Ziggma’s Growth, Impact, Momentum model portfolio is built directly on our GoodStocks research — the ongoing series that screens public companies on two things at once: how much value they can make for shareholders, and how much good they do in the real world. Here’s how the first half of 2026 played out, and a plain-English look at every holding.

The money you invest doesn’t just sit in an account. When invested intentionally, it funds the companies building the next version of the economy — the power grids, the clean-energy financing, the medicines, the more efficient ways of making and selling things. In a year when the climate signals keep getting louder and scientists keep warning about biodiversity limits, where that capital flows matters more than ever.

For a long time the accepted wisdom was that “doing good” with your money meant accepting weaker returns. The evidence increasingly says the opposite. Public markets are where the bulk of real-world capital actually lives, which makes them the most powerful lever an everyday investor has — and, as we explore in Is Impact Investing the Key to Beating the Market?, the companies solving hard problems are often the ones with the strongest structural tailwinds behind them.

That’s the whole idea behind this portfolio: align your capital with positive impact while generating strong returns. The first half of 2026 is a good illustration of why this combination pays off.

Through June 30, the Growth, Impact, Momentum portfolio returned +30.25% year-to-date. The S&P 500, over the same stretch, was up +10.09%.

That’s not a rounding-error win. The portfolio delivered roughly three times the market’s return in six months — and it did it while carrying a beta of 0.96, meaning it was actually a touch less jumpy than the market overall. Higher return, slightly lower volatility. That combination isn’t a fluke of one hot year; it’s the pattern the research keeps finding. The academic work on outperformance with positive impact shows that impact-tilted portfolios have historically matched or beaten the broad market with smaller drawdowns, and points to the structural drivers behind it: operational efficiency, real physical assets, and growth orientation.

Strong returns are only worth trusting if there’s real quality underneath them. Here there is.

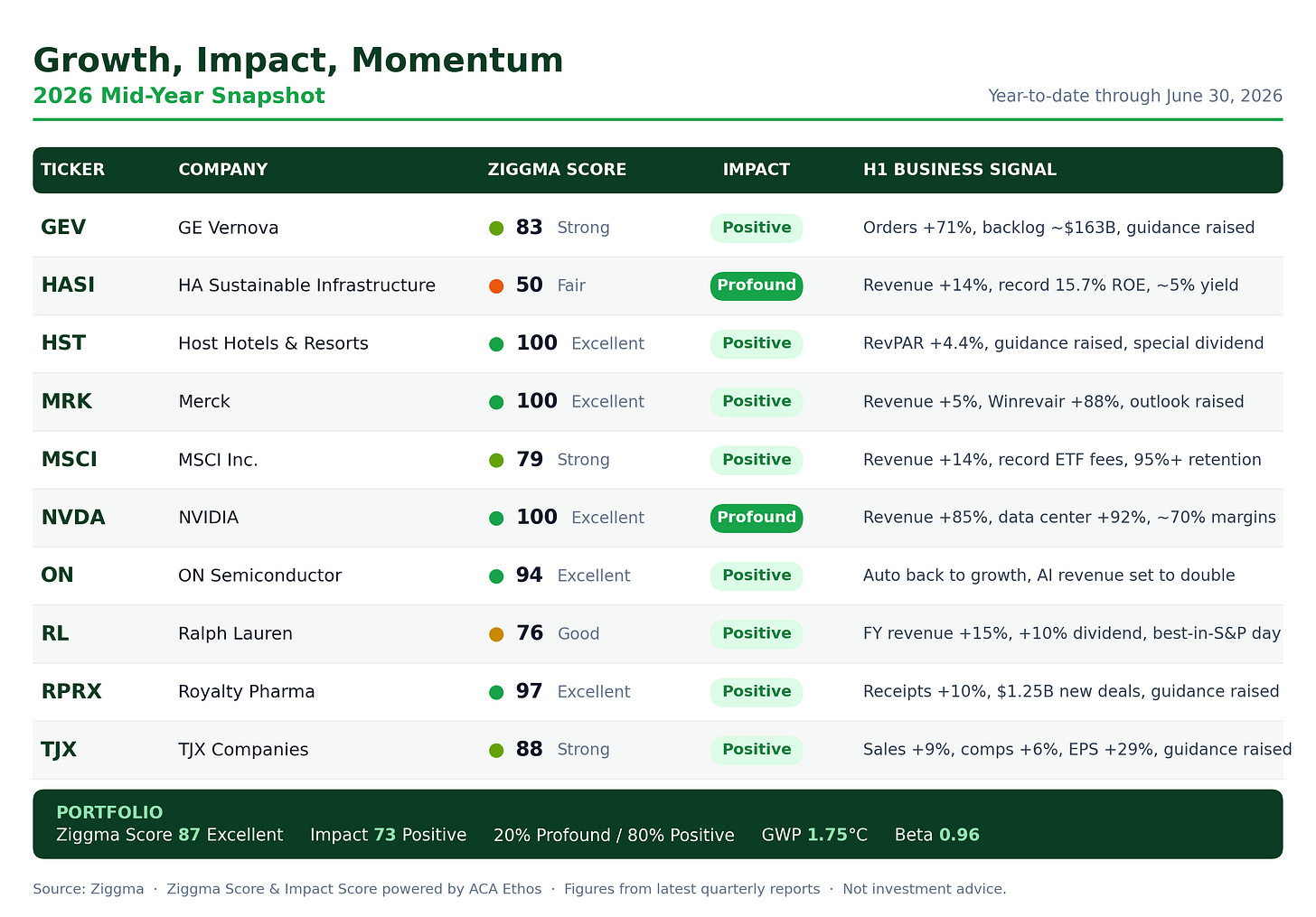

The portfolio carries an Excellent-range Ziggma Score of 87/100 — a composite built from more than 30 fundamental measures of growth, profitability, valuation, and balance-sheet health. Every holding but one sits at “Strong” or better, and half the portfolio scores 94 or higher. This is a collection of genuinely good businesses, not a basket of hopeful stories.

On the impact side, the portfolio earns a Positive Impact Score of 73/100, powered by ACA Ethos data. Twenty percent of the holdings are rated Profound — the highest impact tier — and the other 80% Positive. Its portfolio-level Global Warming Potential is 1.75°C, comfortably inside the Paris Agreement’s 2°C ceiling. In plain terms: these companies are, on balance, making the economy cleaner, safer, or more efficient — not fighting against that current.

That’s the case in one line. High-quality businesses, measurable real-world impact, and a return that tripled the market. Now the names.

The portfolio’s clean-energy anchor had a blockbuster first half, up more than 60% year-to-date and briefly hitting a record high. The business earned it: Q1 orders jumped 71% organically, backlog swelled to about $163 billion, and management raised full-year 2026 guidance on the back of surging demand for gas turbines and grid equipment — much of it to power AI data centers. The one caution is price: after a huge run, the stock trades at a rich multiple, so the bar for the next earnings report (due late July) is high. Business momentum, though, is firmly pointed up.

From the GoodStocks desk: GE Vernova sits at the center of global electrification and decarbonization, which is why it features across our research on the best climate tech stocks and best renewable energy stocks for 2026.

HASI is the purest impact play here — it finances solar farms, wind, battery storage, and other climate-positive projects, with over $16 billion in managed assets and a tool (CarbonCount) that measures the carbon cut per dollar invested. Q1 was strong: revenue up 14% and a record adjusted return on equity of 15.7%, all while paying a dividend near 5%. So why the modest Ziggma Score of 50? Because HASI’s REIT-style accounting and high payout depress the GAAP profitability metrics the score leans on. It’s the one name where we lean into Profound impact despite that modest score — a valuation the market has left cheap, with analyst targets pointing to meaningful upside.

From the GoodStocks desk: HASI is one of the infrastructure-and-financing names we highlight in our best renewable energy stocks research for its clean, direct exposure to the energy transition.

The nation’s largest lodging REIT owns luxury and upper-upscale hotels (Ritz-Carlton, Westin, Four Seasons) and quietly runs one of the highest-quality balance sheets in the portfolio — hence the perfect Ziggma Score of 100. Q1 beat expectations, with comparable RevPAR up 4.4%, and management raised full-year guidance. It also sold roughly $1.15 billion of hotels and returned the gains to shareholders via a special dividend. With the 2026 World Cup expected to lift US travel demand, the near-term setup is favorable. The stock is close to our target, so from here it’s more of a steady, income-generating quality holding than a big-upside bet.

From the GoodStocks desk: Host earns its place in our best sustainable stocks research for driving energy and resource efficiency across its real-estate portfolio.

Merck is the portfolio’s healthcare heavyweight, and the first half was about one question: can it grow beyond Keytruda before that mega-drug loses patent protection in 2028? Q1 said yes, so far. Revenue rose ~5% to $16.3 billion, Keytruda itself grew 12%, and newer drug Winrevair surged 88% — while management raised its profit outlook. In late June, the FDA approved a new Keytruda combination for a hard-to-treat breast cancer, sending shares up. The patent cliff is a real overhang, but the pipeline is broadening at the right time. A high-quality, life-improving business trading at an undemanding price — and, with no fossil-fuel exposure in its model, one of our best fossil-free stocks for 2026, adding clean, defensive ballast to the portfolio.

MSCI is the plumbing of modern investing — it builds the indexes and data that trillions of dollars are benchmarked against, including much of the world’s ESG and climate analytics. That makes it a quiet enabler of sustainable investing itself. Q1 was excellent: revenue up 14%, record asset-based fees, subscription sales up 52%, and a 95%+ client retention rate that shows how sticky the business is. AI is now speeding up how fast it launches new products. The one soft spot is its sustainability-data segment, where some clients are trimming spend — worth watching, but a small part of a very durable, high-margin machine.

Nvidia remains the engine of the AI build-out, and the business is compounding faster than almost any company its size in history: the most recent quarter posted $81.6 billion in revenue, up 85%, with data-center sales up 92% and margins near 70%. The stock spent the first half swinging on “is AI spending sustainable?” nerves rather than on anything wrong with the company — a gap between mood and fundamentals. Its Profound impact rating reflects 100% renewable-energy sourcing and chips that make computing dramatically more energy-efficient per task. Volatile, yes, but the demand signal keeps accelerating rather than fading.

From the GoodStocks desk: Our dedicated Nvidia deep-dive gives it an Impact Score of 92 — its chips deliver far more computing per watt, which lowers the energy cost of AI and powers breakthroughs in climate modeling, drug discovery, and clean energy. Real-world impact isn’t confined to solar panels.

ON Semiconductor makes the power chips behind electric vehicles, industrial systems, and increasingly AI data centers — the unglamorous hardware that makes electrification actually work. After a rough couple of years of inventory correction, the first half brought a clear inflection: Q1 marked the first year-over-year automotive revenue growth in seven quarters, gross margins expanded for a third straight quarter, and management now expects AI data-center revenue to double in 2026. Its silicon carbide tech holds roughly 55% share of new EV models shown at this year’s Beijing Auto Show. The stock has been choppy after a big run, but the recovery story is real and the score (94) reflects it.

Ralph Lauren’s multi-year “brand elevation” strategy — moving upmarket, leaning into full-price selling, cutting reliance on discount wholesale — is working. Its fiscal-year results in May were a standout: full-year revenue up nearly 15%, a 10% dividend hike, and the stock briefly the best performer in the entire S&P 500 on the day. Growth in Asia, especially China, has been a big driver. The shares have largely flatlined since that pop as investors digest the gains and weigh tariff and Europe risks ahead of the next report in early August. A well-run brand with pricing power and a cleaner, more efficient operating model.

From the GoodStocks desk: Ralph Lauren appears in our best sustainable stocks research for its operational and strategic transformation toward a leaner, higher-margin model.

Royalty Pharma has an unusual and powerful model: instead of discovering drugs, it funds their development in exchange for a slice of future sales, holding royalties on around 35 marketed and 20 development-stage therapies. That funding role helps bring more medicines to market — the impact angle — while producing steady, diversified cash flow. Q1 delivered 10% growth in cash receipts, $1.25 billion of new deals (including R&D partnerships with J&J and Teva), a 7% dividend increase, and another guidance raise. With a near-flawless Ziggma Score of 97 and a stock still trading below our target, it’s one of the portfolio’s most efficient compounders.

The parent of T.J. Maxx, Marshalls, and HomeGoods keeps proving that off-price retail thrives in almost any economy — and that its model, which redistributes excess inventory that might otherwise go to waste, has a genuine sustainability angle. Q1 was a beat across the board: sales up 9%, comparable sales up 6% in every division, and earnings per share up 29%, prompting another guidance raise and a bigger dividend and buyback. The one watch-item is fuel costs, which management flagged as a headwind. Our position sits just below cost after a soft three months for the stock, but the business itself is firing on all cylinders. A durable, defensive quality name.

From the GoodStocks desk: TJX features in our best sustainable stocks research as a reminder that reducing waste and improving system efficiency is a sustainability story too.

Six months in, the Growth, Impact, Momentum portfolio has done exactly what it’s designed to do: deliver market-beating returns — roughly three times the S&P 500 — from a lineup of genuinely high-quality, positive-impact businesses, and with slightly less volatility than the market along the way. That last point is the quiet headline. It’s the same pattern the research on impact and outperformance keeps turning up, and it’s the strongest rebuttal to the old idea that values and returns pull in opposite directions.

Looking to the second half, three things stand out. First, a run of Q2 earnings starting in late July — GE Vernova, Nvidia, and ON Semiconductor in particular — will test whether the AI-power and electrification boom keeps compounding or takes a breather. Second, the portfolio’s biggest winners (GEV, ON, RPRX, NVDA) now carry higher expectations, so watch for the gap between price and fundamentals to widen or close. Third, the steady quality names — HST, MRK, TJX, MSCI — should keep doing what they do regardless of the market’s mood.

Nothing about this first half suggests these are worse businesses than they were in January. If anything, most got stronger. The bet from here is the same one that’s worked all year: own excellent companies that are building a better future, and let the returns follow. History, and the first half of 2026, say they usually do.

______________________________________________________________________

A note on the numbers: Portfolio and benchmark returns are year-to-date through June 30, 2026. The S&P 500 is represented by SPY. Ziggma Scores are composite fundamental-quality scores from 0–100; Impact Scores and Global Warming Potential are powered by ACA Ethos. Company figures are drawn from the most recent quarterly reports available at the time of writing. Growth, Impact, Momentum is a Ziggma model portfolio built on our GoodStocks research and is provided for information only — it is not investment advice.