Every hotel room you check into, every meal served in a restaurant kitchen, every AI data center humming through the night — Ecolab has almost certainly been there first. It treats the water, prevents the contamination, cuts the waste. It is the kind of company that keeps the modern world running and even moving it towards a more sustainable path. And quietly, steadily, it has been compounding shareholder returns for decades while doing it.

What makes Ecolab unusual is that its business model and its environmental mission are inseparable. Every gallon of water it saves for a customer is a service contract renewed. Every ton of emissions avoided is a data point that wins the next deal. The more the world strains under water scarcity and AI-driven energy demand, the more essential Ecolab becomes — to its customers, to the planet, and to patient investors who understand that the best returns often come from companies solving problems that only get bigger over time.

That moment may be arriving faster than most people realize. A blockbuster acquisition announced earlier this year has planted Ecolab at the heart of the AI data center cooling boom, doubling its addressable market overnight. Wall Street has taken notice. And for investors looking for a stock that can grow a portfolio while helping conserve the resources the next generation will depend on, ECL deserves a serious look.

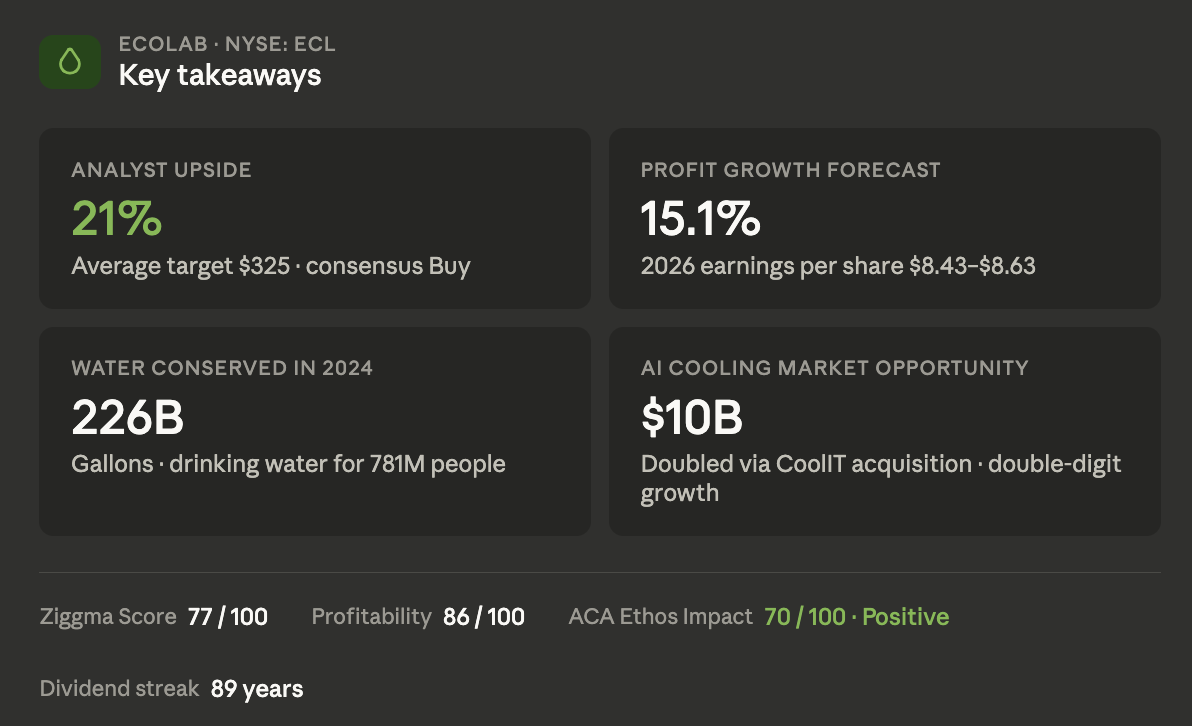

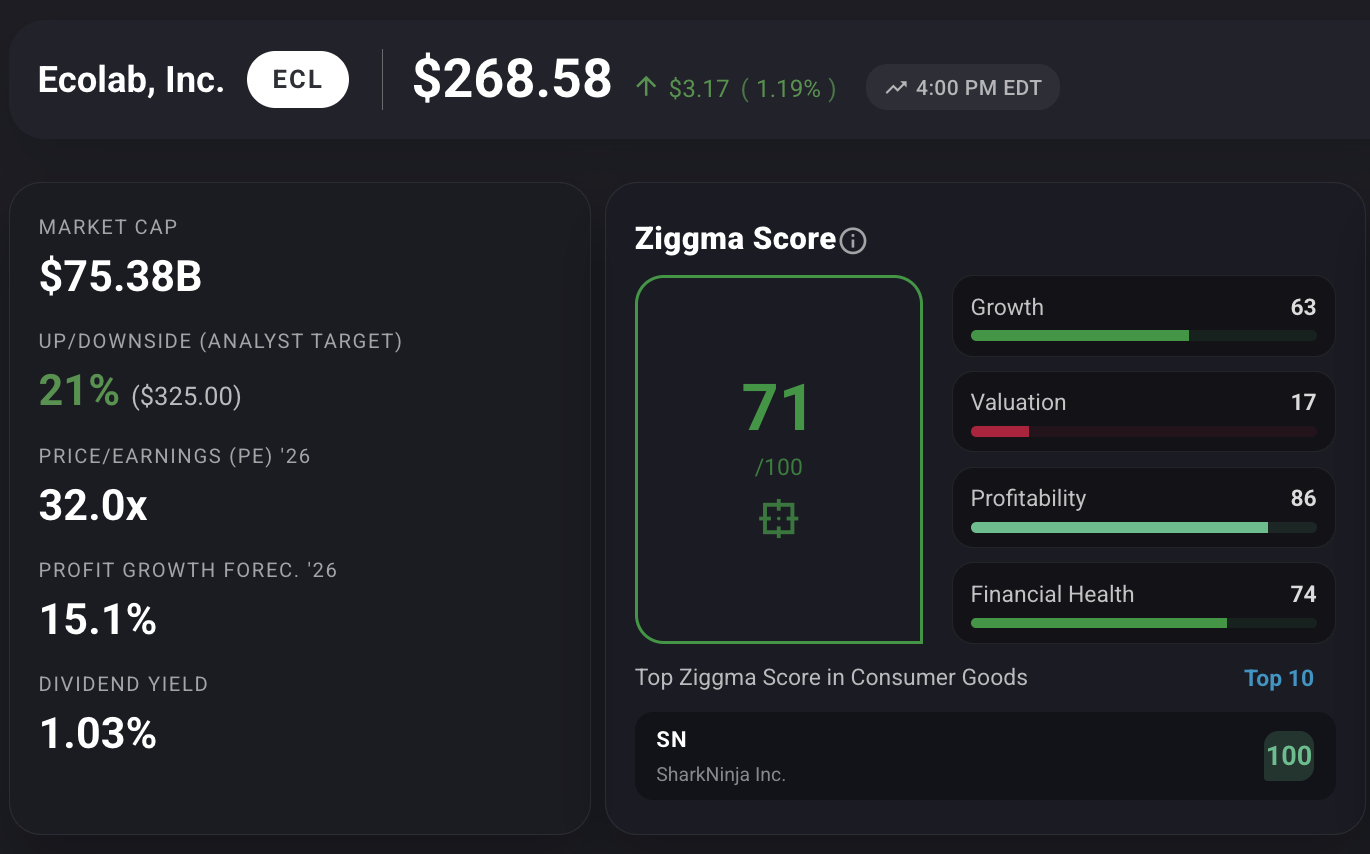

Ecolab is a slow-motion compounder that is about to accelerate. Revenue has grown at a 4.8% five-year average rate, but profit growth is the more compelling number: analysts forecast 15.1% earnings per share growth in 2026, and the CoolIT acquisition adds a high-margin, fast-growing revenue stream on top of the organic business. With 27 analysts covering the stock at a consensus "Buy," the $325 average price target reflects confidence that pricing power, operational leverage, and the AI tailwind have not yet been fully valued in the current share price.

Ecolab's business model and its environmental mission are the same thing. In 2024, its solutions helped customers avoid 4.6 million metric tons of greenhouse gas emissions and conserve 226 billion gallons of water — while the company itself reduced its own Scope 1 and 2 emissions by 33% and sourced 71% of its electricity from renewable energy. CDP, the gold standard for corporate environmental disclosure, awarded Ecolab an A on climate change and A- on water security in 2024. These are not pledges. They are audited outcomes.

Ecolab is not a sustainability-first company that happens to sell chemicals. It is a $75 billion market cap enterprise whose entire revenue base is built on helping industrial, institutional, and high-tech customers use water and energy more efficiently. Founded in 1923 and headquartered in St. Paul, Minnesota, Ecolab serves more than three million customer locations across 170 countries. Its five operating segments cover industrial water treatment, food and beverage processing, institutional and hospitality hygiene, healthcare and life sciences, and pest elimination.

What gives Ecolab its moat is not any single product — it is the combination of proprietary chemistry, digital monitoring platforms, and an embedded service model that makes switching costly and underperformance visible in real time. Customers do not buy Ecolab's cleaning chemicals and walk away; they sign into ongoing service relationships backed by Ecolab field specialists. That creates sticky, recurring revenue with long contract terms.

The market opportunity is growing faster than it has in years, for one simple reason: AI. Data centers need enormous amounts of water and energy to cool high-performance computing systems. Ecolab's March 2026 acquisition of CoolIT Systems — a liquid cooling specialist for next-generation AI infrastructure — positions it as the only company offering end-to-end fluid and thermal management for data centers. The deal doubles Ecolab's total addressable market in high-tech from $5 billion to $10 billion, and that market is growing at double digits annually. As Ecolab CEO Christophe Beck put it at the deal announcement: "AI is transforming the demands on data centers, and liquid cooling is one of the critical technologies that makes advanced computing possible."

Consistent margins, accelerating earnings

Ecolab's financials tell the story of a steady compounder hitting its stride. Net profit margin came in at 13.0% in 2025, up from 9.0% in 2021. Return on equity has held in the 22–25% range for three consecutive years — the Ziggma Profitability sub-score of 86 reflects exactly this kind of durable earnings quality. Operating cash flow grew at 7.4% over five years, and the company has raised its dividend for 34 consecutive years, with a 13.6% dividend increase in 2025 alone.

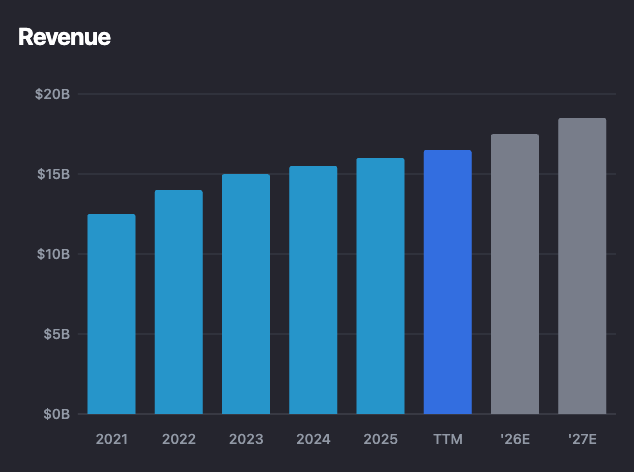

Revenue growth has been measured rather than explosive — up 2.2% in 2025 and 4.9% on a five-year average basis — but the earnings trajectory tells a more powerful story. Earnings per share has compounded at 16.8% annually over five years. The Ziggma Growth sub-score of 71 acknowledges both the steady momentum and the forward acceleration expected from CoolIT, with next year's projected revenue growth of over 10%.

Is it expensive?

At a price-to-earnings ratio of 32x on 2026 estimates, ECL is not cheap by traditional measures. The Ziggma Valuation sub-score of 17 reflects that. But context matters: Ecolab's peer group in specialty chemicals and water technology typically commands a premium, and the CoolIT acquisition reframes the earnings trajectory. With 15.1% profit growth forecast for 2026 and the high-tech segment poised to become a major growth engine, the current multiple looks more reasonable against a two- to three-year earnings horizon. The 1% dividend yield is modest but adds a compounding kicker for long-term holders.

Risks worth knowing

The CoolIT deal is priced aggressively at $4.75 billion in cash, bringing leverage to roughly 3x at closing — a meaningful increase from Ecolab's historically conservative balance sheet. Integration risk is real. Beyond that, Ecolab's industrial and institutional segments are exposed to slower economic conditions and cuts in capital spending by large food and beverage manufacturers. Currency translation remains a headwind given its global footprint. None of these risks change the long-term thesis, but they are worth monitoring.

The upside in plain terms

Analysts put the average 12-month price target at $325 on a stock trading around $268. That is roughly 21% potential gain before dividends, from a business scoring 86 on profitability, a new AI growth catalyst, and a track record of beating earnings estimates. Ecolab looks like a Path 1 compounder — a business whose fundamental quality and secular tailwinds support long-term shareholder value creation, not just a short-term trade.

The world's water problem is Ecolab's growth engine

Water scarcity is accelerating. The World Resources Institute estimates that by 2025, roughly one-quarter of the global population faces high water stress. Ecolab does not merely acknowledge this risk — it has built a $16 billion business around solving it. In 2024, its technology helped customers conserve 226 billion gallons of water while managing one trillion gallons across global operations. Its 2030 goal is to help conserve 300 billion gallons annually — enough drinking water for one billion people every year.

The Climate Action score of 70/100 on Ecolab's ACA Ethos Impact profile reflects genuine progress. Carbon intensity fell 2% in the most recent year, and Ecolab's own operations run on 71% renewable electricity. The company has earned SBTi validation for its emissions reduction targets — an independent verification that its goals are credible and science-aligned.

Circularity at scale

Ecolab's commitment to circular economy principles extends to its product packaging. In 2024, the company avoided 15.9 million pounds of virgin plastic resin — representing 15% of its total plastic packaging by weight. Currently, 91% of Ecolab's packaging is either reusable or recyclable-by-design. New products like the ReadyDose tablet-based cleaning system deliver a 98.8% reduction in plastic packaging waste compared to conventional liquid equivalents. These are the kinds of measurable, audited outcomes that distinguish genuine sustainability leaders from companies that publish annual reports with green covers.

The Fair Labor score of 60/100 reflects a mixed picture internally. An employee rating of 3.70/5 and a near-perfect gender equality score of 97 speak to a genuinely inclusive workplace culture. The CEO-to-median-worker pay ratio of 327:1 is high — a point worth transparency rather than deflection. Ecolab's Accountability score of 46 underscores that even strong impact companies have room to grow on the governance side.

Ecolab is not a flashy company. It does not make electric vehicles or deploy solar panels. What it does is arguably more important: it helps the world use water and energy far more efficiently, at a scale no competitor matches. With 226 billion gallons conserved in 2024, 4.6 million metric tons of emissions avoided for customers, and a brand new position at the intersection of AI infrastructure and water management, Ecolab has built a business where doing good and compounding shareholder value are the same thing.

At $268, with a $325 analyst price target, a Ziggma Score of 77, and an Impact Score of 70, ECL earns its place in the Good Stocks universe. This is a stock for investors who want their portfolio to reflect the world they want to live in — and want it to grow while it does.

Disclaimer

This information is provided solely for general information and educational use. It is not intended as, and should not be construed to be, financial, investment, tax, legal, or other professional advice. Data used in the analysis is derived from third-party sources and applicable at the time of publication of the analysis. No representation or warranty is made as to the accuracy or completeness of the information or any analysis herein.

Ziggma is not registered or licensed as a financial advisor, broker-dealer, or tax professional. Readers should perform their own independent research and seek advice from appropriately qualified professionals before making any financial, investment, or legal decisions.

You should presume that, as of the date this report is published or any related communication referencing publicly traded securities or assets, Ziggma team members may hold positions in the securities or assets discussed and could benefit financially from price movements. Positions may be changed without notice.

There is no duty to revise or update the content after publication. Neither Ziggma nor any affiliated parties accept responsibility for market changes, economic developments, or subsequent events that could affect the relevance or accuracy of the information.

Forward-Looking Statements

This report may include forward-looking statements, such as forecasts, projections, estimates, or expectations regarding financial outcomes, market dynamics, or future corporate developments. These statements are based on assumptions that may not hold true, and actual results may vary materially. The author undertakes no obligation to update or revise any forward-looking statements as circumstances change.

Third-Party Data & External Sources

Certain information is sourced from third parties. Nonetheless, the accuracy, completeness, and timeliness of such information cannot be assured. Ziggma disclaims any responsibility for errors or omissions in third-party data and does not endorse, verify, or assume accountability for the methodologies or conclusions of external sources.

AI-Generated Enhancements

AI tools can be used to enhance clarity, structure, and brevity, and to assist with research organization, ideation, and analytical review.

Redistribution

You may share this report for informational purposes. However, reproduction, distribution, republication, or modification of any portion of the content, in whole or in part, without prior written consent is prohibited.

Investment Risk Disclosure

All investing carries risk of loss.. Historical performance does not guarantee future outcomes. References to specific securities, companies, or strategies are for informational purposes only and do not constitute recommendations or endorsements. Any use of, or reliance on, the information in this report is entirely at the reader’s own risk.

Neither Ziggma nor affiliated parties shall be liable for any direct or indirect losses or damages of any kind arising from the use of this report or reliance on its contents. By accessing this report, you agree to indemnify and hold harmless Ziggma and affiliated parties from any claims, liabilities, or damages resulting from your use of the material.

You alone bear responsibility for your decisions. Use this information at your own discretion and risk.