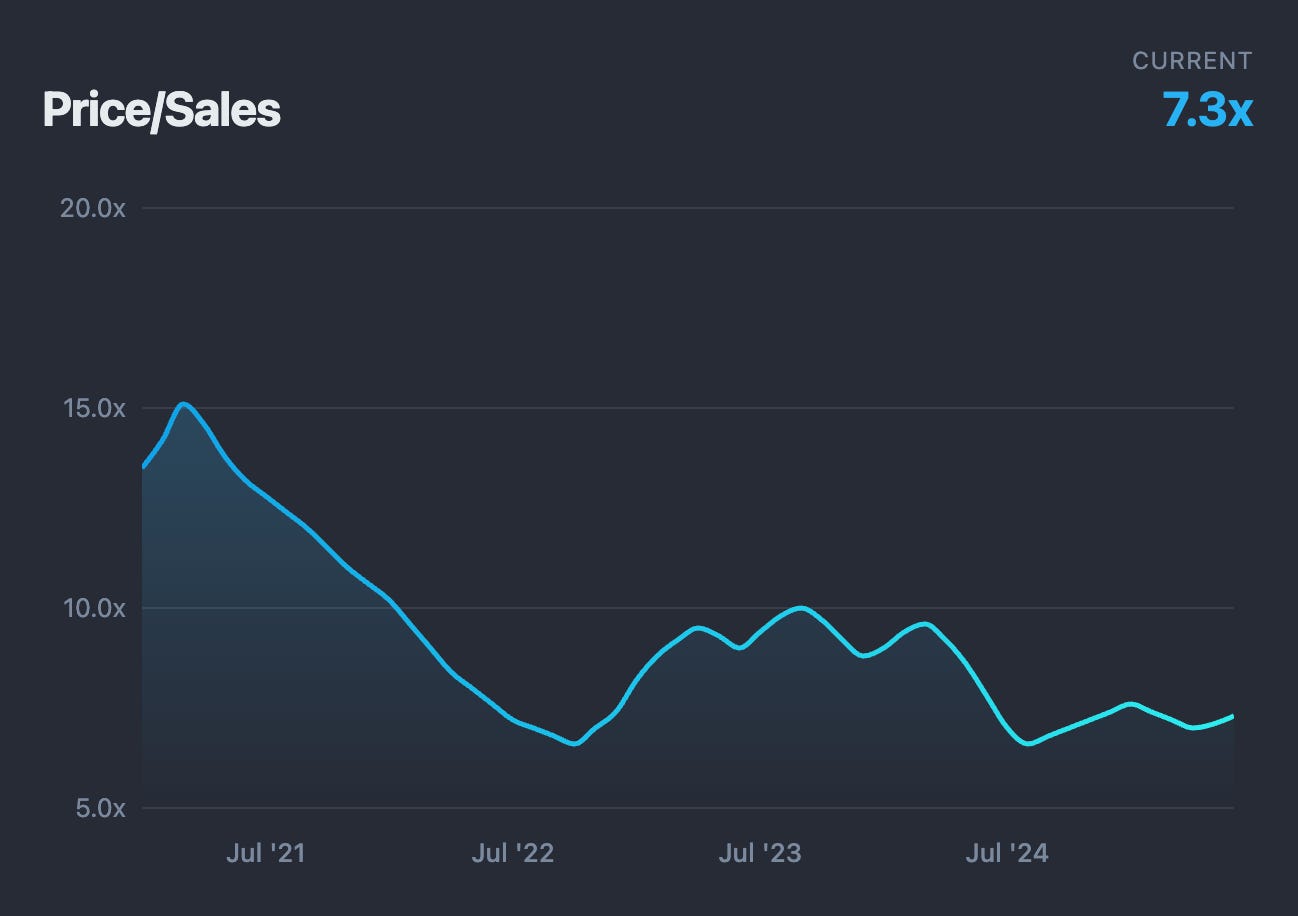

The compression is striking. Edwards historically traded at much higher earnings and sales multiples. Price-to-sales ratios once exceeded 15x. Today, the stock trades closer to 7.4x sales. Its long-term earnings multiple chart also shows a dramatic reset from prior peak valuations. In other words, investors are no longer pricing Edwards like a hypergrowth story. That may create opportunity.

Source: Ziggma

Despite the valuation reset, Edwards still generates elite financial metrics. The company carries a Ziggma Score of 82, supported by exceptional profitability and financial health subscores of 99 and 96 respectively.

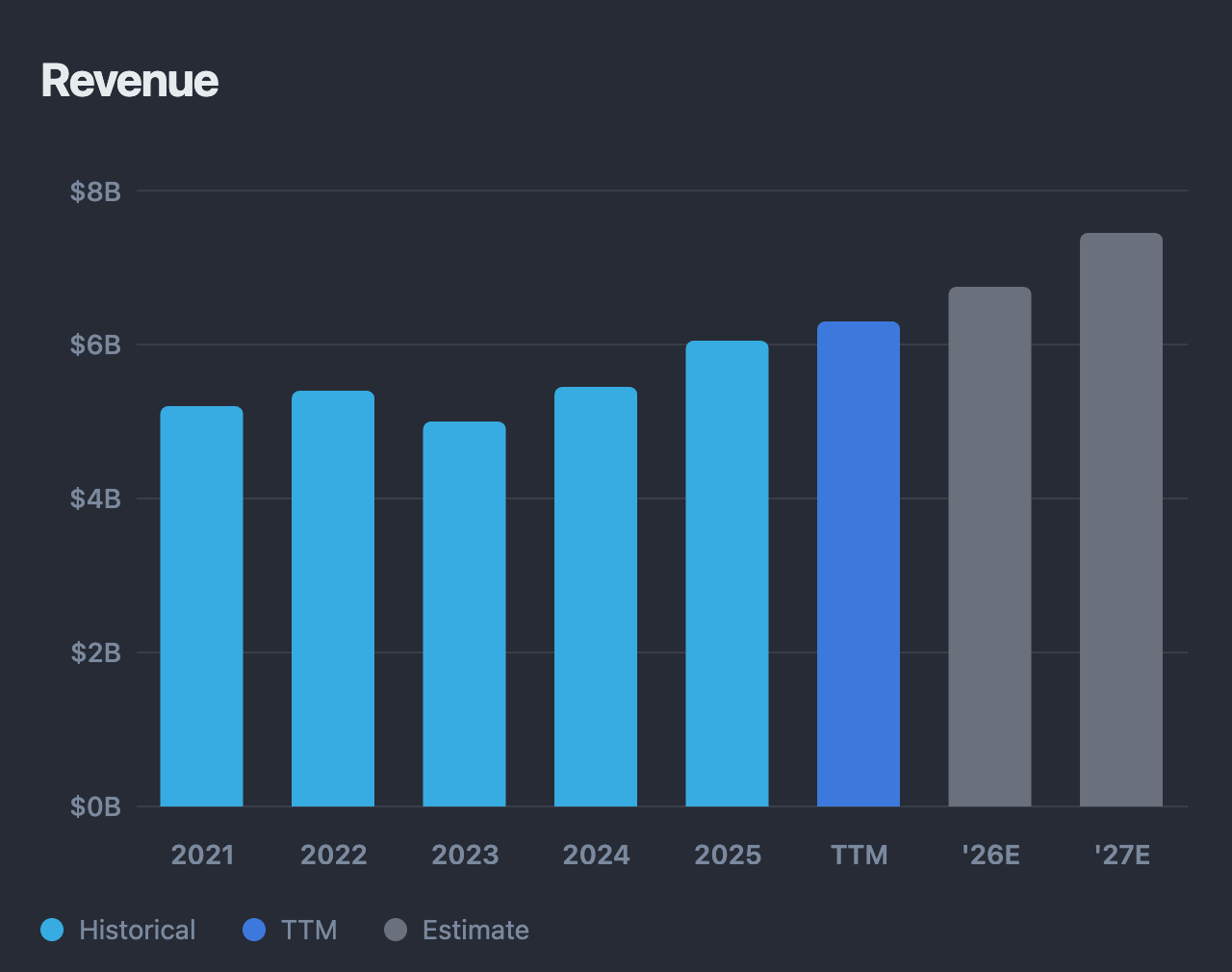

Revenue is projected to grow at double-digit rates in both of the next two years.

Source: Ziggma

Debt levels remain extremely low with debt-to-equity near 0.1x. Financial flexibility is one of Edwards’ major strengths.

Profitability also remains outstanding:

Very few healthcare companies combine, high margins, low leverage and consistent innovation at this level.

The challenge is growth perception.

The key question now is whether Edwards can successfully move beyond its original TAVR growth story. The company’s newer tricuspid therapies could become critical here.

Tricuspid valve disease has historically been underserved, partly because many patients are poor candidates for surgery. Edwards’ EVOQUE system represents one of the first meaningful minimally invasive treatment options in this market.

This opportunity could be large. Millions of patients globally remain untreated, while awareness and diagnosis continue improving. If adoption accelerates over time, tricuspid therapies could evolve into a major long-duration growth engine.

That possibility helps explain why analysts still project strong profit growth next year despite recent investor skepticism.

Competition remains strong, particularly from Medtronic and other structural heart players. Slower-than-expected TAVR adoption could continue pressuring sentiment. Newer therapies like EVOQUE still face commercialization and adoption risk. Healthcare reimbursement dynamics always remain important in medical technology.

Still, Edwards’ balance sheet, moat, and innovation capabilities provide substantial resilience.

Overall, the current setup increasingly resembles a high-quality compounder temporarily priced below historical enthusiasm levels.

Many healthcare businesses face controversy around pricing, reimbursement battles, or questionable societal value. Edwards stands apart. There have not been major, sustained public accusations that Edwards Lifesciences engaged in the kind of systemic price gouging controversies seen in parts of pharma.

Its products directly improve patient outcomes in ways that are both visible and measurable. Minimally invasive valve replacement can extend lives, reduce hospitalization time, and improve quality of life for elderly patients who previously had limited treatment options.

Healthcare innovation is not automatically positive impact. But helping patients avoid high-risk open-heart surgery is a compelling real-world benefit.

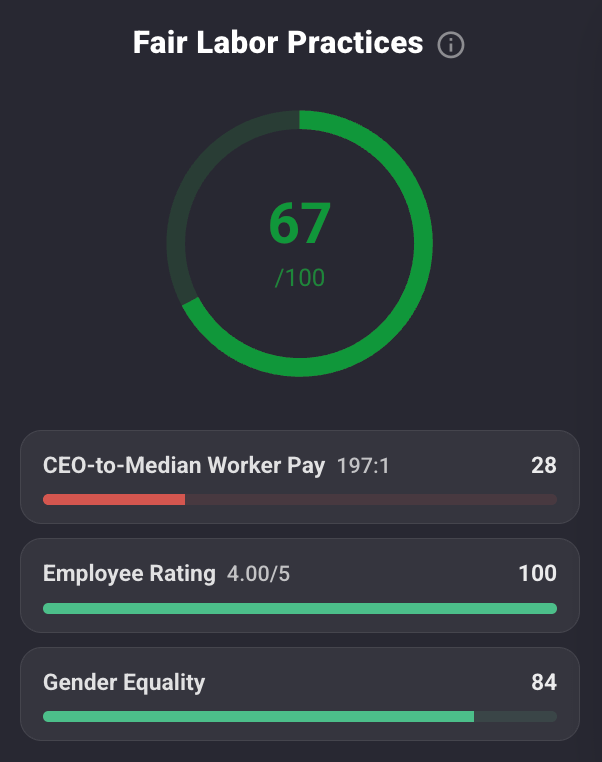

Edwards also compares favorably to many healthcare peers from an operational standpoint. The company holds an Impact Score of 74, supported by strong climate, resource use, and labor metrics:

Employee ratings are particularly strong at 4.0 out of 5.

The company is not perfect. Accountability metrics are weaker, and climate metrics show room for improvement, especially regarding global warming trajectory targets. Still, relative to many pharmaceutical and healthcare businesses, Edwards appears meaningfully more responsible and less controversial.

That strengthens its fit within the GoodStocks framework.

Source: Ziggma

Edwards Lifesciences may no longer be the market’s favorite hypergrowth medical device stock. But that could be exactly what makes the current setup interesting.

The company still operates one of the strongest franchises in healthcare. It benefits from aging population trends, medically necessary procedures, and a deep competitive moat built over decades. Meanwhile, newer structural heart therapies could reignite longer-term growth beyond the original TAVR story.

Importantly, Edwards also represents a form of healthcare innovation that is easier to believe in. Its products help patients live longer and avoid invasive surgery. Its business model remains financially disciplined and relatively low controversy. And after a major valuation reset, investors may finally be getting the chance to buy a world-class healthcare compounder at a far more reasonable price.

For long-term investors looking for both durable returns and meaningful societal impact, Edwards Lifesciences increasingly looks like a compelling GoodStock candidate.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.