Disclosure: PODD is a holding in the Ziggma High Conviction model portfolio.

Source: Ziggma

Here is a question worth sitting with: what do you do when a company grows revenue by 34%, beats earnings estimates by 18%, raises its guidance — and then watches its stock fall anyway?

For impact investors willing to look past short-term noise, Insulet Corporation (PODD) may be one of the most compelling setups in healthcare right now. The stock has shed roughly 60% from its 52-week high of $354.88, with shares recently trading around $151. Yet the underlying business is accelerating, the product pipeline is the strongest it has ever been, and insiders are buying. A company director put nearly $500,000 of her own money into shares at these levels in early June 2026. That is not the behavior of someone who thinks the story is broken.

Insulet makes the Omnipod, a tubeless, wearable automated insulin delivery system used by people with diabetes. It is a product that directly improves clinical outcomes and quality of life for patients — and it now has FDA clearance to reach a vastly larger population than ever before. The combination of a genuinely impactful product and a deeply discounted stock makes PODD a higher-risk, higher-upside candidate for the Good Stocks universe.

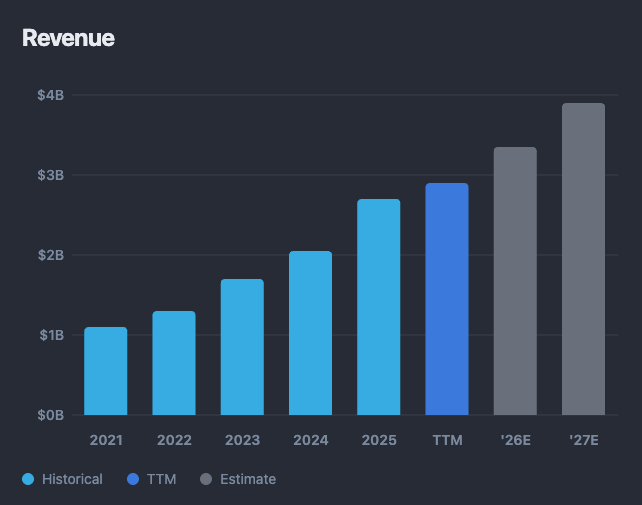

Insulet posted Q1 2026 revenue of $761.7 million, up 33.9% year-over-year, and raised its full-year 2026 constant-currency revenue growth guidance to 21-23%, with profit growth projected above 86%. At a forward price-to-earnings ratio of just 23.4x on that profit trajectory, the Ziggma Stock Score of 95/100 (Growth 89, Profitability 88) reflects a business that the market has materially mispriced.

The Omnipod 5’s SECURE-T2D pivotal trial — the largest and most racially diverse study of automated insulin delivery in Type 2 diabetes ever conducted — showed patients gaining an average of 4.8 extra hours per day in a healthy blood sugar range. For the roughly 420 million people worldwide living with diabetes, that kind of outcome is not incremental. It is life-changing.

Insulet Corporation was founded in 2000 and is headquartered in Acton, Massachusetts. It develops, manufactures, and commercializes insulin delivery systems under the Omnipod brand, selling direct to patients through the pharmacy channel and via distributors internationally. With 2025 revenue of $2.71 billion and a market cap of approximately $10.5 billion, it is one of the largest dedicated diabetes technology companies in the world.

The flagship product is Omnipod 5, an automated insulin delivery system that replaces traditional injection regimens with a waterproof, tubeless pod worn on the body. The pod communicates wirelessly with a continuous glucose monitor and automatically adjusts insulin delivery in real time. No tubing. No manual calibrations. No injections. For a person managing Type 1 diabetes, this can mean the difference between constant vigilance and something closer to a normal life.

A Market That Is Still Wide Open

The global opportunity is enormous and still largely untapped. Roughly 420 million people worldwide live with diabetes, the vast majority still relying on syringes or basic insulin pens. Insulet’s pharmacy channel access gives it a structural moat that competitors are finding hard to replicate. International Omnipod revenue grew 59.4% in Q1 2026 alone, and reimbursement coverage now extends to 85% of the Canadian market and above 90% in the US.

Source: Ziggma

Leadership is also a meaningful upgrade from the recent past. New CEO Ashley McEvoy, appointed in April 2025, brings 27 years at Johnson and Johnson, including six years running its Vision and Diabetes Care division. She arrived with direct category knowledge and a personal connection to the mission — her late grandfather was insulin-dependent. Her first full year of results have been strong, and J.P. Morgan noted at her appointment that she would bring “a more sophisticated level of communication” to a company that had struggled to tell its own story to investors.

Five Years of Evidence

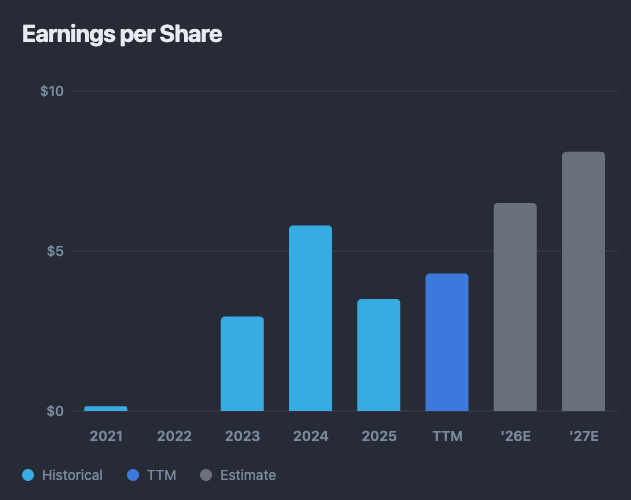

The Ziggma financial data reflects consistent execution interrupted by transition-year noise. Revenue has compounded at 19.8% annually over five years. EBITDA margins expanded from 8.1% in 2022 to 21.6% in 2025. Return on equity reached 43% in 2024 before pulling back to 18.1% in 2025, reflecting one-time restructuring charges that are already working through the system. Operating cash flow grew at 59.6% over the same five-year window — a figure that says a great deal about the quality of the underlying business.

The 2025 earnings-per-share decline of 39.8% looks alarming until you understand what caused it: a CEO transition, restructuring costs, and expenses tied to a pod configuration change. None of these are structural. Forward projections show earnings snapping back sharply, with 86% profit growth expected in 2026 and earnings per share projected to continue climbing toward $9 in 2027.

Source: Ziggma

Valuation: Cheap Relative to Growth

On a price-to-sales basis, PODD has re-rated from 16.9x in 2021 to just 5.1x today. The market is essentially pricing in very little of the growth that management has guided for and delivered. A forward price-to-earnings of 23.4x on 86% profit growth is the kind of setup growth investors look for. The 24-analyst consensus price target of $248 implies roughly 64% upside. RBC has maintained its Outperform rating with a $280 target. William Blair recently initiated with Outperform, specifically noting that the shares are pricing in too much pessimism.

Source: Ziggma

What Could Go Wrong

The voluntary recall of roughly 7 million pods due to a manufacturing defect is an overhang that needs a clean resolution. Gross margins face near-term pressure from the pod configuration transition, and two distributors together account for roughly 46% of revenue. Competition from Tandem, Beta Bionics, and DexCom-integrated systems is real. This is a recovery play, not a compounder — and investors should size accordingly.

The Setup

With a 95 Ziggma Stock Score, 64% average analyst upside, 86% projected profit growth, and insider buying near multi-year lows, PODD offers one of the more asymmetric return profiles in healthcare today.

The Clinical Case Is Hard to Argue With

Better glucose control is not just about comfort. It is about preventing the cascade of complications that make diabetes one of the most devastating chronic conditions on earth: kidney failure, vision loss, cardiovascular disease, and limb amputation. The Omnipod platform prevents those outcomes with clinical evidence to back it up.

The SECURE-T2D trial, the largest and most racially diverse automated insulin delivery study in Type 2 diabetes ever conducted, produced remarkable results. After 13 weeks on Omnipod 5, participants saw their primary blood sugar control metric (HbA1c) fall from 8.2% to 7.4%, gained an average of 4.8 more hours per day in a healthy glucose range, and reduced their daily insulin dose by 23 units — all without increasing time in dangerously low blood sugar territory. The FDA cleared Omnipod 5 for Type 2 diabetes in August 2024, and more than 30% of new patient starts by Q1 2025 were already Type 2 patients.

Reaching Those Who Need It Most

Around 24% of SECURE-T2D trial participants were Black and 22% were Hispanic — the exact communities that bear a disproportionate burden of Type 2 diabetes complications and mortality. Bringing automated insulin delivery to those populations through an accessible pharmacy channel is not a footnote to the business strategy. It is the business strategy.

The pipeline extends the impact thesis further still. Omnipod 6, expected to launch in 2027, delivers up to 50% more automated insulin and produced strong results across all age groups in the STRIVE pivotal trial, presented at the American Diabetes Association conference in June 2026. The fully closed-loop system for Type 2, currently in the EVOLVE pivotal trial targeting a 2028 commercial launch, would eliminate bolus inputs entirely. No mealtime calculations, no settings to configure. That is a genuine step-change for the hundreds of millions of Type 2 patients who have never had access to this technology.

Where Insulet Has Work to Do

The ACA Ethos Impact Score of 67/100 (POSITIVE) reflects genuine product-level leadership. Climate Action (70) and Fair Labor (64) are solid. But Resource Use (57) exposes a real gap: only 11% of energy comes from renewables for a company operating at this scale. The Accountability score of 30 is the most concerning number in the Impact scorecard, reflecting an employee satisfaction rating of 1.90/5. Employee reviews point to real cultural challenges that built up through a period of rapid growth and serial leadership turnover. The appointment of Ashley McEvoy is a credible reset, but investors should watch whether the culture improvements follow the financial ones.

Insulet is a company with a world-class product, proven clinical impact, and a growth engine that the market has temporarily chosen to ignore. The stock is down 60% from its highs while the business posts 34% revenue growth and raises guidance. That gap does not close overnight, and the near-term risks are real. But for impact-oriented retail investors with a two-to-three year horizon and an appetite for some volatility, PODD offers something genuinely rare: a Ziggma Stock Score of 95, 64% analyst upside, and a product that is literally adding hours of healthy life to patients every single day.

Higher-risk, higher-upside. The risk here is not that the business is broken. It is that the market takes time to recognize it never was.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.