The bear case on Salesforce is simple: AI will make CRM software obsolete. The bull case is simpler. Salesforce already has the AI platform, the customer base, and the cash flow to prove that wrong — and the stock is priced like the bears are right.

CRM has shed 28% in 2026 while quietly posting its fastest revenue growth in two years, beating earnings estimates by 31%, and scaling Agentforce to nearly $1.4 billion in annual recurring revenue. The market is looking at yesterday’s story. The numbers are writing a different one.

And here is what makes this a GoodStock, not just a trade: Salesforce runs on 100% renewable energy, has achieved net zero emissions across its full value chain, and pioneered a philanthropy model that has since spread to 19,000 companies worldwide. It scores 87/100 on the Ziggma Impact Scale. That combination — genuine impact credentials and a genuinely beaten-down price — is exactly what this series exists to find.

Source: Ziggma

KEY TAKEAWAYS

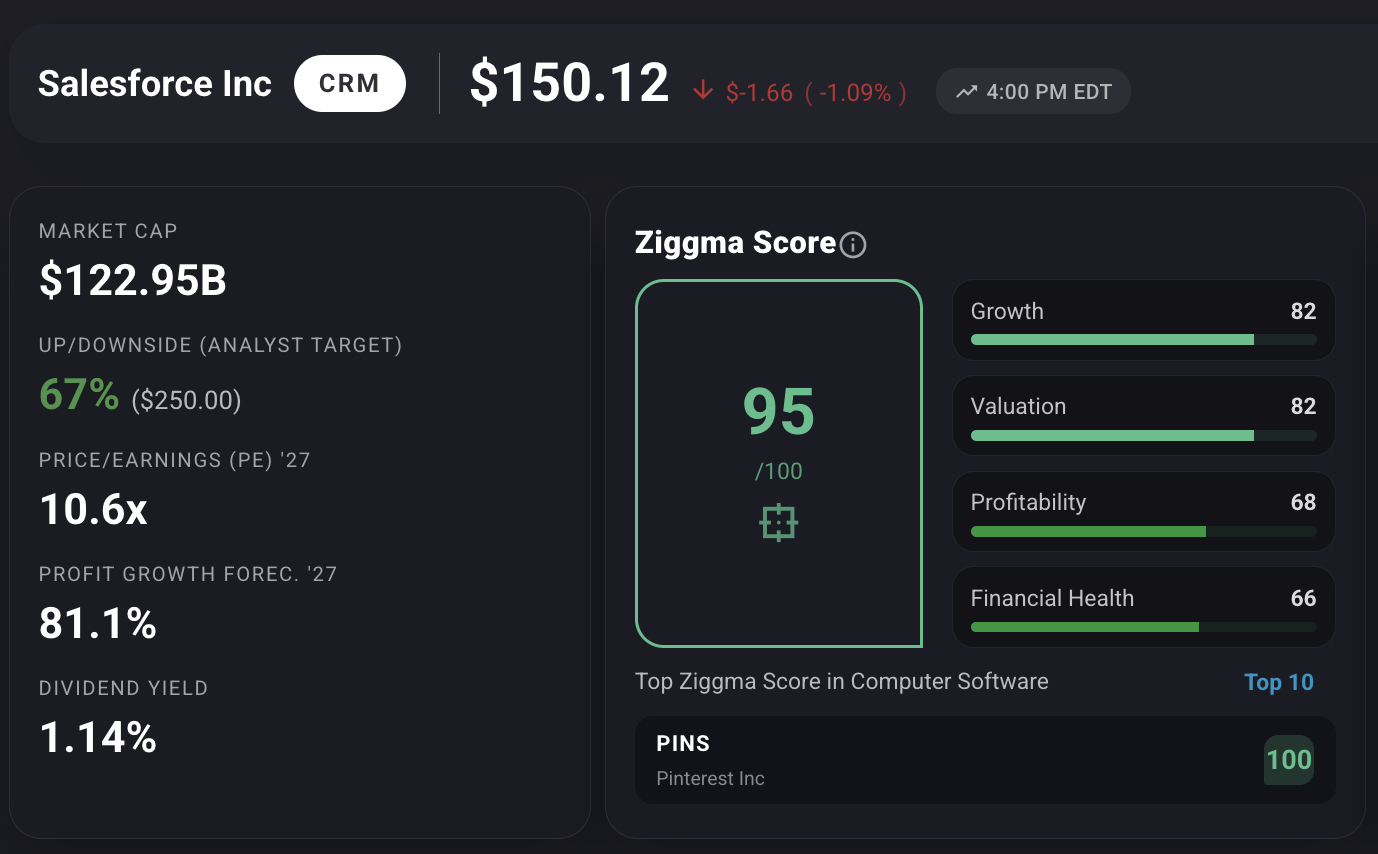

Salesforce trades at roughly 10.6x forward earnings for fiscal year 2027, at a moment when analysts forecast profit growth of 81% by that same year. That combination of low valuation and accelerating earnings is rare in large-cap software. The consensus among Wall Street analysts is a Buy, with an average 12-month price target in the $250 range, implying over 60% upside from current prices. Salesforce itself has committed $50 billion to share buybacks at what CEO Marc Benioff described on the Q4 earnings call as “some low prices” - a signal of management conviction that is hard to ignore.

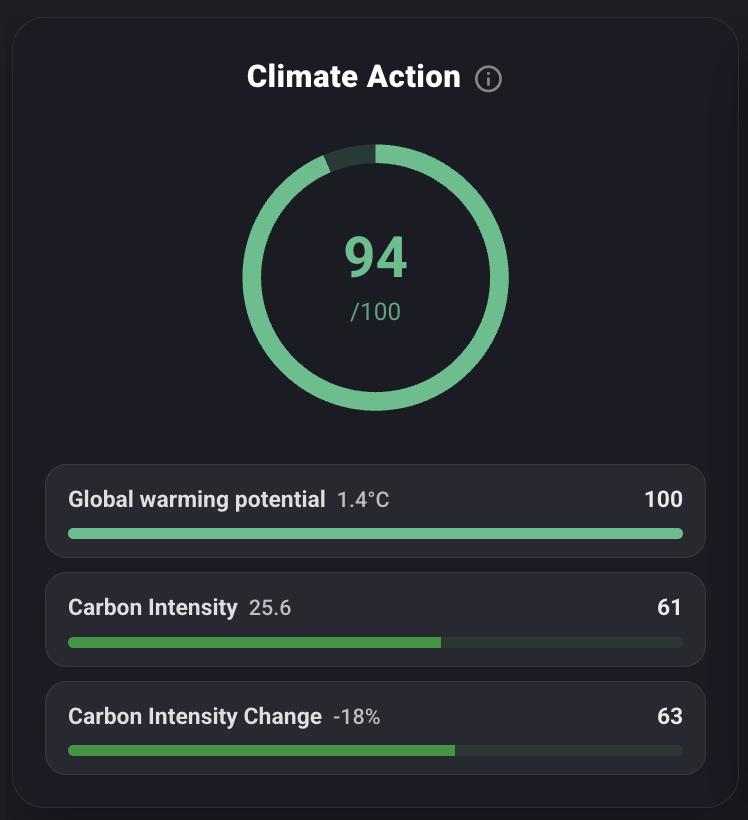

Salesforce has been running on 100% renewable energy since 2021 and achieved net zero residual emissions across its entire value chain, including suppliers and customers, well ahead of most peers. Its Climate Action sub-score on the Ziggma platform registers a near-perfect 94/100, with a global warming potential of just 1.4°C and energy sourced 100% from renewables. The company’s 1-1-1 model, pledging 1% of equity, 1% of employee time, and 1% of product to nonprofits, has mobilized a movement now spanning 19,000 companies in over 100 countries.

Salesforce is the global leader in customer relationship management software, holding a 20.7% share of the worldwide market according to IDC, a position it has held for 12 consecutive years. Its platform spans Sales Cloud, Service Cloud, Marketing Cloud, Commerce Cloud, and the newer Data 360 and Agentforce suite. With over 150,000 customers ranging from small businesses to nearly half the Fortune 100, Salesforce is deeply embedded in how the world’s companies manage their relationships with customers.

What makes Salesforce’s market position so defensible is not any single product but the depth of integration. Once a large enterprise has built its sales workflows, customer service operations, and marketing automation on Salesforce’s platform, migration to a competitor becomes an enormous undertaking. Add in the Data 360 layer, which unifies customer data across all touchpoints, and the switching cost grows further. This structural stickiness translates into highly predictable, recurring revenue and long-term retention rates that are difficult for newer entrants to replicate.

The most significant development in Salesforce’s recent history is Agentforce, its platform for deploying AI agents across business workflows. Launched in late 2024, it has already closed over 18,500 deals, including 9,500 paid contracts, and processed 19 trillion tokens of AI work as of Q4 FY26. The platform’s own internal deployment at Salesforce’s customer support operation resolved 84% of cases without human intervention, with only 2% escalating to a human agent. These are not pilot numbers. They represent a fundamental shift in how enterprise software creates value.

After a period of slower growth that weighed on the stock, Salesforce posted 12% revenue growth in Q4 FY26, its fastest rate in two years, followed by 13% growth in Q1 FY27. Full-year FY26 revenue came in at $41.5 billion. Management has guided FY27 revenue to $45.8 to $46.2 billion, implying 10 to 11% growth, with organic acceleration expected in the second half of the year as Agentforce adoption scales.

The operating margin picture has improved materially. Non-GAAP operating margin came in at 34.8% in Q1 FY27, and management is targeting a path toward 50% operating margin by fiscal year 2030 under its Profitable Growth Framework. The five-year operating cash flow compounded annual growth rate is over 20%, and the company generated $15 billion in operating cash flow in FY26. The balance sheet is conservative, with a net debt-to-EBITDA ratio that has historically been negative, meaning Salesforce carries more cash than debt.

At roughly 10.6x forward earnings for fiscal year 2027, Salesforce trades at a level that would have seemed unthinkable just two years ago for a business of this quality. That forward multiple sits at a steep discount to historical norms, reflecting a market that has repriced the stock as though the growth story is over.

The Price-to-Sales ratio drives the point home even more starkly: at around 3.8x today, it sits roughly 50% below its 10-year median of 7.6x, and a fraction of the 8-10x the stock commanded at peak in 2021 and 2022. The froth has been thoroughly wrung out.

The Ziggma Valuation sub-score of 82/100 and Growth sub-score of 82/100 confirm what the raw numbers suggest: this is a high-quality business trading at an uncharacteristically attractive price. The Ziggma Financial Health sub-score of 66 reflects the Debt-to-Equity ratio which has ticked up to 1.1x following the Informatica acquisition, worth monitoring, though cash generation remains robust.

The bear case centers on AI disruption: if tools like large language models allow companies to build custom software more easily, demand for packaged CRM could face pricing pressure over time. Microsoft continues to embed AI deeply into its existing enterprise suite, creating a competitive threat from a vendor many customers already rely on. And while Agentforce’s early traction is impressive, converting pilot deployments into full enterprise contracts at scale remains the critical execution challenge for the next 12 to 18 months. Informatica integration execution is an additional variable to watch.

With analysts clustering around price targets in the $250 range against a current price near $150, and with earnings growth projected at over 80% through fiscal 2027, the risk-to-reward profile at current prices is compelling. The Ziggma Score of 95/100 places CRM in the top tier of the computer software universe and reflects a high quality stock.

Salesforce’s environmental credentials are among the strongest of any large-cap technology company. It has operated on 100% renewable energy since 2021 and was one of the first major corporations globally to achieve net zero residual emissions across its full value chain, including Scope 1, 2, and 3 emissions. Its carbon intensity has declined 18% in recent years. The company’s Ziggma Climate Action sub-score of 94/100 reflects genuine, third-party verified commitments, not marketing copy.

Net Zero Cloud: Helping Others Get There Too

What distinguishes Salesforce from most corporate sustainability stories is that its impact extends beyond its own operations. Net Zero Cloud, now part of the broader platform, helps enterprises track, analyze, and reduce their own carbon footprints. In a world where companies face increasing regulatory and investor pressure to measure and disclose emissions, Salesforce has turned its own sustainability journey into a product. The customers who use it to achieve their own net zero goals create a multiplier effect that goes well beyond anything Salesforce’s internal operations could achieve alone.

The Ziggma Sustainable Resource Use sub-score of 87/100 reflects 91 points on sustainable water use and 85 points on energy from renewables. Gender Equality scores 95/100. Employee satisfaction registers 4.10 out of 5, earning a near-perfect 98/100 on the Ziggma Fair Labor sub-score. The one area where Salesforce scores lower is Accountability, at 44/100, driven partly by a CEO-to-median-worker pay ratio of 308:1. It is a real number and an honest tension the company will need to address over time. But in the aggregate, the Impact Score of 87/100, rated “Profound,” reflects a company that takes its responsibilities to people and planet seriously, in measurable ways.

Salesforce is down sharply in 2026. The market has priced in fear of AI disruption, growth deceleration, and competitive pressure. But the most recent results tell a different story: revenue growth accelerating, earnings crushing expectations, a contracted backlog approaching $72.5 billion, and an AI platform growing at triple-digit rates. Trading at a decade-low valuation while generating record cash flow, backed by a Ziggma Score of 95/100 and an Impact Score of 87/100, CRM looks like exactly the kind of GoodStock the market overlooks. For investors with a two to three year horizon and the conviction to go where the crowd is not, Salesforce at current levels is a case worth making.

____________________________________________________________________________________________________________________________________________________

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.