The world is moving toward digital payments faster than ever. Artificial intelligence is accelerating commerce, cross-border transactions keep climbing, and cash continues to disappear from the global economy. Yet despite sitting at the center of these trends, Visa Inc. (V 🔎) currently trades below its historical valuation multiples.

That disconnect is exactly what makes Visa so interesting right now.

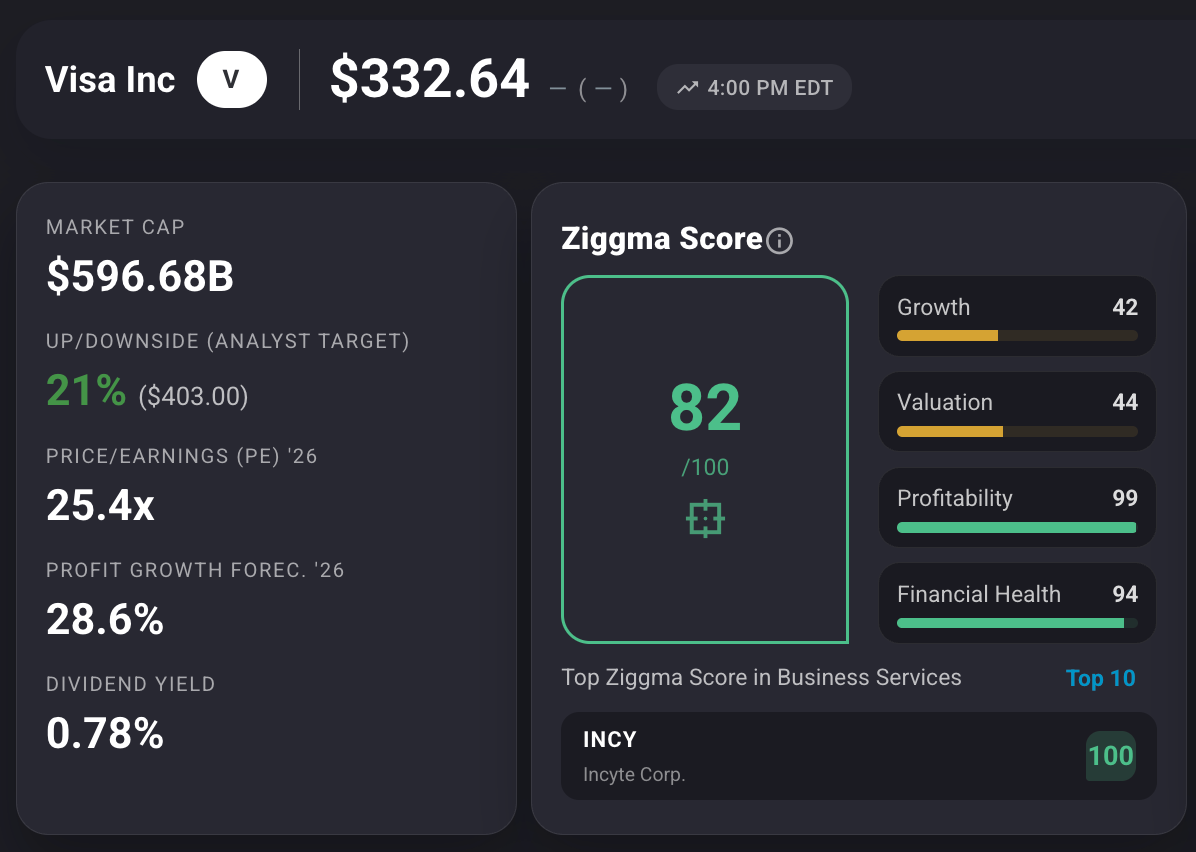

Investors often assume the world’s largest payment network has already matured. But the numbers suggest otherwise. Revenue is still projected to grow at double-digit rates, earnings are expected to climb nearly 29% next year, and analysts see roughly 21% upside from current levels. Meanwhile, Visa continues to generate extraordinary profitability, massive free cash flow, and relentless share buybacks that steadily increase each shareholder’s ownership stake. And unlike many financial companies, Visa also stands out on climate metrics and operational responsibility. The company operates with a relatively light environmental footprint, sources renewable electricity, and benefits from the broader shift away from paper cash and physical banking infrastructure.

That combination of durable growth, financial strength, and positive impact makes Visa a member of the GoodStocks universe.

Source: Ziggma

Visa combines one of the strongest business models in the world with unusually attractive valuation conditions. Revenue growth remains in line with historical averages, yet the stock trades materially below its long-term Price/Sales multiple.

Visa scores strongly on climate action and resource efficiency, supported by its low operational footprint and renewable electricity usage. The company also helps accelerate the global shift toward digital payments, reducing reliance on cash-heavy systems and physical banking infrastructure.

Visa is not a bank. It does not lend money directly to consumers. Instead, it operates the infrastructure layer behind global digital commerce. Every time a consumer taps a card, shops online, or sends money internationally, Visa helps route and secure the transaction. The company processes more than 300 billion transactions annually across over 200 countries and territories. That creates one of the strongest network effects in global finance.

Consumers use Visa because merchants accept it everywhere. Merchants accept Visa because consumers carry it everywhere. Replicating that network would take decades and enormous trust. The long-term market opportunity also remains massive. According to industry estimates, trillions of dollars in global consumer payments still occur through cash and checks. At the same time, e-commerce, digital wallets, and cross-border payments continue expanding rapidly. Now a new driver is emerging: artificial intelligence. As AI agents begin handling purchases, subscriptions, logistics, and automated business transactions, payment infrastructure becomes even more important. Visa is already positioning itself for this future through tokenization, fraud prevention systems, and AI-enhanced payment security.

The AI economy will still need trusted financial rails. Visa already owns some of the most important ones.

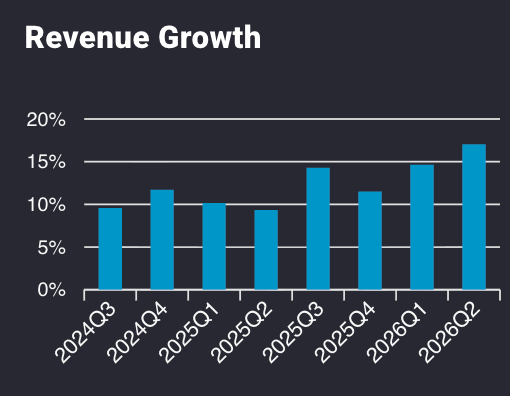

For a company worth nearly $600B, Visa’s growth profile remains exceptional. Revenue has compounded at roughly 10.7% annually over the past five years. Importantly, forward estimates still point toward revenue growth around 11-14%, showing that the company’s momentum has not slowed.

Source: Ziggma

Earnings growth has been even stronger historically. Analysts currently forecast profit growth of roughly 28.6% next year. Few mega-cap companies combine this level of consistency with this degree of profitability. Visa’s net profit margins exceed 50%. Return on equity recently climbed above 60%. Even more impressive, return on assets jumped sharply over the past two quarters, rising toward 24% and 32% in forward projections, from a long-term average of 21.6%. That matters because it signals Visa is extracting more profit from every dollar invested into the business.

The company’s Ziggma Profitability Score of 99 reflects exactly that. Financial Health also scores extremely high at 94/100, supported by low debt levels and strong cash generation.

Normally, investors pay a premium for this kind of quality. Today, that premium looks surprisingly muted. Visa currently trades around 12.7x sales versus a five-year average above 14x. Its current Price/Earnings multiple also sits well below historical peaks despite fundamentals remaining very strong. In other words, Visa’s valuation has compressed while the business itself continues compounding. Part of this reflects investor rotation toward more speculative artificial intelligence names. Ironically, that may create opportunity in a company that could quietly become one of the biggest beneficiaries of AI-driven commerce growth.

Analysts currently see roughly 21% upside, with an average price target around $403.

One of Visa’s greatest strengths is its ability to turn enormous cash generation into long-term shareholder value. In 2025, the company authorized another massive $30B share repurchase program, one of the largest active buyback authorizations in the market today. That matters because buybacks steadily reduce the share count, allowing each remaining shareholder to own a larger piece of the business over time. Visa has already spent tens of billions of dollars repurchasing stock over the past decade, helping drive powerful earnings per share growth alongside rising revenues.

The company can afford this because its business model is extraordinarily efficient. Unlike industrial or manufacturing companies, Visa requires relatively little physical infrastructure to scale globally. That leaves management with exceptional financial flexibility to invest in artificial intelligence, strengthen fraud prevention systems, expand internationally, raise dividends, and continue aggressive buybacks simultaneously.

Very few companies have the financial strength to do all of that at once.

Visa still faces regulatory scrutiny around interchange fees and market dominance. Competition from alternative payment platforms and digital wallets could pressure some transaction volumes over time. Economic slowdowns may also temporarily reduce consumer spending and cross-border activity. Finally, geopolitical fragmentation could complicate global payment flows in certain regions. Still, Visa’s scale, trust, and network effects make its competitive position exceptionally durable.

Overall, the current combination of double-digit growth, expanding efficiency, strong buybacks, and below-average valuation leaves Visa looking attractively positioned for long-term upside.

Cash may seem harmless, but physical money carries meaningful environmental and operational costs. Printing, transporting, securing, and managing cash requires enormous physical infrastructure. Banks, armored transport systems, and ATMs all consume energy and resources.Digital payments are far more efficient.

Visa helps accelerate that transition by enabling secure electronic commerce globally. The company processes enormous transaction volumes with relatively limited physical infrastructure. That contributes to Visa’s relatively strong climate profile and positive Impact Score of 70.

Source: Ziggma

Visa scores particularly well on climate action and sustainable resource use. The company reports sourcing 100% renewable electricity for its operations and maintains a global warming trajectory aligned with 1.5°C scenarios according to the provided ACA Ethos data. Carbon intensity has also improved meaningfully over time.

Unlike many financial companies, Visa’s environmental footprint remains relatively manageable because it operates primarily as a digital network business rather than a capital-intensive industrial operator. That makes Visa an interesting example of how scalable digital infrastructure can potentially combine profitability with lower environmental impact.

Visa may not generate the same headlines as flashy artificial intelligence companies, but its position inside the global economy remains extraordinarily powerful. The company sits at the intersection of digital commerce, AI-enabled transactions, and the long-term decline of cash. Revenue growth remains strong, profitability is world class, and return on assets is improving sharply.

Yet despite those strengths, the stock trades below historical valuation levels while analysts still see more than 20% upside. Add in Visa’s enormous buyback engine, financial resilience, and strong climate metrics, and the investment case becomes increasingly compelling. For long-term investors seeking durable compounding with positive real-world impact, Visa continues to look very much like a GoodStock.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein. Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions. You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice. There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk. Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material. You alone bear responsibility for your decisions. Use this information at your own discretion and risk.