Rivian (RIVN 🔎) just hit its first full year of positive gross profit. Its most important product ever is rolling off the line. And a $5.8 billion bet from Volkswagen says the technology is real. For investors who want their portfolio to reflect their values, RIVN sits at a rare crossroads: a high-upside inflection story wrapped in genuine environmental impact.

This is not a “safe” stock. Rivian is still burning cash and operating profitability is at least a year away. But the risk/reward is shifting, and the window to get in before the R2 ramp plays out is narrow. Here is why this stock belongs on your radar.

Source: Ziggma

Key Takeaways

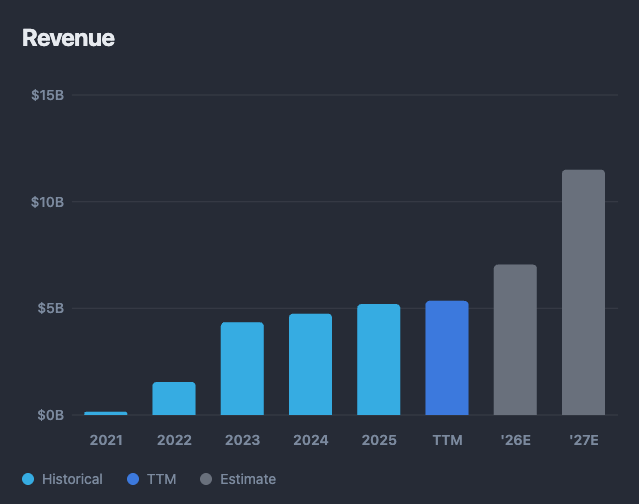

Rivian spent years being written off as a money-losing EV startup with a premium-only product and no clear path to scale. The story changed in 2025. Full-year gross profit came in at $144 million, the first time the company made money on the vehicles it sells. That is the milestone that separates companies that survive from those that do not.

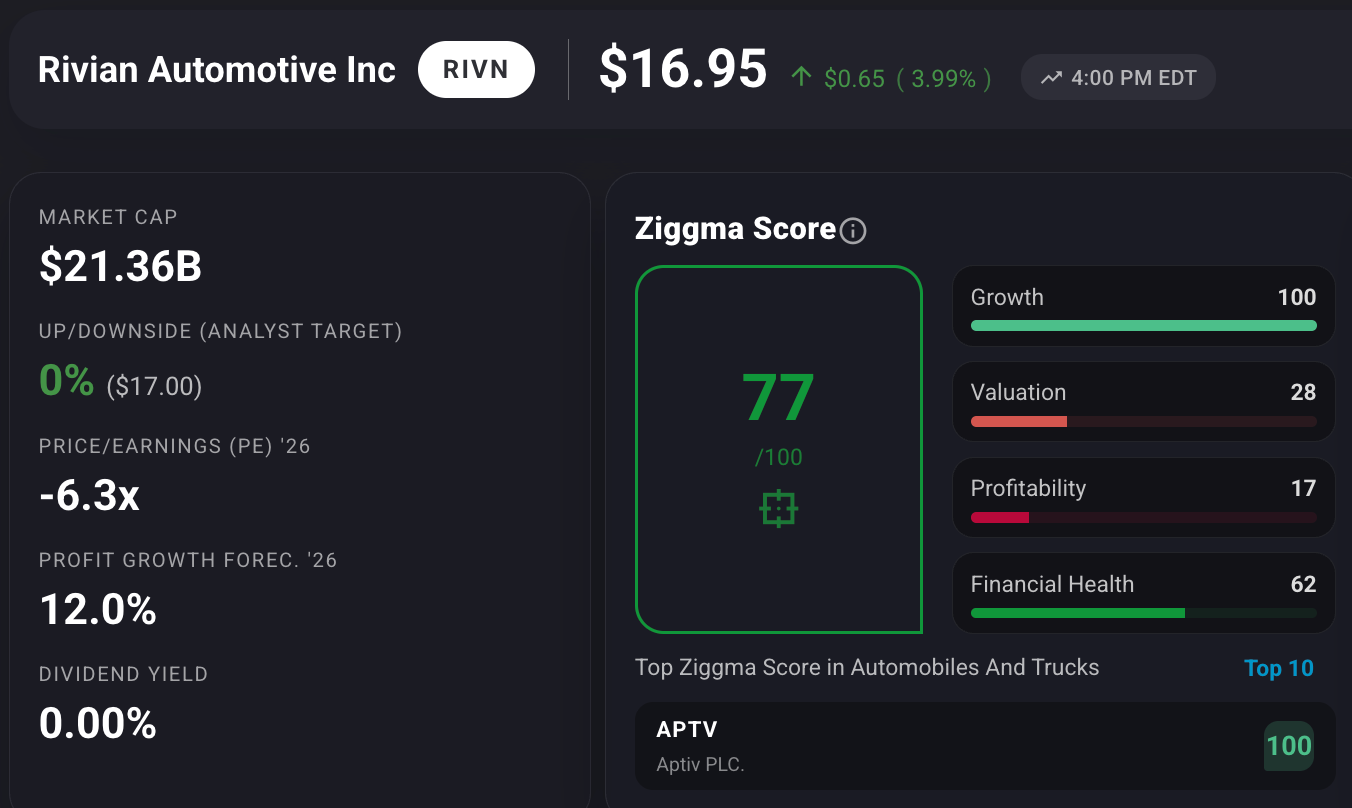

The Ziggma Score of 77/100 captures what the market is beginning to reprice, most notably a perfect Growth sub-score of 100/100 and a Financial Health sub-score of 62/100. Revenue has grown at a 5-year CAGR of 150%, and the Q1 2026 earnings print beat expectations on both revenue ($1.38 billion, up 11% year over year) and loss per share ($0.55 actual versus $0.60 expected). Deliveries were up 20% year over year.

Source: Ziggma

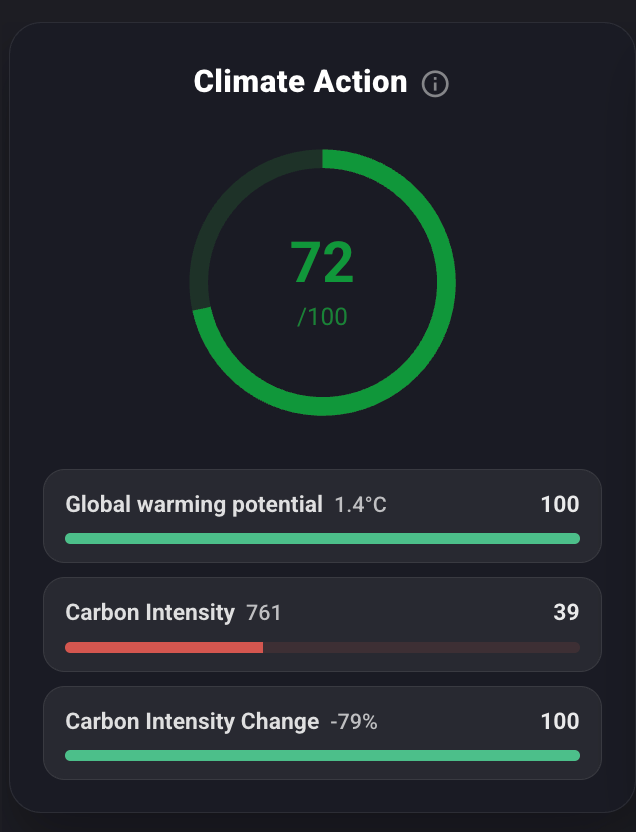

Rivian’s R1T pickup has a full lifecycle carbon footprint 34% lower than the tailpipe and fuel emissions alone of an average gas-powered pickup, according to the company’s own lifecycle assessment. Every vehicle that leaves the Normal, Illinois plant gets its first charge from 100% renewable energy produced onsite. The Impact Score of 66/100 is led by Climate Action (72/100) and Sustainable Resource Use (70/100), the two dimensions that matter most for an automaker with genuine environmental ambitions.

Rivian makes electric trucks and SUVs, but calling it a truck company misses the bigger picture. The R1T pickup and R1S SUV are the brand-builders: premium, adventure-ready vehicles that command fierce loyalty among owners. The commercial delivery van, produced for Amazon, extends the mission into fleet electrification. And the R2 SUV, now entering production at roughly $45,000 to $58,000, is the mass-market vehicle that makes everything else scale.

What makes Rivian structurally interesting is its software layer. The company has built its own vehicle electrical architecture from the ground up, and that is exactly what Volkswagen paid to access. The joint venture means Rivian is no longer just selling trucks; it is licensing technology to one of the largest automakers on earth. That fundamentally changes the ceiling.

The US EV market is expected to grow steadily through 2030, and Rivian is positioning itself as the clear number two in North America behind Tesla in the adventure and mid-size SUV segments. The moat is real: brand identity, software differentiation, and a manufacturing footprint that would take billions and years to replicate.

Rivian is not a value stock. The Valuation sub-score of 28/100 and Profitability sub-score of 17/100 make that plain. Price/Sales is 3.4x trailing and the company is guiding for an adjusted EBITDA loss of $1.8 to $2.1 billion for full-year 2026. These are not the metrics of a mature compounder.

But the trajectory is what counts here. Net loss per share improved from -$0.60 consensus to -$0.55 actual in Q1. Gross margin held at approximately 9%. Software and Services revenue, largely fueled by the Volkswagen joint venture, grew 49% year over year to $473 million, becoming an increasingly significant part of the total revenue mix. For context, Rivian’s Q4 2025 software segment alone contributed $447 million, roughly a third of quarterly revenue, at margins far above the vehicle business.

The entire investment case pivots on one question: can Rivian execute the R2 launch at cost? Management confirmed on the Q1 call that the R2’s bill of materials is approximately half that of the R1 platform, and non-manufacturing costs are expected to fall more than 50% due to new design and production efficiencies. The target is to profitably deliver 4,000 vehicles per week from Normal, Illinois. With a second plant in Georgia adding capacity through 2028, total manufacturing capacity across both sites is projected at 515,000 units annually.

Full-year 2026 delivery guidance sits at 62,000 to 67,000 vehicles, with heavier volume expected in the second half as the R2 ramp builds. That implies roughly a 59% annual increase at the top end compared to 2025.

Analyst targets range from $14 to $25, reflecting genuine disagreement about execution risk. CFRA recently raised its target to $22. Wedbush maintains an Outperform with a $25 target. Cantor sits at $19. With the stock trading at roughly $17, the consensus implies limited downside from current levels but meaningful upside if the R2 lands.

The wide range is itself the story: this is a stock where execution either unlocks a re-rating or confirms the skeptics. Operating breakeven is realistically 2027 or 2028. Cash on hand sits at $4.83 billion, providing runway, but free cash flow was -$1.08 billion in Q1 alone.

The four risks that matter most: R2 production delays or cost overruns would set the profitability timeline back significantly; tariffs on South Korean battery supply from LG Energy Solution add cost pressure until domestic sourcing ramps by 2027; the macro environment for big-ticket discretionary purchases remains uncertain; and Volkswagen’s continued investment, while substantial, involves dilution from new share issuances. This is a high-conviction, high-patience investment, not a trade.

At current prices and with analyst consensus around $17 to $22, the immediate upside is modest on paper. But if R2 volumes build through 2026 and the software licensing revenue continues compounding with the VW joint venture, the path to a $22 to $25 stock is credible within 12 to 18 months. The bigger opportunity is what a profitable, scaled Rivian looks like in 2028, when both plants are running and the autonomy roadmap is visible.

Rivian’s lifecycle assessment of the R1T makes a stark point: the truck’s total carbon footprint, manufacturing included, is 34% lower than just the tailpipe and fuel emissions of a comparable gas pickup. That comparison is not cherry-picked. It accounts for the full production process, battery manufacturing, and energy used over the vehicle’s life. The Climate Action score of 72/100 reflects both that advantage and a 79% improvement in carbon intensity over the measurement period.

The Global Warming Potential implied temperature rise score of 1.4 degrees Celsius places Rivian among the most climate-aligned companies in any sector.

Source: Ziggma

The impact goes deeper than the cars themselves. Every kilowatt-hour on the Rivian Adventure Network is matched with 100% renewable energy. The company co-developed a framework with The Nature Conservancy to prioritize renewable energy projects that deliver the greatest combined benefit for climate, conservation, and local communities. On the commercial side, the Amazon delivery vans represent fleet-scale electrification with a direct carbon reduction effect across last-mile logistics, one of the more emissions-intensive links in the supply chain.

Rivian has signed the Climate Pledge and set a net-zero target for 2040, with specific commitments to halve the carbon footprint of its vehicles by 2030 through increased recycled materials, improved manufacturing efficiency, and supply chain decarbonization.

The Sustainable Resource Use score of 70/100 reflects meaningful progress on water stewardship and material efficiency. Where Rivian lags, notably Accountability (13/100) and Fair Labor (44/100), signals room for improvement on corporate governance and pay equity, areas the company will need to address as it scales.

Rivian is not the right stock for everyone. It is unprofitable, capital-hungry, and the R2 launch needs to execute nearly perfectly for the bull case to materialize. But for an investor with a two-to-three year horizon who wants a stake in clean transportation and believes EV adoption in North America is a structural trend, not a fad, RIVN offers something rare: a credible technology platform, a mission-driven brand, and a valuation that still reflects the doubts rather than the potential.

The first year of gross profitability is done. The mass-market vehicle is shipping. Volkswagen wrote the check. The inflection is underway. Whether you call it impact investing or just good stock picking, Rivian is worth a serious look.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.