lnylam Pharmaceuticals (Nasdaq: ALNY 🔎) did something most drug companies never do: it invented an entirely new way to treat disease. RNA interference — the gene-silencing mechanism at the heart of everything Alnylam makes — was considered a scientific curiosity when the company was founded in 2002 around Nobel laureate research. Two decades later, Alnylam has six FDA-approved therapies, nearly $3 billion in annual revenue growing at 81% year-over-year, a platform that can theoretically be aimed at any gene target in the human genome, and a five-year strategy — Alnylam 2030 — with over 40 clinical programs in its sights.

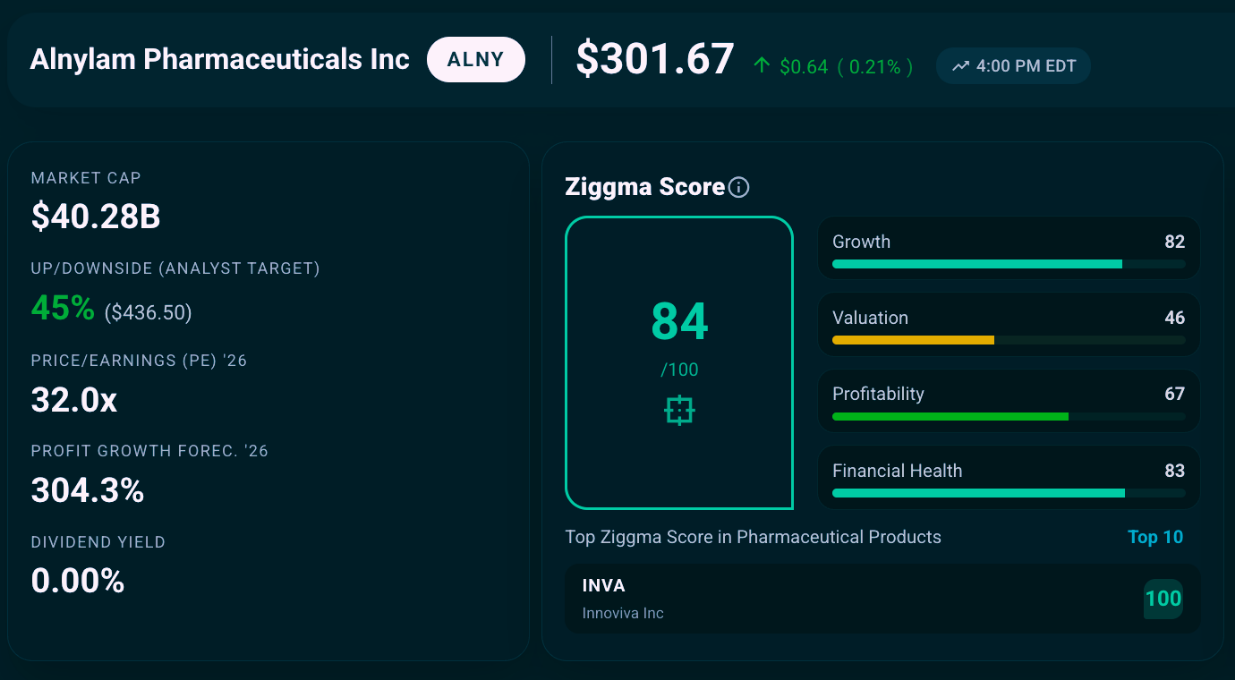

The stock trades at $301, against an analyst consensus price target of $472, implying 44% upside. The Ziggma Score is 84/100, with a Growth sub-score of 82 and a Financial Health sub-score of 83. Profit growth for 2026 is forecast at 304%. The PEG ratio is below 1.

For GoodStocks investors, the impact case here is different from what we usually feature. Alnylam’s operational environmental credentials are a work in progress. We will say so plainly. But the scientific impact of what this company does — creating medicines that simply did not exist before for patients with diseases that had no good treatment options — represents a category of positive contribution to human health that is rare, measurable, and compounding.

Source: Ziggma

➡️ For readers new to the GoodStocks series, our most recent research on Salesforce illustrates the dual thesis in action.

Alnylam was founded in Cambridge, Massachusetts, in 2002, built directly around the discovery of RNA interference — a natural cellular mechanism by which short strands of RNA can silence specific genes and prevent them from producing disease-causing proteins. The science was recognized with the 2006 Nobel Prize in Physiology or Medicine, awarded to Andrew Fire and Craig Mello, whose foundational work Alnylam licensed in its earliest days.

The core insight is elegant and radical. Most drugs work by targeting proteins after they have already been made — blocking an enzyme, occupying a receptor, neutralizing a pathogen. RNAi works upstream, silencing the messenger RNA that instructs the cell to make the protein in the first place. If the protein is never made, the disease process never starts. For conditions driven by a single gene producing a harmful protein — a category that encompasses hundreds of diseases — this is a fundamentally more precise and more powerful intervention than anything that came before.

Alnylam has translated this science into the largest portfolio of approved RNAi therapeutics in the world:

Amvuttra (vutrisiran) treats transthyretin-mediated amyloidosis (ATTR), a progressive and fatal disease in which a misfolded protein accumulates in the heart and nerves. It is approved for both the polyneuropathy form (hATTR-PN) and, following a landmark FDA approval in 2025, the cardiomyopathy form (ATTR-CM) — a far larger patient population affecting hundreds of thousands of people with heart failure of genetic or age-related origin. Amvuttra is administered by subcutaneous injection once every three months, a meaningful convenience advantage over alternatives.

Onpattro (patisiran) was the world’s first approved RNAi therapeutic, greenlit by the FDA in 2018 for hATTR-PN. Its approval validated the entire platform and demonstrated that RNAi could be safely delivered to human patients at therapeutic doses.

Givlaari (givosiran) treats acute hepatic porphyria, a rare and debilitating genetic disease causing recurrent attacks of severe abdominal pain, neurological damage, and in some cases life-threatening paralysis. Prior to Givlaari, patients had no disease-modifying option.

Oxlumo (lumasiran) treats primary hyperoxaluria type 1, a rare genetic disorder causing progressive kidney failure in children and adults. It is approved in both the US and EU for pediatric and adult patients.

Leqvio (inclisiran) is partnered with Novartis and targets PCSK9 for LDL cholesterol reduction — a massive cardiovascular market. While partnered, it validates the platform’s reach beyond rare disease into common, high-prevalence conditions.

Qfitlia (fitusiran), the sixth approved therapy, received FDA approval in early 2025 as the first and only therapeutic to treat both hemophilia A and hemophilia B with or without inhibitors — a genuinely groundbreaking label covering patient populations that previously lacked effective options.

In January 2026, Alnylam unveiled its five-year strategic plan with three pillars: achieving global TTR franchise leadership, driving long-term growth through sustainable innovation, and scaling with financial discipline. The ambitions are specific:

The pipeline includes programs in CNS disorders including Huntington’s disease in partnership with Regeneron, type 2 diabetes, obesity and weight management, hypertension through the zilebesiran program in partnership with Roche, and cardiovascular diseases through a new collaboration with Tenaya Therapeutics worth up to $1.13 billion in milestones. This is no longer a company with one drug and a platform. It is a platform company with a commercial engine large enough to fund its own transformation.

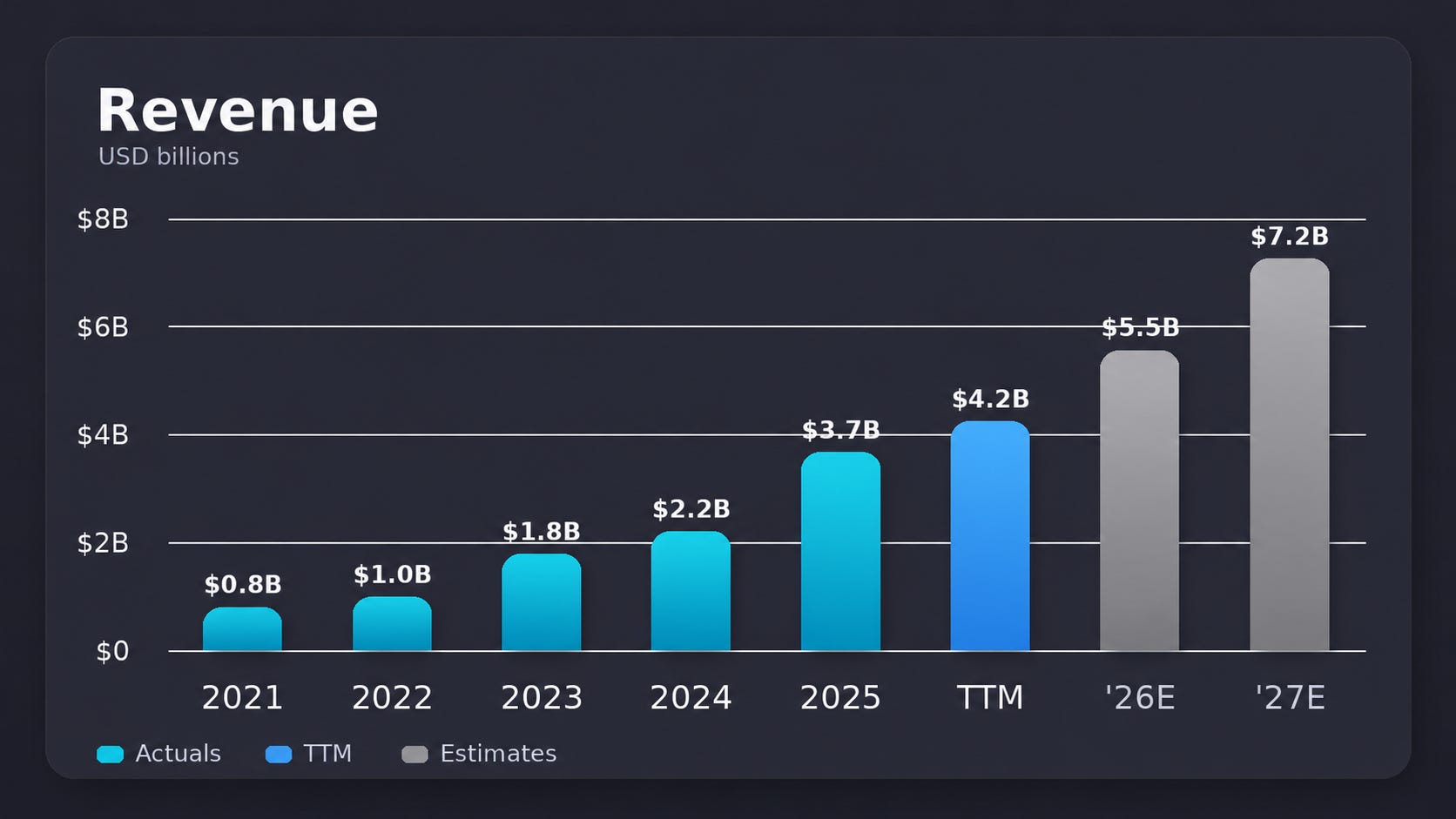

Alnylam’s revenue trajectory is one of the steepest in large-cap biotech. Total net product revenues grew 81% in 2025 to nearly $3 billion, driven primarily by Amvuttra’s ATTR-CM launch in the US following its April 2025 FDA approval. Q1 2026 revenue came in at $1.17 billion, beating consensus, with the TTR franchise growing at triple-digit rates year-over-year at peak launch velocity. Full-year 2026 net product revenue guidance of $4.4 to $4.7 billion implies growth of roughly 57% at the midpoint — sustained hyper-growth at a scale that is rare in any sector. The five-year revenue CAGR is 34.5%.

Source: Ziggma

After more than two decades of R&D investment, Alnylam hit a massive milestone by crossing into profitability in 2025. Net profit margin expanded from -12.4% in 2024 to 8.4% in 2025 and 12.5% over the past 12 months. EBITDA margin reached 15.1% in 2025 and 18.6% over the past 12 months, with significant further expansion expected as Amvuttra ATTR-CM revenues scale against a largely fixed cost base.

At 32x forward earnings for 2026, Alnylam trades at a PEG ratio below 1 — meaning investors are paying less than one times the growth rate for each unit of earnings, an unusual combination in large-cap biotech. The Price-to-Sales ratio of 10.2x is at a multi-year low, well below the 5-year average of 18.6x, reflecting the market’s historical tendency to discount Alnylam during periods of commercial uncertainty. With Amvuttra’s ATTR-CM launch now well underway and full-year guidance reiterated, that uncertainty has materially diminished. The Ziggma Valuation sub-score of 46 reflects the absolute level of the multiple rather than its relationship to growth — the PEG tells the more important story here.

The balance sheet has transformed alongside the income statement. Alnylam ended Q1 2026 with a net cash position — Net Debt/EBITDA of -2.5x — meaning cash exceeds debt by a meaningful margin. The current ratio stands at 312.7%. Financial Health sub-score on Ziggma is 83/100. With a $500 million revolving credit facility in place and operating cash generation now firmly positive, Alnylam no longer needs external capital to fund its pipeline. The Alnylam 2030 strategy is self-funded. That is a transformative shift from the company’s history as a perpetual cash consumer.

The single most important near-term risk is ATTR-CM market penetration pace. The total addressable population is large — estimated at over 300,000 patients in the US alone — but diagnosing ATTR-CM requires specialist cardiology workup that is still not routine. If patient identification rates lag expectations, near-term revenue growth could disappoint against consensus. The German pricing reset of approximately $25 million in international revenues is a one-time headwind visible in near-term estimates. Competition in the ATTR space from Pfizer’s tafamidis and emerging entrants including Novo Nordisk’s nucresiran program is real, though Amvuttra’s mechanism, quarterly dosing, and broad label create meaningful differentiation. The Q3 2025 DOJ subpoena regarding government price reporting for Amvuttra and other products is an open legal uncertainty that should be monitored, though it has not escalated to formal charges. Finally, the platform’s expansion beyond the liver into CNS and other tissues remains scientifically promising but unproven at commercial scale.

Alnylam’s therapies carry list prices that reflect the full cost of pioneering an entirely new class of medicine — from over two decades of academic research through years of clinical trials in diseases with high failure rates and small patient populations. Reasonable people disagree about whether the current US drug pricing system distributes those costs equitably. Our view is that the incentive structure that funds breakthrough science is a policy question, not an investment one — and that Alnylam’s contribution to human health is better measured by what it makes possible than by what it charges for it.

On access, the Alnylam Assist program is more robust than the industry average. Uninsured and functionally uninsured patients can receive Amvuttra at no cost through the Patient Assistance Program, with an Alnylam Case Manager proactively assessing eligibility after a doctor submits a Start Form. Commercially insured patients can access copay support reducing out-of-pocket costs to as little as $0. A Bridge Program covers patients experiencing coverage gaps or delays. The same Medicare and Medicaid exclusions apply as across the industry — a genuine limitation that reflects the gap between commercial access programs and government payer populations that remains the most significant access challenge in US specialty pharma.

ATTR amyloidosis was, until recently, a disease that cardiologists rarely diagnosed and patients often died of without understanding why. A misfolded protein produced by the liver accumulates silently in the heart muscle over decades, eventually causing progressive heart failure that is frequently mistaken for other conditions. Amvuttra silences the gene that produces the misfolded protein, preventing further accumulation and allowing the heart to stabilize. In the HELIOS-B Phase 3 trial, vutrisiran demonstrated statistically significant reductions in cardiovascular death and cardiovascular hospitalizations in ATTR-CM patients — outcomes that matter to patients and families in the most direct way possible.

Acute hepatic porphyria, the target for Givlaari, causes attacks of excruciating abdominal pain, neurological damage, and in severe cases respiratory paralysis requiring mechanical ventilation. Patients lived in fear of attacks and had no way to prevent them. Givlaari reduces attack frequency by silencing the gene driving hepatic heme synthesis dysregulation. For patients who had been hospitalized repeatedly for acute attacks, the ability to go months or years without one is life-changing in the most literal sense.

Primary hyperoxaluria type 1, targeted by Oxlumo, causes progressive kidney stone formation from birth, leading to kidney failure in childhood or early adulthood. Oxlumo was the first approved treatment that addresses the underlying genetic cause rather than managing symptoms.

What distinguishes Alnylam from a drug company that happens to have made a breakthrough is that the breakthrough is the platform, not any individual drug. Every additional RNAi therapeutic that advances to approval — whether in hemophilia, hypertension, Huntington’s disease, obesity, or diabetes — is a validation and extension of the same underlying technology. As the platform matures and manufacturing costs decline, the economic model for future drugs improves, and the case for broader access becomes easier to make. The long arc of a platform technology is always from scarce and expensive toward standard of care. That arc is what Alnylam 2030 is building toward.

The Ziggma Impact Score of 65/100, rated Positive, reflects genuine gaps in Alnylam’s impact profile that we will not paper over. Sustainable Resource Use scores 30/100, reflecting missing renewable energy data rather than confirmed poor performance, but the absence of disclosed renewable energy sourcing is a real gap for a company of this size and ambition. Fair Labor scores 39/100, driven primarily by Gender Equality at 65 — an area where Alnylam has room to improve relative to peers. The CEO-to-median-worker pay ratio of 39:1 is exceptionally restrained by large-cap biotech standards, a positive signal on compensation equity. Climate Action scores 79/100, with carbon intensity declining 30% — meaningful operational progress. Employee satisfaction at 4.90 out of 5 earns a perfect 100 and reflects a culture that genuinely attracts and retains scientific talent.

For GoodStocks investors whose primary impact lens is environmental performance, the operational picture here is not yet at the level of CRM or ECL. For those who weight medical innovation and patient outcomes as equally valid dimensions of positive real-world impact, the scientific platform speaks for itself.

Alnylam invented an entirely new class of medicine. It has six approved products built on a single platform. It grew revenue 81% in 2025 and is guiding to 57% growth in 2026, at which point it will have crossed $4 billion in annual revenue. It is newly profitable, self-funding, and building toward over 40 clinical programs across 10 tissue types by 2030. It trades at a PEG below 1, with analysts carrying a Strong Buy consensus and a median price target implying 44% upside.

The operational impact profile is a work in progress. The drug pricing reality is a genuine tension that we have addressed directly rather than minimized. The platform impact — creating medicines that literally did not exist, for patients who previously had none — is the most scientifically significant impact story in the GoodStocks series to date.

For investors who define impact broadly enough to include pioneering life-saving treatments that rewrite what is medically possible, and who have a two to three year horizon to let the Amvuttra ATTR-CM launch compound, ALNY at current levels makes a compelling case.

____________________________________________________________________________________________________________________________________________________

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.